Matthew Kerkhoff, options expert and editor of Dow Theory Letters, has written an exceptional 14-part educational series on understanding options and their role in investment portfolios. His series begins this week with the basics of calls and puts. Each Friday on MoneyShow.com through December, Matt will delve into increasingly more sophisticated strategies.

Today we’re going to take a little departure from our typical conversation and talk a bit more about portfolio strategy. In particular, we’re going discuss the role of options in an investment portfolio.

If you just cringed, don’t worry. Many people have that same reaction when they hear the term “options,” because it may conjure up images of excess risk and leverage. For the average investor, options seem like a complicated way to potentially lose large sums of money.

In reality, that view couldn’t be further from the truth. Yes, there are options strategies that can be employed to increase leverage and risk, but the reverse is also true, and is much more common. Professional investors almost ubiquitously use options as a component of their overall strategy, and in most cases they do it to reduce risk, rather than increase it.

I became interested in the use of options nearly ten years ago while earning my MBA at the University of San Diego. Originally introduced to them via an investments course, I found that they provided a very unique way to structure positions in the market that couldn’t be replicated through the purchase of stocks and ETFs.

In the following years I traded options quite heavily and became enamored with their use in enhancing and protecting returns. I still use options as an ongoing part of my investment approach, and have been asked by many subscribers of Dow Theory Letter to elaborate on a few of the strategies that can play a beneficial role in a conservative investor’s portfolio.

As a result, we’ve decided to start a new “mini-series” if you will, focused on providing a foundational level of knowledge on the use of options.

We’ll begin with a cursory overview of exactly what options are, and then we’ll discuss a few of the strategies that are consistently effective (there are many that aren’t). As time goes on, we’ll begin to relate these options strategies to the broader market, and include recommendations from time to time as conditions warrant.

The end goal here is to add a few tools to your investment toolbox, enabling a wider array of profit opportunities and more effective ways to protect and manage your portfolio.

Introduction to Calls and Puts (Part 1)

When it comes to using options, there are many strategies, but there are only two types of options: calls and puts. Every position that is built using options is comprised of either calls, puts, or a combination of the two.

Thus, if you can understand calls and puts at their fundamental level, then adapting them to strategies as we move forward will be much easier.

Before we get into the specifics of calls and puts, it’s important to understand that options are a direct form of investment.

As we’ll see later, an investor can achieve everything they want in terms of positioning just by using calls and puts. In fact, nearly every position you could ever want to take in stocks, bonds or ETFs can be replicated using options, often with a better risk/reward profile.

For our purposes, most of our attention will focus on using options in conjunction with regular stock or ETF positions we own. We’ll also discuss using options as a way to get better pricing on stocks and ETFs that we would like to own.

Options (calls and puts), are called “derivatives” because they derive their value from some other investment. This is called the “underlying” security.

Examples would include Apple (AAPL), the S&P 500 ETF (SPY) or even a bond fund like the iShares US Aggregate Bond Fund (AGG). If a stock or ETF has an “options market” it means that calls and puts can be traded on that underlying security.

Nearly all large cap stocks and popular ETFs have options markets. This makes our life pretty easy as most of these markets are highly liquid and allow investors to build and liquidate positions with ease.

Calls and puts can both be bought and sold, just like any other security. One especially nice aspect of options is that you don’t necessarily have to own a call or put in order to sell one. As we’ll see over the course of the next few months, some situations will warrant buying calls and puts, and others will warrant selling calls and puts.

FREE 14-part guide to options: The Basics to In-Depth Portfolio Strategies

When determining which side to be on (buying vs. selling), it’s important to remember this general rule of thumb: Option buyers have rights; option sellers have obligations.

The implications of this statement will become more clear as we progress, but this is a fundamental truth and one that will affect every decision regarding the use of options.

Okay, enough beating around the bush. Let me explain exactly what calls and puts are, and then we’ll wrap up with a brief summary.

A call option is the option to buy an asset at an agreed upon price on or before a particular date.

A put option, on the other hand, is the option to sell an asset at an agreed upon price on or before a particular date.

Again, keep in mind that both call options and put options can be bought and sold. If you’re the buyer of a call option, it means you have the right to buy the underlying asset. If you’re the seller of a call option, it means you have conveyed to someone else the right to buy the underlying asset from you (recall our general rule of thumb above).

Conversely, if you’re the buyer of a put option, it means you have the right to sell the underlying asset. And if you’re the seller of a put option, you have conveyed to some else the right to sell you the underlying asset.

