The consensus expectations for Friday’s headline nonfarm payrolls data point to around 165,000 jobs added in January, says Fawad Razaqzada, Market Analyst, Forex.com.

Ahead of Friday’s U.S. Bureau of Labor Statistics Employment Situation Report, it was the Federal Reserve’s Open Markets Committee (FOMC) report that caused volatility in the markets on Wednesday. The central bank successfully triggered a stock market rally that helped to push the major U.S. stock indexes to new highs for the year, while the U.S. Dollar Index was pushed back towards its early January lows where it rebounded on Thursday ahead of the data. Therefore, Friday’s jobs and wages numbers may turn out to be not as significant in terms of their potential market impact as investors will still be assessing the Fed’s apparent U-turn in its monetary policy stance – unless the data turn out to be significantly strong or significantly weak.

Fed turns dovish

We had already anticipated that the Fed and its chairman Jay Powell may very well deliver a dovish surprise and as it turned out, that was indeed the case. This should not have come as surprise, but the markets’ reaction suggests that the Fed was perhaps more dovish than had been anticipated. All of a sudden, the central bank’s focus has shifted from a bias towards hiking rates to a completely neutral and data-dependent outlook. The FOMC will now be “patient” in determining future “adjustments” to interest rates given “muted inflation pressures.” Reading in between the lines, the Fed may even lower interest rates should the economy deteriorate, as “adjustments” could mean a rate increase but also a cut. Powell also confirmed reports that the Fed is evaluating its balance sheet strategy and will be finalizing plans at the coming meetings.

Strong employment data may be shrugged off

Given the renewed weakness for the dollar, if the jobs and wage data were to disappoint expectations badly then this will further reinforce the Fed’s cautious outlook on the economy and reduce the possibility of rate increases even further. However, a positive surprise will probably not cause too much of a reaction as investors are aware that the jobs markets has already been a strong area of the economy. In other words, we expect the dollar to respond more significantly to poor than positive data.

Current NFP Expectations

The consensus expectations for Friday’s headline nonfarm payrolls data point to around 165,000 jobs added in January, after December’s much stronger-than-expected 312,000 print. The January unemployment rate is expected to have remained unchanged at 3.9%. In terms of wage growth, average hourly earnings are expected to have increased by 0.3% month-over-month after last December’s 0.4% increase.

Jobs Data Preceding NFP

Predicting the outcome of the nonfarm payrolls report is never an easy task, and this one is practically impossible to forecast with any degree of confidence because some of the most important leading employment indicators that we usually take into account won’t be released until after the jobs report is published. The ISM manufacturing PMI and its employment index will be released later in the day on Friday while the headline and employment component of the dominant services sector PMI will be released next week.

Meanwhile the unrevised Jobless claims figures released throughout January have averaged 222,400. This has been on about 2,600 above the average expectations for the January releases, and marks an uptick from the previous months’ averages. It is possible that longest U.S. government shutdown in history may have impacted employment-related claims.

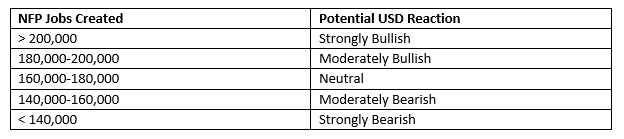

Forecast and Potential $ Reaction

Given the above considerations, our target range for the nonfarm payrolls for this month is tilted to the middle of the average expectations. With the consensus expectations of around 165,000 jobs added in January, our target falls in the range of 150,000-180,000. Though the U.S. dollar will likely be moved by a host of other fundamental factors, any headline jobs outcome falling above this range should give the dollar a boost, but we think this may be short-lived given the Fed’s dovish shift. A result falling within the range will unlikely make much of a significant impact, unless the wages show a big surprise. And any reading that falls significantly below this range could result in a sharp dollar sell-off.

NFP trade ideas

In the event the jobs and crucially wages data beat expectations, then we would favor looking for short-term bullish setups on the dollar against the likes of the British pound given the ongoing Brexit uncertainty in the UK. But if the jobs data turns out to be very poor, then we would favor looking for bearish setups on the dollar against the likes of Japanese yen in “risk-off” conditions (falling stock prices) or Aussie dollar if it is “risk-on”.