If Mr. Market sees more hawkish-risk from the FOMC today, we may see a stronger USD and weaker Treasury yields through Wednesday, allowing us to stay short/inverse precious metals and long defensive equity sectors, writes Ziad Jasani of the Independent Investor Institute.

This week starts with the Feb. 9 Global Equity Market’s bounce intact but slowing into resistive structures, which kept us defensive into the close on Feb. 16 vs. adding significantly to the bounce.

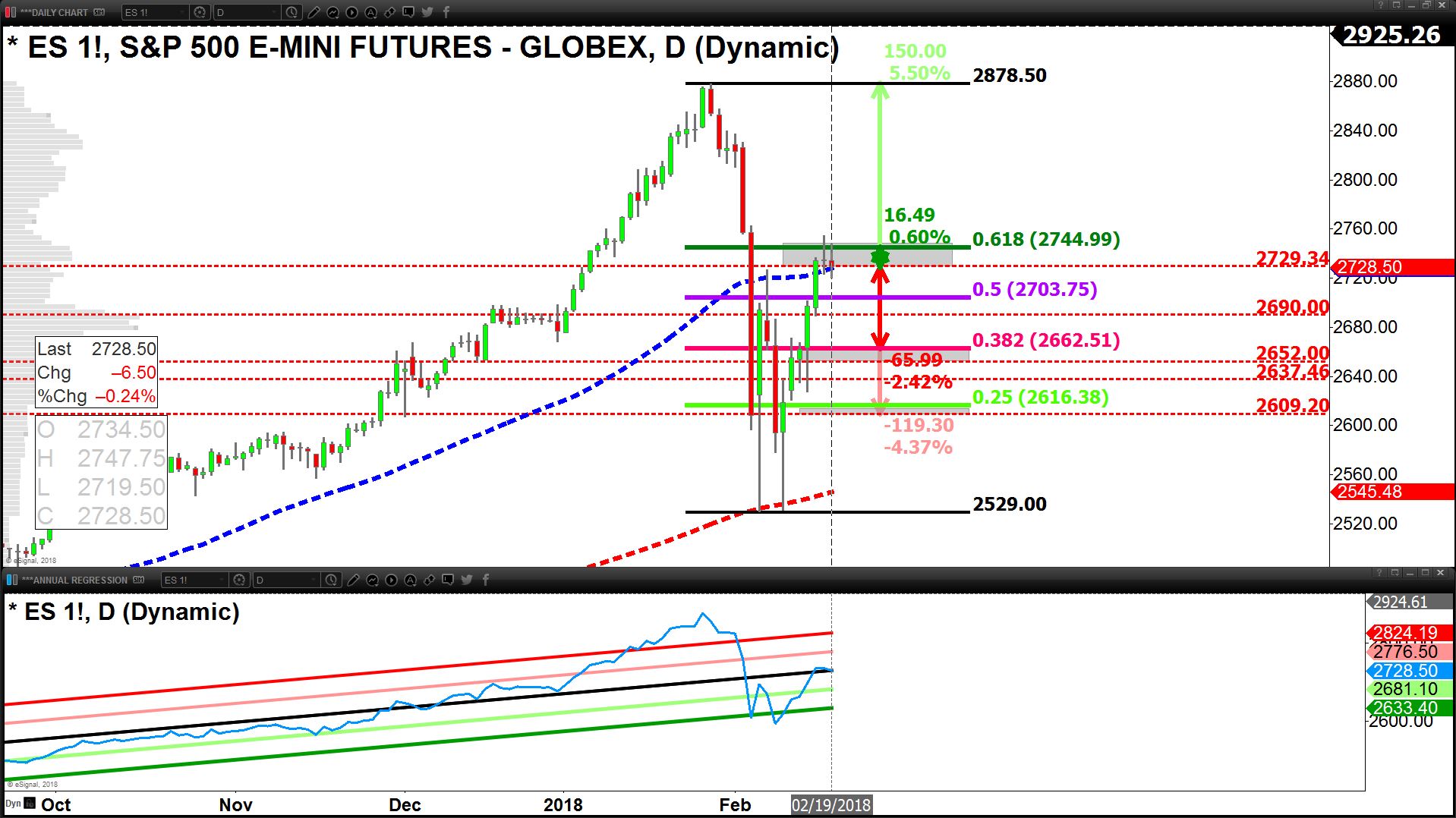

The S&P 500 Futures Index presents with 2 Indecision Candles within resistance of 2,745 – 2,729 (Feb 16 & 19). Clearing above said resistance implies a move up towards 2,825 or +3.54%; with minor resistance at 2,810-2,805. However, remaining below resistance of 2,745-2,729 implies at minimum a move down to test 2,664 - 2,652 or -2.42% away.

The question we asked and answered at our Feb. 16. Workshop was: “Should we stay or should we go?”

The answer was unearthed through a detailed review of macro variables during our Weekly Workshop Feb 16:

• Currencies/Precious Metals: Swing behavior suggests at least a few days of euro, yen and CAD weakness supporting a mildly stronger USD:

--Implications #1: Removal of long precious metal trades, and trying to play short over the weekend.

--Implications #2: A stronger USD may also stunt the bounce in Oil and the Technology space, implying profit taking before the weekend and/or tight stop losses for those playing out the Feb. 9 Market Bounce.