If that doesn’t make sense right off the bat, don’t worry. Things will become more clear as we progress and go through examples. In the meantime, just understand that there are two types of options (calls and puts) and each one can be bought and/or sold.

Wrapping things up, I want to go through a bit more of the vocabulary and terms that are associated with call and put options.

We’ve already discussed the “underlying asset,” which is the asset that the call or put option derives its value from. The two other important aspects that we need to be aware of with options are the “strike price” and the “expiration date.”

As mentioned earlier, call and put options convey the right (but not the obligation) to buy or sell assets at an agreed upon price. That price is known as the strike price. As we’ll see moving forward, choosing the right strike price is an integral part of using options to your advantage.

Next, all options have an end date, or expiration date. When an option is traded, the rights and obligations of that option (whether it be a put or a call) only last until a certain point in time.

This could be anywhere from a day or two in the future, up to many years from now. Here as well, choosing the right expiration date is a very important factor.

There are more nuances to options pricing that we’ll get into, but what we’ve discussed so far should suffice as an initial introduction.

In the next segment, we’ll go through examples for buying a call option, selling a call option, buying a put option and selling a put option. We’ll also discuss what factors in the marketplace affect the pricing of options.

Introduction to Calls and Puts (Part 2)

Now let’s begin by going over some examples of buying and selling a call option.

Buying Calls

The best place to start when it comes to understanding how option contracts work is to look at buying calls. This is because call buying is one of the simplest ways of trading options, and it positions the buyer to benefit from a rise in the underlying stock or ETF.

As we walk through these examples, we’re going to use hypothetical pricing to understand various payoff scenarios. Therefore, it’s important that you understand two crucial aspects of option pricing right off the bat:

Advertisement

1. Every option contract, whether a call or put, represents 100 shares of the underlying security.

2. Option prices are shown and quoted on a “per share” basis.

Here’s what that means. If you were to look up the price of a call option, and your screen showed that option trading at $2, it would cost you $200 (plus any commission) to execute the trade. This is because one option contract represents 100 shares, and the price of that option is $2 per share. Make sense?

If not, it’ll probably become more clear as we walk through some examples, which we’ll do right now.

In order to visualize the payoff scenarios of buying and selling options, we use handy little profit and loss charts like the one below. If you can get in the habit of viewing option trades visually like this, it will go a long way in helping you select the right trade at the right time.

Okay, let’s dive right in.

In this first example, we’re going to look at the profit and loss scenario of buying a call option.

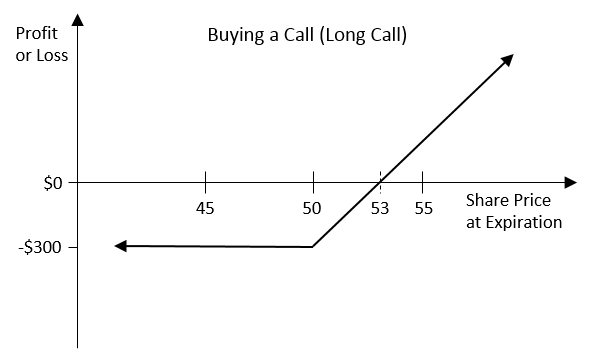

Suppose ABC stock is trading at $50 per share. We are bullish on the stock and believe it will trade higher in the months ahead. Therefore, we purchase a call option priced at $3, that has a strike price of $50.

The chart below shows the payoff scenario from buying that call option. The first thing to observe is that this trade cost us $300 (plus any commission) to execute. As described above, this is because while the call option was priced at $3, it represents 100 shares, so our total outlay is $300.

In exchange for this $300, we have purchased the right (remember our rule of thumb) to purchase 100 shares of ABC, on or before expiration, for $50 per share. In effect, we get to “control” 100 shares of ABC stock until expiration.

One nice thing about buying options is that your potential downside is limited. In this case, as buyers of the call option, the most we can lose is our $300. We have the right to buy 100 shares of ABC stock at $50 per share, but we are not obligated to make that purchase. If ABC stock isn’t trading above $50 at expiration, our call option will simply expire worthless.

As you can see in the chart above, at a share price of $50 or less, we sustain our maximum loss, which is $300. But if ABC rallies, as we think it will, then our gains with this call option are potentially unlimited. As ABC trades above $50 per share, our call option gains value quickly.

One of the most important aspects of assessing an options trade is to look at the breakeven point. This is the share price at which the underlying stock (in this case ABC) must trade for the option to be worth what you initially paid for it at expiration.

In this example, that share price is $53. The math here should be straightforward. Our call options gives us the right to buy 100 shares of ABC at $50 per share.

