Stay away from homebuilders. As long as earnings continue to expand elsewhere, as they have been, housing woes should not harm the still-favorable investment climate, writes Marvin Appel. He's presenting at MoneyShow Toronto Sept. 15.

S&P Core Logic reported last week that U.S. home prices rose 6.2% from twelve months ago as of June 30. Although this is a smaller increase than the 6.4% increase reported as of May 31, home price inflation is still outpacing income growth. In addition, rising mortgage rates deal homebuyers a double whammy in terms of making homes less affordable.

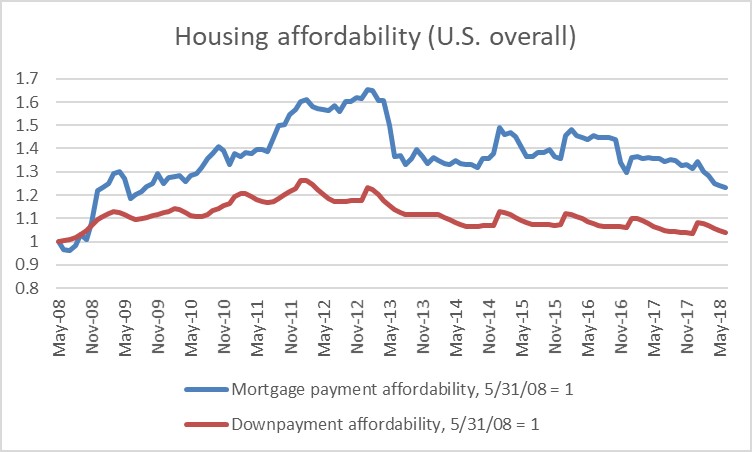

Home down payments (typically 20% of the purchase price) are now less affordable relative to median household income than at any time since the data began in 2008. Mortgage payments are less affordable than at any time since the end of 2008.

The sharp rise in home prices in recent years has not been accompanied by an increase in the supply of new homes. Rather, housing starts have been fairly stable over the past three years and have been falling in recent months. Similarly, pending home sales have also been falling consistently in 2018.

This all points to a crisis of affordability; homes are becoming more difficult to afford so demand is falling as prices rise. Unfortunately, this is not benefitting anyone.

Home building stocks are weak even as prices rise, in part because the costs of building a home are also rising, leaving little room for price reductions. According to the National Association of Home Builders, investment in new and existing single and multi-family housing accounts for 3%-5% of GDP, so stagnation in home building and home sales should have only a modest effect on the broader economy.

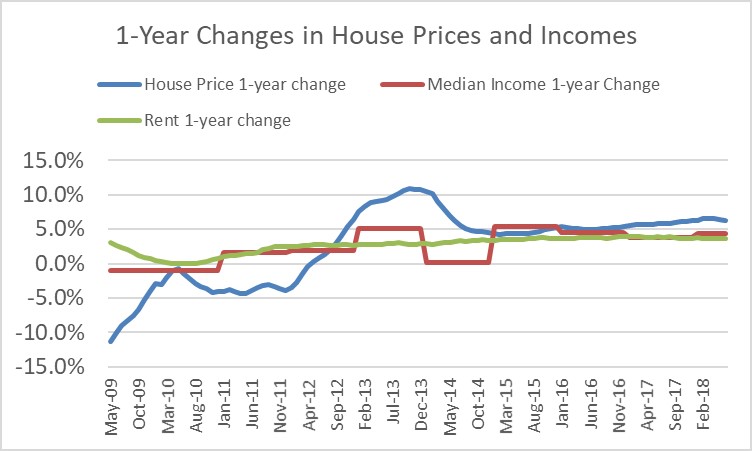

The charts below illustrate the situation, all based on data from 5/31/2008-6/30/2018.

Home prices are rising faster than incomes or rents.

The chart shows the trailing 12-month changes in home prices (Case-Shiller US National Home Price NSA Index), rent of primary residence (Consumer Price sub-index), and median U.S. household income in current dollars.

Ever since 2012, home prices (blue line) have risen faster than rents (green line). There was a big jump in income in 2015, but apart from that, home prices have consistently grown faster than incomes since 2012.

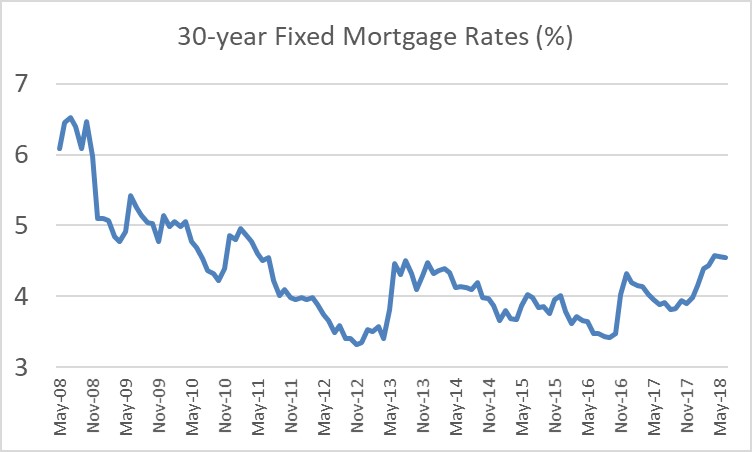

Mortgage rates contribute to rising homebuying costs.

