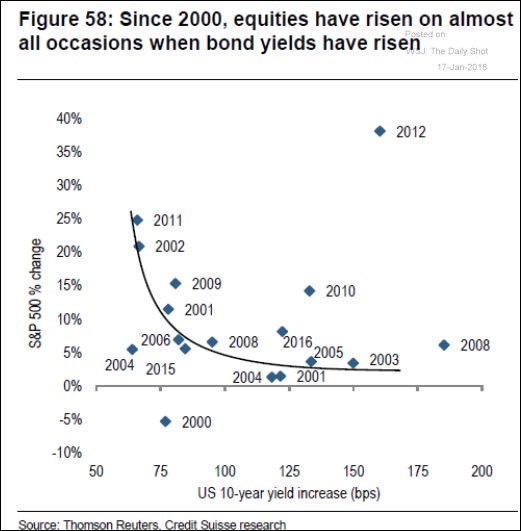

Investors focused on bonds look at the 30-year bond yield and say 2.8937% implies growth won’t be strong in the coming year. However, equities have increased in almost every year the 10-year bond yield has increased since 2000, writes Don Kaufman, co-founder of TheoTrade.

There are a few countervailing theses on how bonds yields are related to stocks. One thesis says stocks do well when yields are low because there is no other option, but to buy stocks. This theory has had great results in the past few years but might run up against problems in the future because the 10-year Treasury bond has a higher yield than the S&P 500 dividend yield.

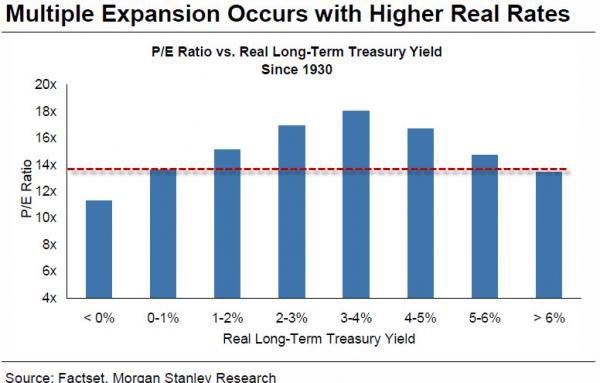

It turns out that TINA (there is no alternative) investing has only occurred in this cycle. Usually, when yields are low it’s bad for multiples. It’s confusing because stocks were up when the signal was poor, so are they going to go up when the signal is good? The chart below shows the signal we’re discussing. As the real long-term Treasury yield increases, the PE multiple increases. It then peaks at 3%-4% before falling as yields increase. This chart is referred to as a frown because of the shape of the bars.

Investors focused on bonds look at the 30-year bond yield and say 2.8937% implies growth won’t be strong in the coming year. However, the chart below sees it differently. As you can see, equities have increased in almost every year the 10-year bond yield has increased since 2000. To be fair, this chart doesn’t have much history.

Stocks have gone up almost every year since 2000 anyway. Ignoring that caveat, the economy and stocks look like they are about to have a strong 2018 as the 10-year bond yield has been spiking in the past few weeks. Its 2.6163% yield is the highest yield since March 13, 2017, when the yield was 2.6258%.

The highest point in the past 5 years was 3% on December 27, 2013. That signaled 2014 was going to be a great year for the economy. It fell from there, correctly indicating the economy would have a bad 2015 and 2016. I see the 10-year yield getting above 3% as I think the tax cut will help 2018 reach the highest GDP growth rate in this expansion.

The update on the difference between the 10-year and 2-year yield is 57.7 basis points as the yield curve recently has steepened. You never hear about steepening because the flattening elicits fear.

My point about how the yield curve won’t necessarily invert in the next couple months stands. It often has countertrend steepening periods which lengthens the time it takes to get to an inversion.

Capex set to increase

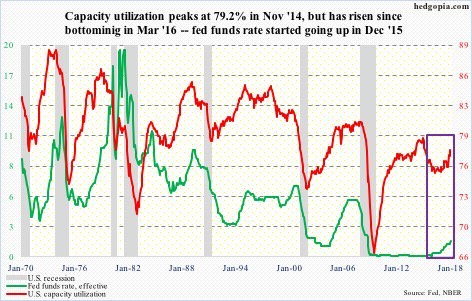

As has been suggested from surveys, the capacity utilization rate suggests capex will accelerate in 2018. As you can see from the chart below, the capacity utilization rate peaked at 79.2% in November 2014. After bottoming at 75.4% in March 2016, the rate has been in an uptrend. The latest reading was 77.9% last December.

Just like the 10-year bond yield, I expect the capacity utilization rate to make a new cycle high. As we mentioned, this is a signal capex growth will start to increase. Historically, the 80% level has been accompanied by strong capex. One long-term issue is that each capacity to utilization peak in the past 5 cycles has had a lower high.

The 2014 peak would make this the sixth straight cycle. It will be interesting to see if the peak in 2018 gets to the level of the previous cycle. This metric is important because low capex spending and the low capacity utilization rate have been blamed for the low productivity growth. Remember, high productivity growth helps workers get real wage hikes.

