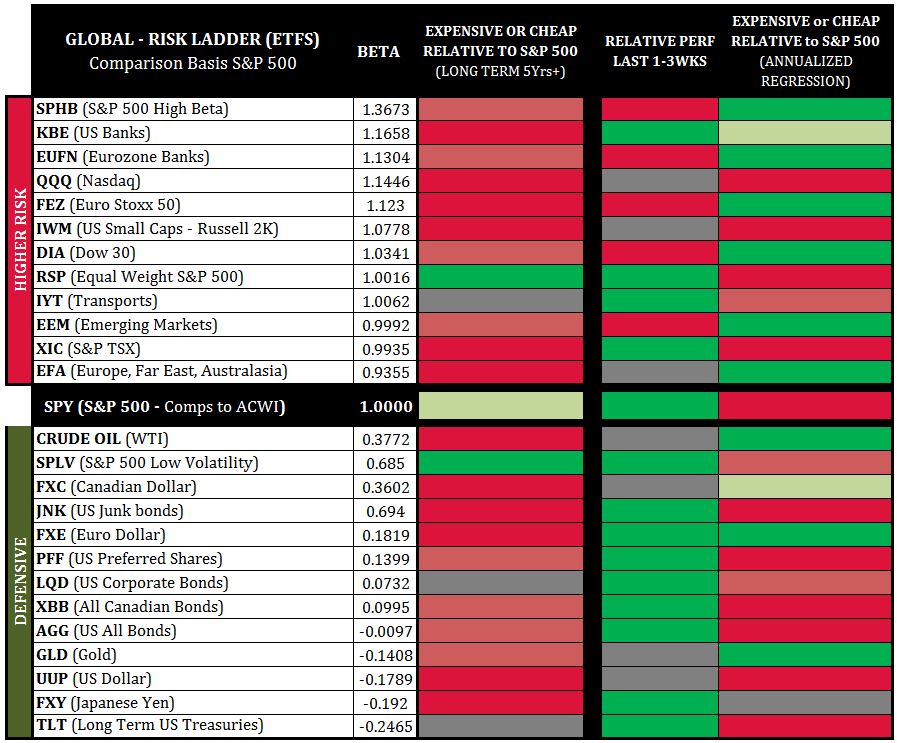

Currently, higher-risk asset classes polarized. Some very expensive, some very cheap. Cheap: Dow, Eurozone Financials, U.S. Banks, Hi-Beta, EuroStoxx 50, Emerging Markets, Eurozone Far-East & Australasia, Oil, writes Ziad Jasani Monday.

View my Market Strategy Session

Recorded: June 25, 11 am EDT

Duration: 1 hour

Global Risk Sentiment

Looking at the third column to the right in the chart, we see a comparison of higher risk asset classes and defensive asset classes back to the S&P 500 (SPY) on an annual basis.

Comparison to the S&P 500 creates a “risk-ladder” where market risk is considered neutral.

When we see more green above the SPY-Line (middle line) and more red below we have a general “risk-on” signal; and vice-versa - red above, green below would be “risk-off.”

Currently, higher-risk asset classes polarized. Some very expensive, some very cheap, indicative of the current geopolitical and tariff trade war issues.

Cheap: Dow, Eurozone Financials, US Banks, Hi-Beta, EuroStoxx 50, Emerging Markets, Eurozone Far-East & Australasia, Oil.

Expensive: Nasdaq, Russell 2000, TSX, S&P 500.

Defensive asset classes largely present as very expensive, in particular the U.S. dollar (USD) and U.S. Treasuries.

For equities to advance, the USD must soften up.

Overall, our Global-Risk-Ladder leans risk on into the week ahead, but there are notable concerns with how expensive Technology (QQQ), Small-Caps (IWM) and the S&P 500 (SPY) present.

This implies that any equity upside is likely short-lived (one week or at most two weeks before a move back down); or we have a few days of jitters (minor-risk-off) before risk-on presents.

