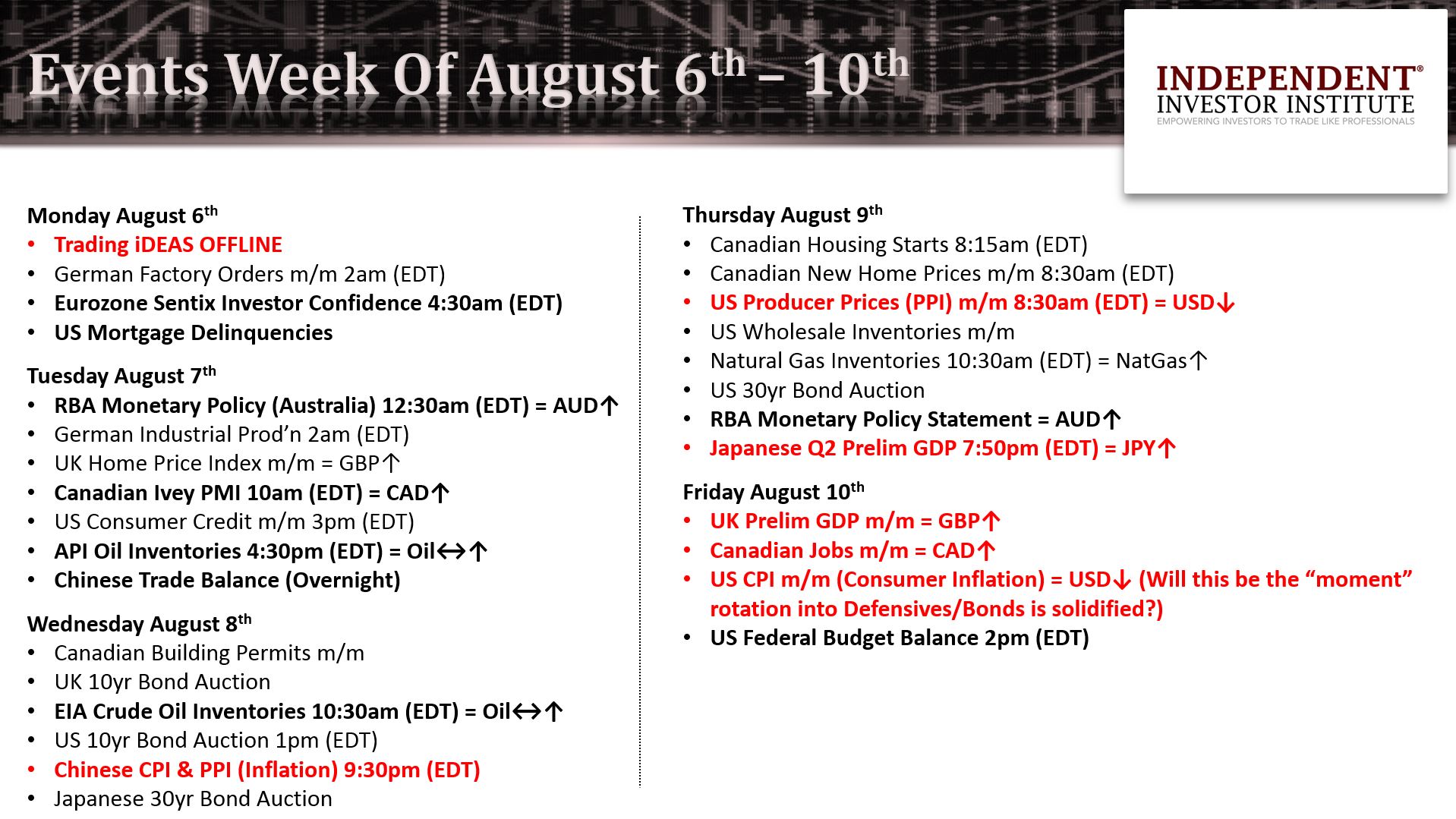

The Global Equity Market (ACWI): has bounced up off important support (ACWI $73.03) to end last week; fueled by Emerging Markets (EEM) & the Eurozone Far East & Australasia (EFA), writes Ziad Jasani Monday from Toronto.

View my weekly strategy session here

Recorded: August 3, 2018

Duration: 1:33:12.

This doesn’t mean “recovery” is clear for the trade war battered Chinese market (FXI), but the move comes with Base Metals and Precious Metals bouncing up off support structures and presenting in swing-low formation – which implies last week’s escalations are not making things worse.

Also, it helps that the PBOC came back to defend their turf and have prevented the yuan from sliding further (showing of confidence).

For Global-Equity markets to rise, we “must” see the World-Ex-US (ACWX) outperform North American Equities and within North America we must see Technology (QQQ, XLK, IYW, FNG) and the Dow (DIA) do the heavy lifting.