Strong jobless claims report sweeps away recession fears

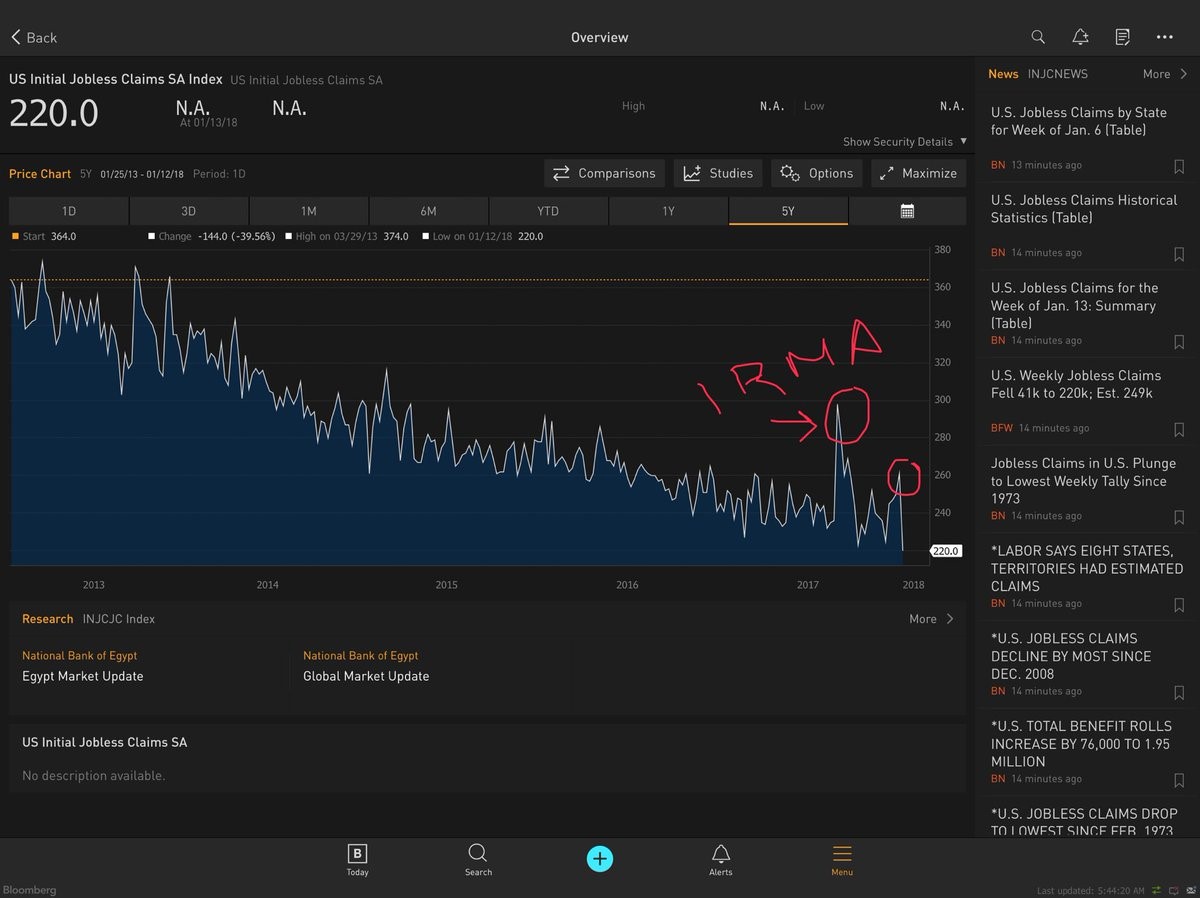

Some investors and macroeconomic advisors misinterpreted the recent spike in jobless claims, saying they thought it meant a recession was coming later this year.

You need to be able to differentiate near-term noise from one time events like the weather from actual trend changes. The previous increase was mainly caused by one time events which signaled to me that the labor market was strong.

The latest report was the opposite of the previous reports in that it was forced lower by a one-time event. Claims fell from 261,000 to 220,000 which was the lowest reading since February 1973. Anyone worrying about the time since the bottom in jobless claims will need to start their recession countdown over again.

You can see the spike was caused by Hurricane Irma in the chart below. The more recent spike was caused by the cold weather and the holidays. The latest trough was probably overstated because the results from California, Arkansas, Kentucky, Maine, Hawaii, Virginia and Wyoming were all estimated. Estimates can be wrong.

Since the report was so low, we can assume the estimate was too aggressive. The results may have been affected by the Martin Luther King Day holiday on Monday. I expect this week’s report to show somewhere between 230,000 and 250,000 jobless claims if it’s not affected by another one-time event. Either way, the labor market remains strong.

Valuations

The 10-year Shiller PE is at 33.86 which means it’s about 10 points below the all-time peak of 44.19 which occurred in December 1999. Some investors say the 10-year Shiller PE isn’t a great metric because it includes the weak earnings from 2008.

I’m conflicted because I think the Shiller PE was built to include recessions and expansions. If this expansion lasts a little longer, it will become greater than 10 years which means the metric will only have data from the expansion.

On the other hand, the earnings from 2008 were worse than the usual recession. To follow up on that point, investors follow Shiller PEs which don’t include the 2008 period. The chart below shows the 10-year Shiller PE and the 7-year Shiller PE. As you can see, the 7-year Shiller PE is at about 27 which makes it close to the most expensive period since 1999. The 1999 peak is 40 which means the market is about 13 points cheaper.

No matter how you look at the data, this is an expensive market.