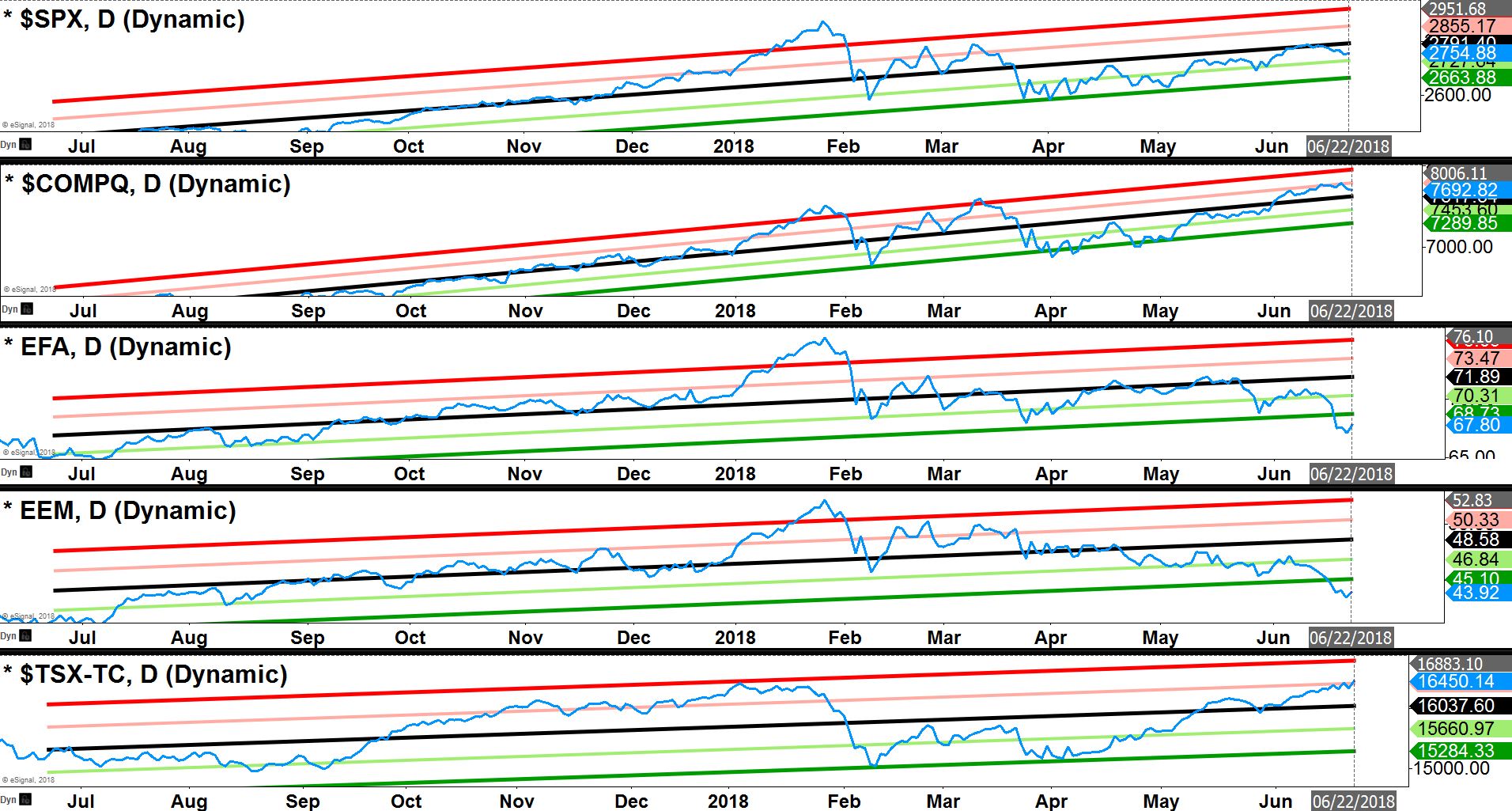

Major Index Direct Price Regression

When humans move very far away from “normal” routines they tend to come back “home.”

In markets, we call this “mean-reversion.” The channels to the right are direct closing prices day over day, enveloped in 2-standard deviation channels (“home” is the middle of the channel).

Currently, the Eurozone Far-East & Australasia (EFA) & Emerging Markets (EEM) present 2 standard deviations cheap, the S&P 500 (SPX) is slightly cheaper than neutral, while the Nasdaq slightly more expensive than neutral (COMPQ) and TSX present as 1 standard deviation expensive.

This presentation suggests that equities can advance, especially EFA & EEM, but a catalyst is required (i.e. USD down). At the same time this presentation can also indicate the beginning of a “new-normal” for EFA, EEM and roll-over dragging world markets with them.

To learn more about investing and trading within the cannabis space for the back-half of 2018, join us for a complimentary 3-hour Online Workshop on July 14, 2018 (12 pm – 3 pm EDT). Click here to reserve your seat.