The S&P 500 (SPX) is flexing its muscle with a breakout above 4,000. However, the rest of the market is not joining in on the fun, says Steve Reitmeister, editor of Reitmeister Total Return.

For example the small caps in the Russell 2000 are actually down since the S&P breakout began to start April.

To me this is just a sign that the bull market is a bit lopsided. The likely next step is for this to reverse. For the large caps to take a breather while smaller stocks, often with growthier outlooks, to take the baton and run ahead.

If true, then it bodes well for our portfolio, which leans smaller and growthier and higher beta'ier (yes, I know that's not a real word...just roll with it ;-)

We will talk about this market action, economic events and updates on our portfolio of 11 stocks and three ETFs in the commentary that follows.

Market Commentary

As shared in the intro, the headlines read bull run...but small-cap investors are calling BS.

That’s because the large caps are running ahead on their own. That is actually quite odd as most breakouts to new heights are a sign of bullish zeal on the part of investors. That usually comes hand in hand with smaller, growthier stocks leading the way higher. That is simply not happening at this time as the Russell 2000 and the Mid-Cap indices are actually in the red in April all the while large caps are bathed in green.

No, I am not saying this is a sign of trouble. Just an oddity that will likely be rectified by a rotation in the other direction. Meaning that small- and mid-caps will likely outperform in coming weeks. If so, I suspect that will be very good for the RTR portfolio to push to new heights.

There is not much new information to report of late. The economic picture continues to improve with the one main report of the past week heading higher. I am referring to the NFIB Small Business Optimism index rising from 95.8 to 98.2.

The reason this report is so important is that this group was the most harmed by the coronavirus turndown. So as their optimism for the future improves, the more likely they are to hire more employees and invest more on equipment and services for their business. This is truly the key to the economic engine of the US and it continues to head back in the right direction.

On top of that the government wants to throw another couple trillion on the fire with a forthcoming infrastructure bill. In general, infrastructure is a pretty bi-partisan concept with broad support. The key is where that money will be spent leading to a typical DC sausage-making process to churn out the final bill.

Plain and simple, the economy was already on an upward path. So any additional stimulus from the government only adds to the upside potential of the economy, and stock market for that matter.

The main risk of these efforts is causing inflation to spike higher, which indeed was showing up in recent reports.

+2.6% YoY for CPI Core Inflation

+3.1% YoY for PPI Core Inflation

Both of those are running hotter than the typical 2% target of the Fed. However, there is some noise in these numbers because the economic implosion of the coronavirus back in March/April of last year is by its very nature deflationary. So we are looking at a year-over-year picture versus a very soft time for inflation.

On the other hand, don’t overlook inflation either. Typically that goes hand in hand with an improving economy. And it certainly goes hand in hand with ROBUST government spending (if you get the hint that I think the government is spending too much these days, then you are right. But then again, both parties have been handing out money like candy from a bottomless Halloween bowl for longer than I have been alive. So don’t think I am casting aspersions at one party or another. I am casting aspersions at ALL POLITICIANS...but lets not digress any further ;-)

The point is that inflation IS on the rise, which begets higher Treasury rates, which is still good for two of our existing rate trades (TBT & KRE). Yes, neither has been that robust of late. Just remember that investors move in advance of most situations. In this case, it was obvious that rates would move higher and investors pressed hard on both investments pushing them substantially higher.

After this pause in share price action for TBT and KRE I still fully expect them to be outperformers in the future. That is why they remain in the portfolio and would advise newcomers to RTR to take their rightful allocation in these positions.

Summing it up, we are still most certainly in a bull market. Its just that the action is a bit skewed towards large-caps of late, which likely gives way to a rotation to smaller/growthier stocks in the weeks ahead. That outlook bodes well for our portfolio. Now let’s dig into more insights on those individual stocks & ETFs below...

Portfolio Update

Lots more turnover in the portfolio than usual with four trades in the past week. That was not planned. Just sometimes I get in a mood where I just feel things could be better. Like you ignore your messy closet for several months. Then one day you decide to dig in and re-organize. It’s the same kind of impulse here.

But also earnings season is real a “moment of truth” for every stock. So in the case of RPM it came up short on their day of judgement and thus needed to be replaced.

This is another way of saying that earnings season has just started and we will see more and more of our companies get sworn in for their testimony. Those found guilty of wantonly poor results will be tossed out of the RTR portfolio making way for more virtuous and healthy positions to be added. So be prepared to act when the time comes.

Now let’s give some additional updates on the positions inside our portfolio:

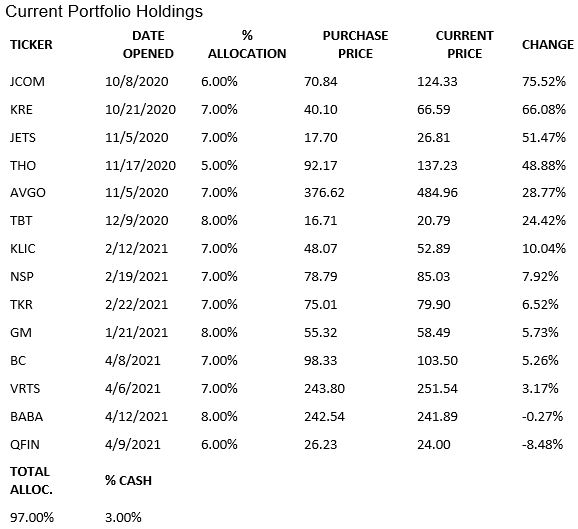

Alibaba (BABA): We were in BABA for a long time before all the regulatory issues started. Thus we were compelled to sell on 9/8/20 when it was clear the stock would be dead money for a long time. So we sold at $269.59 for a nice 52.7% gain.