--Implication #3: A stronger USD would weaken the CAD, perhaps providing some fertile ground for the Canadian Financial Sector (XFNT) to start out-performing as earnings come in late this week (Thursday, Feb. 22 Royal Bank & CIBC).

• Bonds / Yields: High risk Credit Markets (JNK, HYG, EMB) bounced with equities, averting a bond market crisis as yields softened up to end last week, mainly on faith that the Fed will stick to its plan for three rate hikes in 2018, furthered by comments/events from the ECB and BOJ that leaned dovish last week.

No technical event has transpired on US Treasury yields until the 10-year is back below 2.7%; closed the week at 2.877%. However, the recent inverse correlation between USD direction and yields is likely to keep some downward pressure on yields at the front end of the week ahead:

--Implication #1: Bonds stabilizing may be short-lived but helpful to keep the equity bounce intact; that doesn’t mean we can’t see a re-test of support at 2,664-52 on the S&P 500

--Implication #2: We translated the evidence of swing-highs on the EUR/USD currency pair and wwing lows on the USD/JPY pair to move into higher risk long trades in Defensive Equity Sectors on Feb 15 & 16 and carried the positions over the weekend (XLU, XLP, VNQ, IYZ, XST-T, XRE-T, ZUT-T, BCE-T)

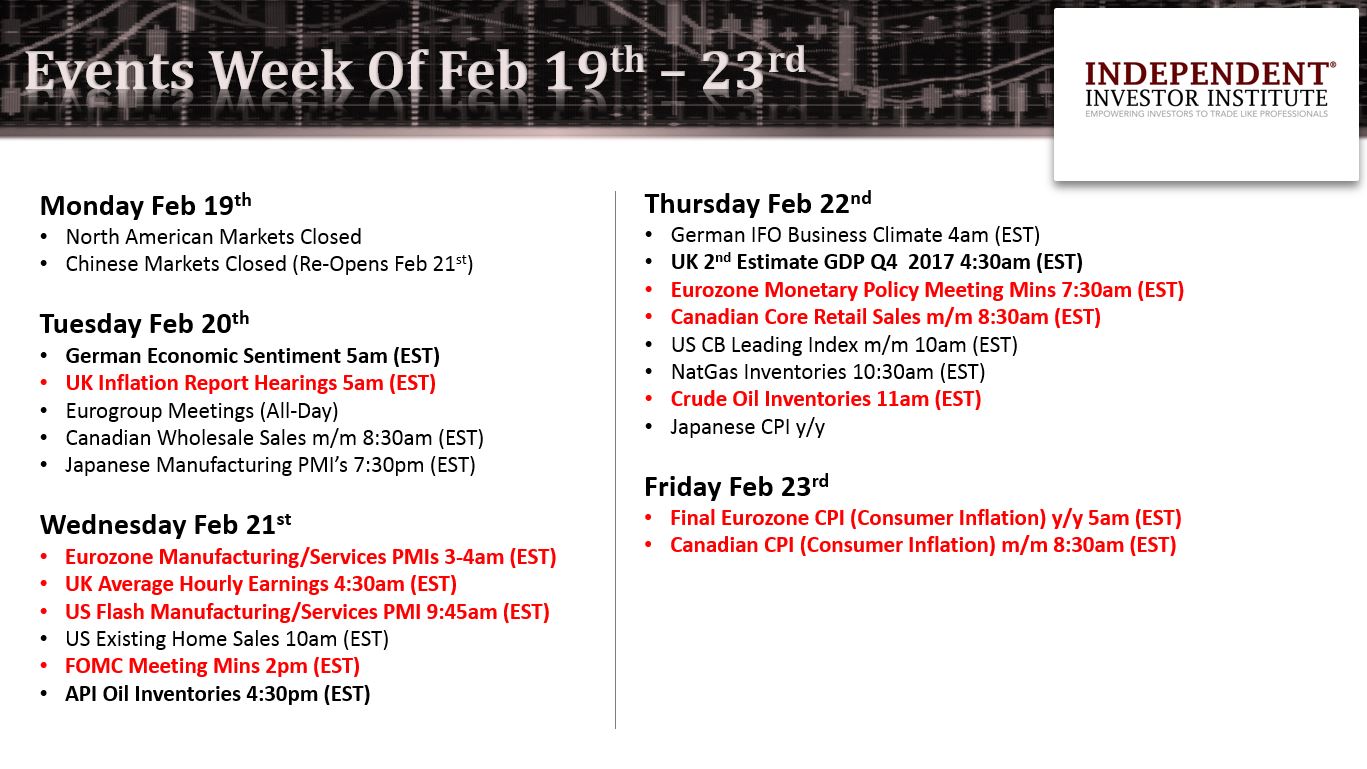

--Implication #3: All eyes will be on the release of the FOMC Jan. 2018 Meeting Minutes Wednesday at 2 pm (EST) and the ECB’s Meeting Minutes on Thursday, Feb. 22 at 7:30 am (EST).

If Mr. Market sees more hawkish-risk from the FOMC, we are likely to see a stronger USD and weaker US Treasury yields persist through Wednesday, allowing us to remain short/inverse precious metals and long defensive equity Sectors.

Join experts at the Independent Investor Institute online for a complimentary deep dive on markets. The Live Session starts on Saturday, February 24, 2018, at 12 pm (EST) – 3 pm: Click here to register free