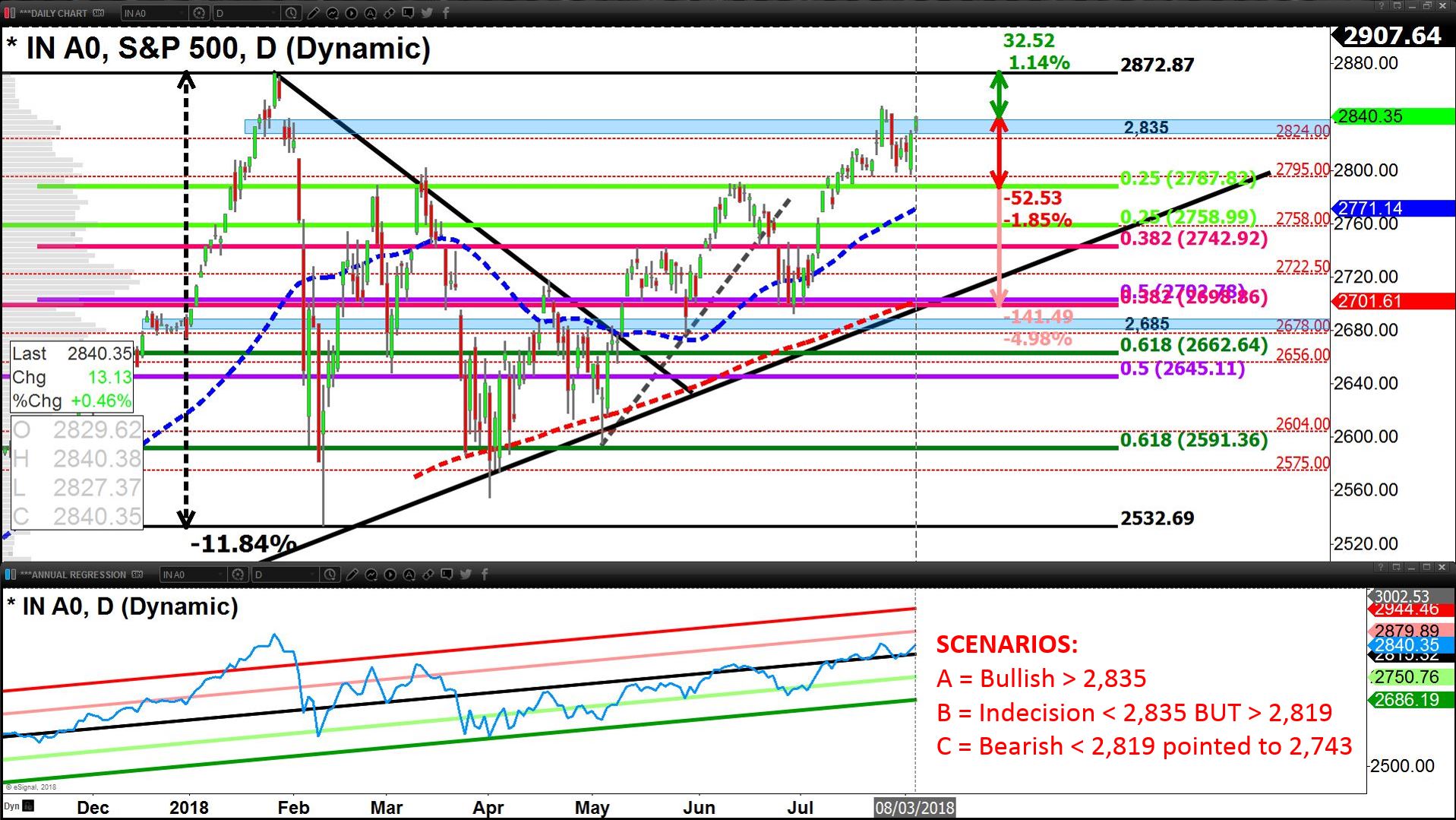

In general, any further rise in U.S. Equities is likely short-lived (days-to-a-week) prior to a more pronounced macro market swing-high formation that presents taking the S&P 500 (SPX) at minimum back down to its 50-day average (2,773).

Bottom line: While ACWI remains above $73.03 we are looking prices continuing to rise; however, we’re not willing to accumulate ACWX, EEM, EFA until they break-back-above their respective 50-day averages and we maintain the Hold decision if allocated on a swing-basis to the S&P 500 (SPY), Nasdaq (QQQ), Dow (DIA), Russell2K (IWM) and TSX (XIC-T).

US Equities

• AAPL has successfully mopped up Facebook’s mess and afforded the Technology sector (XLK, IYW, FNG) and the Nasdaq (QQQ) a strong bounce up off the bottom of up-trend and side-ways channels. To end last week, profit taking occurred but no clear signs of the money that rushed on AAPL’s earnings leaving.

• The S&P 500 (SPY) has been able to surmount a key decision-line 2,824 and hold above 2,830 (support); fueled primarily by Technology (XLK, IYW), Healthcare (XLV), Financials (XLF), Discretionaries (XLY), Materials (XLB), and Defensive Sectors (XLU, XLP, VNQ, IYZ).

• The U.S Treasury yield curve flattened to end last week on the poorer than expected jobs data allowing the already dislocated and expensive Defensive sectors to catch a bid alongside Bonds (TLT, IEF, IEI, LQD), but interestingly enough Financials (XLF) also enjoyed a bid. This implies the flow to defensives is likely to be short-lived; within 2-to-3 trading sessions we can expect a steeper yield curve.

• Trade war related spaces have bounced with the Chinese yuan (CYB) shoring up alongside Base Metals (DBB, CPER) and Precious Metals (GLD, SLV). The Dow (DIA) has surmounted a key line of resistance at 25,373, Materials (XLB) have popped above their 50-day average and present in swing-low, and Industrials (XLI) are holding above key support of $75.11. We can’t truly trust the move in trade war related areas (yet) as they are head-line/tweet driven making moves less predictable. Nonetheless we see are seeing strength that is encouraging.

• Oil had difficulty staying above its 50-day average to end last week and has seen inventory builds plague it throughout last week. As a consequence, we are seeing Energy Equities (XLE, RYE, XOP, XES) challenged to end last week. However, while XLE holds above $75.01 we maintain a Hold-decision as we see better chances for Oil to remain above $66.89 and give us a bounce, supporting the space.

Join Ziad at MoneyShow Toronto Sept. 15 when he discusses Portfolio Management Strategies for Active Investors. Information: ZiadJasani.TorontoMoneyShow.com