Interest rates hit their low in mid-2016. They jumped strongly after the 2016 election and have made another leg higher this year.

Mortgage rates are now at their highest since 2011.

As a result of both higher prices and higher rates, home prices are becoming increasingly unaffordable. In the chart below, down payment affordability is just the ratio of median household income to home prices relative to the ratio at the start of the data series (red line).

This is at its lowest level ever. Mortgage payment affordability is the ratio of median income to a monthly mortgage payment calculated based on 30-year fixed rates, again relative to conditions at the start of the data.

Mortgage payments are less affordable than at any time since late 2008. In both cases, lower numbers mean that housing is less affordable.

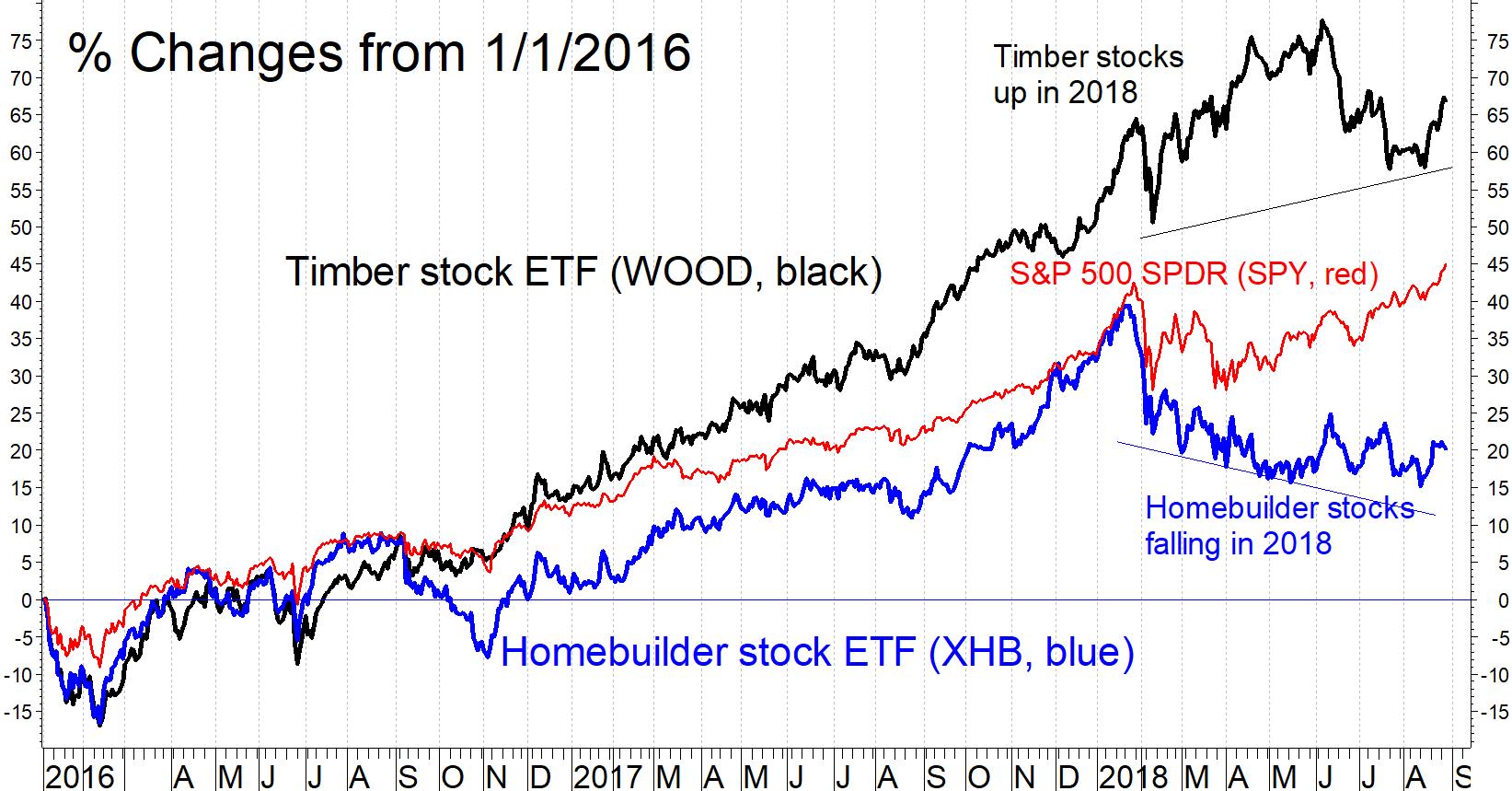

Homebuying stocks have stopped benefitting from higher home prices.

