The lesson of the day so far is that President Donald Trump’s delays on tariffs are good for global markets, says Bob Savage.

The lesson of the day so far is that President Donald Trump’s delays on tariffs are good for markets while UK Prime Minister Theresa May’s delays on a UK vote for her deal for Brexit until March12 is bad. What is the difference? Are expectations about denials and time interlaced with politics?

The Trump Tariff delays, Trump talking down North Korea denuclearization deals and China Banking and Insurance Regulatory Commission (CBIRC) forcing increased lending to the private sector by 30%, drive shares 5.6% higher in China, the yuan to seven-month highs and crude oil back to the highs for the year. The CBIRC declared victory on its debt control targets today. “After two years of work, various financial disorders have been effectively curbed,” Wang Zhaoxing, vice chairman of the CBIRC, told a news conference.

The lack of other big news stories leaves markets watching technicals rather than fundamentals for the next clue. The lack of supportive economic data hasn’t been the problem in 2019, rather it’s the reaction function of central bankers that on the margin drives and the all-clear from the FOMC to the PBOC to the ECB is in play this week. Delaying rate normalization has brought relief and comfort as the story reverts back to slow but steady growth everywhere without the burning inflation fears or the bears of recession. This won’t last as the business cycle can’t be denied but merely delayed. The best barometer for understanding the price action today is in the commodity linked currency world where hope for a trade deal overrides fears of deflation and housing bubble pops – with the Australian dollar at the front and center of the storm - wait for .7275 to confirm the risk breakout.

Is the problem in Europe more than just China growth?

The bounce back in the euro today and the relief in the periphery of Europe are connected back to the gains in China. The hope for a Trump trade deal drives away fears about an EU car tariff and restarts the hope that Germany and Italy are going to turn their growth woes around. The standard argument is that China growth matters more to the world than the United States. The U.S. divergence in 2018 is taken as proof of this point.

The problem with this logic is that the U.S.-China trade talks are not just about trade. A story in Project Syndicate on Feb. 18 states: “The US is prepared to sacrifice its economic relationship with China; because the risks posed by the two powers’ conflicting national interests and ideologies now overwhelm the benefits of cooperation.” The article adds: “Likewise, for China, the trade war has exposed the strategic vulnerability created by overdependence on U.S. markets and technologies. Chinese President Xi Jinping will not make the same mistake again, nor will any other Chinese leader.”

Europe is that alternative and it plays a significant role in balancing out the U.S. push.

Conclusions

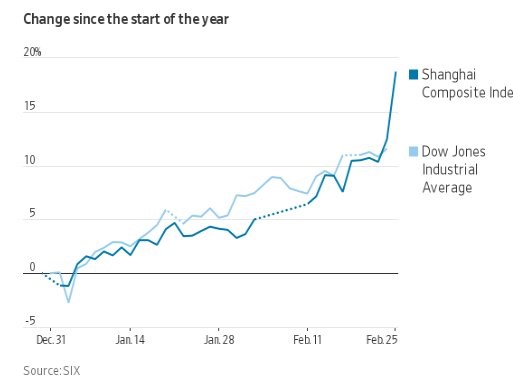

Is the China share market going to help or hurt the U.S. rally? When you consider the rally in Chinese stocks since January, the performance looks stellar and logical given its underperformance in 2018. The knock-on effect for Europe has been more powerful than for the United States, even as the pressure for a Trump deal leads the headlines.

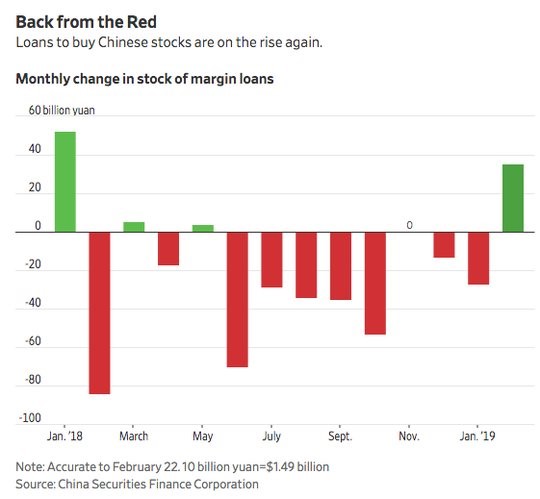

The issue behind the surging Chinese stock is linked to debt and this is where U.S. and China fears combine. Margin loans in China are driving much of the rally. This is the unintended consequence of the PBOC policy push.