If ABC is trading at $53 per share at expiration, then it means our call option gives us the right to buy 100 shares at $50, which we could theoretically then sell right back into the market at $53 per share. Our profit from that would be $300, which is exactly what we paid for the option in the first place.

If ABC trades between $50-$53 at expiration, then we know we will suffer a loss of somewhere between $0 - $300. But if we’re right, and ABC does move higher, anything above $53 becomes profit.

For the sake of the example, let’s say ABC is trading at $56 at expiration. This means that our call option would be worth $600 [($56 - $50) x 100]. Since the call option cost us $300 initially, it means we have a profit of $300, or 100%.

And if ABC trades even higher than $56, we get to capture all the upside in the stock until the expiration date. Not bad, right?

To summarize, here is what we need to remember about buying call options:

* It’s a strategy for when we are bullish on a stock or ETF

* There is limited downside (the price or “premium” that we paid)

* There is unlimited upside

Now, let’s flip the script and see what the trade above would look like if we were on the opposite side, as the seller of the call option.

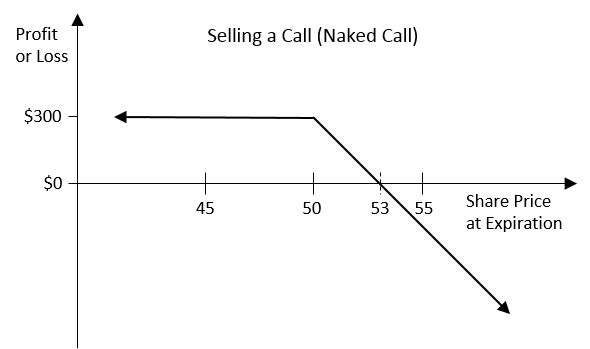

Selling Calls

One quick terminology note before we get started -- when you sell an option (either a call or put) that you do not already own (and you do not have a position in the underlying stock), it’s called a “naked” call or put. This term comes from the unlimited risk nature of the trade.

Before you start to worry, know that there are very few instances in which it is advisable to do this. In most cases, when we sell options we will have a position in the underlying stock or ETF; thus these will be considered “covered” options. Or we’ll be using a different option to hedge out the risk that selling a naked option creates.

For now, it’s important to understand how these options work on their own before we start combining them with other positions.

In the previous example, when we bought our call option for $300, someone was on the other end of the trade selling us that call option. The chart below shows the payoff scenario from that person’s point of view.

In this case, the $300 is actually revenue to the call seller, and this represents the most that the call seller can possibly earn on the trade. As long as ABC trades at $50 or less by expiration, the call seller will have made $300 on the trade. Why is this?

Because if ABC is trading at less than $50 at expiration, then the call option that we purchased will be worthless. After all, why would we exercise our option to buy shares at $50 if we can buy them in the market for cheaper?

In this scenario, the call option is said to have expired worthless, and the option seller gets to keep all of the premium he or she received.

But in exchange for this $300, the option seller has obligated himself to sell us 100 shares of ABC stock for $50 per share, if we so desire.

This means that from the option seller’s perspective, his payoff begins to decline as the share price of ABC rises. At the breakeven price of $53 (at expiration), the option seller has received $300 in revenue, but is obligated to sell us 100 shares at $50 per share.

If this truly was a naked call on his behalf, then he would have to go into the market and buy 100 shares of ABC at $53 per share, which he would then turn around and sell to us for $50 per share. This would result in him losing $300, which would offset the premium he earned, causing him to break even.

As the share price rises above $53, making good on the obligation the option seller committed himself to becomes more difficult. Since stocks have no upper bound, the price at which the option seller must buy shares at in order to sell to us has no limit. If the stock soared to $100 by expiration, the option seller could lose $4,700 [(($100 - $50) x 100) – 300].

This is why, generally speaking, an option seller would want to hedge or cover that unlimited risk somehow. We’ll get into how to do that later.

For now, let’s summarize what we need to remember about selling call options:

* It’s a strategy for when we are neutral to slightly bearish on a stock or ETF

* There is limited upside (the premium collected)

* There is unlimited downside (unless the position is hedged some way or another)

If you’ve made it this far, congrats, some of this stuff can be difficult to conceptualize at first.

By now you should have an understanding of what a call option is, and how the benefits, rights and obligations vary between the buyer and seller, based on the terms of the contract.

In the next article, we’ll go through this same exercise for puts, and then we’ll talk about what factors affect the pricing of options. We’ll also discuss some of the finer aspects of trading options. After that, we’ll be ready to dig into specific options strategies.