Gladly we bought back in today in the low $240’s and also saved seven months of wasted time. All in all a good move to leave the stock and come back. And a good reminder to folks that if there are dark clouds hanging over a stock it simply will not perform well. Thus, no matter how much you LOVE the stock (and I most certainly loved BABA)...you have to walk away and only come back when the coast is clear. Otherwise you will likely be sorry. This is good lesson to keep in mind for the future.

So at this stage the Wall Street community is pounding the table for folks to rush back to shares. With that has been a flurry of analyst upgrades and target price raises with the average around $320. That is ample upside from our current perch. However, I suspect that will prove to be too low a target when all is said and done with $400-500 being its likely destination 12-24 months down the road. And if BABA is indeed the Amazon of China, then this should become a stock to hold onto the long term with great expectations of years of outperformance to come.

Brunswick (BC): Speaking of new picks, BC also is looking good out of the gate as it has mounted an attack to break above $100. Monday was the first close above with a burst to $102.32. And then today it pressed even higher to $103.50. At this stage I suspect it will climb to around $110 coming into the next earnings report. Just nice seeing this boat manufacturer make positive waves in our portfolio.

General Motors (GM): Shares did finally break below $60 on Friday and stayed below the next two sessions. However, analysts like John Murphy from Merrill Lynch are unfazed leading him to reiterate the Buy rating with a raised target of $72. Right now the main thing holding shares down is the temporary concerns about a semiconductor chip shortage that will lead to fewer cars produced this year. Same problem exists for Ford and the others. No doubt they will start to solve this problem and the cars will roll off the assembly line into the hands of eager buyers. When there are signs of the chip shortage easing, shares will rev up quickly to higher levels.

Speaking of Chips...(AVGO & KLIC): Both of these companies have seen an ample price increase the past month. Part of that was bouncing back from the broad tech sell off. Another part is what we discussed above.

Chip shortage + high demand = FAT profit margins.

The above equation tells you why we will be staying in these shares a good while longer. Then throw on top that in the current infrastructure stimulus bill is proposed $50 billion to expand semiconductor manufacturing in the US to be more self-reliant than in the past on chips (most from Asia). No doubt KLIC would benefit from more money being spent on chip-fabricating equipment.

Timken (TKR): Shares were hot out of the gate when we added in late February and immediately broke about above $80 to a high of $87.92. However, since then it has underwhelmed leading to a new test of support at $80. All signs point to shares being worth $95-100. But just because one says that doesn’t mean others will agree. So at this stage I want to see shares respond better and start to outperform going forward. If not, then we will consider switching to another stock that offers us a more timely response.

J2 Global (JCOM): Normally JCOM is stealthy in the way it steadily rises over time. However, on Thursday it was leading the way in the RTR win column with a +3% return. And today it lead the way with a +2.2% session. And now it proudly waves the checkered flag that it is winning the RTR portfolio race at +75.52% since inception. Indeed I suspect it will be a 100% winner when all said and done. However, JETS and KRE will give it a run for the money at the top of the portfolio over time.

360 Finance (QFIN): QFIN is in almost all regards the opposite of JCOM when it comes to price action. In this case we are talking about SUPER VOLATILE shares. That is how it tumbles on Monday right after it rallied 10% on Thursday of last week. This is why we have a smaller allocation so not too much money is at stake.

Plain and simple, this is the kind of speculative stock that you stick in the back of your portfolio and don’t focus on too much. And if you give it a chance to breathe the volatility over time should work in your favor as it climbs back closer to its fair value targets. However, on the side we do need to have a limit on downside. In this case it has to be more than the traditional 10% limit. In this case we need to be willing to see a 15-20% decline. But more than that is unacceptable. You, of course, can follow a different path if you want. Just wanted you to know where I was coming from.

Virtus Investment (VRTS): Let’s end on a good note with one of newest picks that is strong out of the gate rising +4% in the first few sessions before giving a touch back today. To me this choice of VRTS was like pressing the easy button with TBT.

Higher Inflation > Rates Rise > TBT Rise

Market Goes Up > Virtus Assets Rise > Management Fees Rise > VRTS Shares Rise

My guess is that at less than $2 billion market cap that most other investors used the above equation to swarm to larger money management firms. Yet that is what is so awesome about our reliance on the POWR Ratings system. Everyday it scans the universe of stocks with equal eye to small-caps, as well as the largest shares. This often leads to unearthing hidden gems with stellar fundamentals, but with lagging share price. This creates a glorious opportunity for us to step in and have outsized odds of outperformance.

That certainly was the case here with VRTS. And expect more of the same as we rely upon the POWR Ratings to propel our portfolio going forward.

Closing Comments

Hopefully the lopsided market once again tilts back in our direction in coming weeks to broaden out our lead over the market this year.

Learn more about Steve Reitmeister at StockNews.com