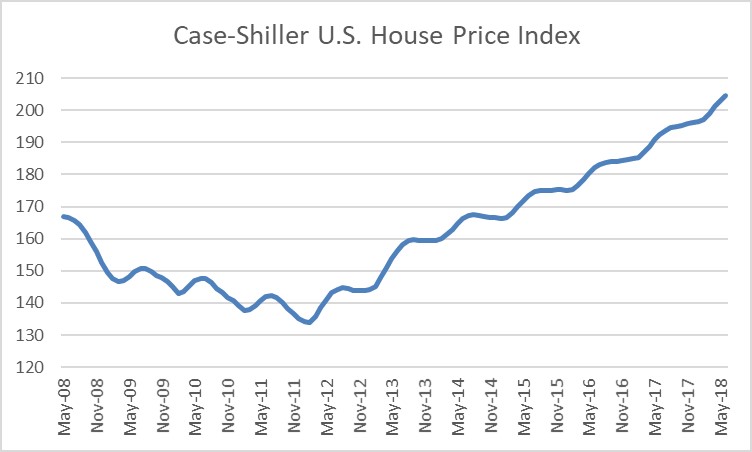

The chart above shows the Cash-Shiller House Price index, which has been rising briskly since early 2012.

2012 was a boom year for homebuilders, with their stocks up 57%, represented by the SPDR S&P Homebuilders ETF, (XHB).

Since then, however, they have overall lagged the S&P 500 but at least remained profitable until this year. Starting in 2015, lumber company stocks rose faster than homebuilders and faster than the S&P 500, reflecting increasing lumber prices that are a major expense for building houses.

The year 2018 has been a bust for homebuilding stocks, with XHB down 8.5%.

Lumber companies, however, are up almost 12%. Lumber companies are represented by the iShares Global Timber and Forestry ETF (WOOD). The chart shows the divergence in 2018 between WOOD and SPY (both up) and XHB (down).

Implications

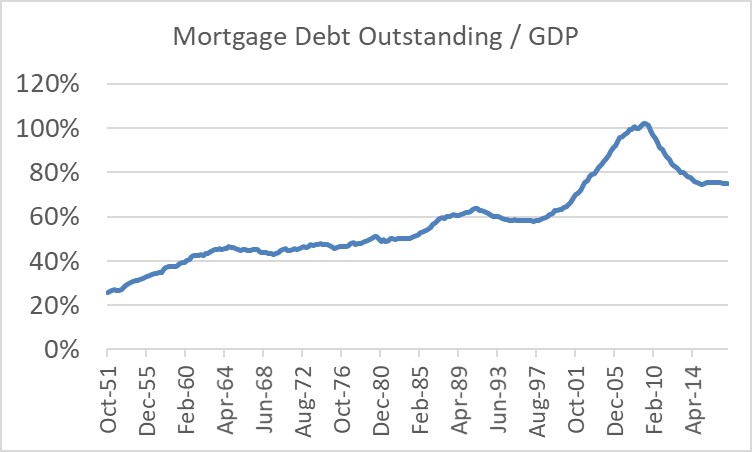

Difficulty in affording homes will act as a drag on this sector. Indeed, the chart below shows that the 58-year trend (from 1951-2009, source: St. Louis Federal Reserve) in which outstanding mortgage debt grew faster than the economy has come to an end.

Reduced demand for mortgage loans will probably help stabilize interest rates if federal budget deficits expand, as projected by the Congressional Budget Office.

Stay away from homebuilders. A sign that the shakeout will have been complete would be when WOOD also capitulates. Fortunately, the broader economy remains healthy and people are finding employment in other sectors, as evidenced by the low rate of unemployment and of new claims for unemployment insurance.

As long as earnings continue to expand elsewhere, as they have been, housing woes should not harm the still-favorable investment climate.

Sign up here for a free three-month subscription to Dr. Marvin Appel’s Systems and Forecasts newsletter, published every other week with hotline access to the most current commentary. No further obligation.

View a video interview with Marvin Appel and Dan Gramza on 2018 investing opportunities here.

Recorded: July 25, 2018 at TradersExpo Chicago.

Duration: 6:30.

View a video interview with Marvin Appel and John Bollinger on Bollinger Bands, when they are most useful for traders and about systematic investing pioneered by Dr. Appel and his father Gerald Appel here.

Recorded: July 25, 2018 at TradersExpo Chicago.

Duration: 4:31.