Stocks lurched to new highs. Yes, I said lurched. Because there was nothing smooth about it given so much sector rotation and volatility that it makes it hard to see the trend, says Steve Reitmeister, editor of Reitmeister Total Return.

But that lack of clear trend is in fact, the trend that exists. Meaning this swirling, twirling action has been with us since March. And til proven otherwise that is the trend in place. You should count on that going forward.

We will talk more about that...and how it affects our trading strategy...and updates on our individual positions in the weekly commentary that follows.

Market Commentary

Over the last several months, I and many other market commentators, have used the following terms to describe recent stock market activity:

* Volatile

* Consolidation

* Sector Rotation

* Rolling Correction

* Frankenstein (fits in with the lurching theme in the intro)

All of that is true...but still a bull market. Thus, if you read too much into the daily tale of the tape you will misread what the market is telling you. Because today’s winner is likely tomorrow’s loser and anyone trying to catch some momentum in that trend is likely going to be fairly disappointed.

This is where we come back to other themes discussed in recent commentary. And that is just to stay focused on the fact that it is a bull market. More specifically, a bull market based on two main drivers:

1) Low bond rates...like really low...like historically low and an absolute thumb on the scale for the stock market (like Paul Bunyan’s thumb).

2) Economy still making its ways back from the coronavirus crisis.

The first part about low bond rates should just have you bullish day in and day out because odds are so ridiculously skewed in our favor. The second part about the improving economy says that, in general, go for more risk-on and cyclical stocks. That’s because they should sport faster earnings growth at this stage, which generally leads to higher share price appreciation.

That certainly has been the game plan for the RTR portfolio this year. Unfortunately, that doesn’t work every day, week, or month given the all the volatility. But over time it proves its merit with our strong outperformance on the year (+26.16%).

Reity, wasn’t our gain at +29% YTD on Friday?

Yes, it was. Which only proves my point about the violence and short-term illogic of this market. But if you panic and think the strategy is not working because of these short-term hiccups, you will miss those stretches where we absolutely crush it...like last week...and probably once again right around the corner.

Do I like this kind of market?

No...I absolutely hate it.

But hating it doesn’t mean I am scared of it. Or running away from it. Just that I prefer stock action that is less volatile and more rational.

Gladly we do understand the trend in place and are playing our hand quite well. Now let’s move on to the...

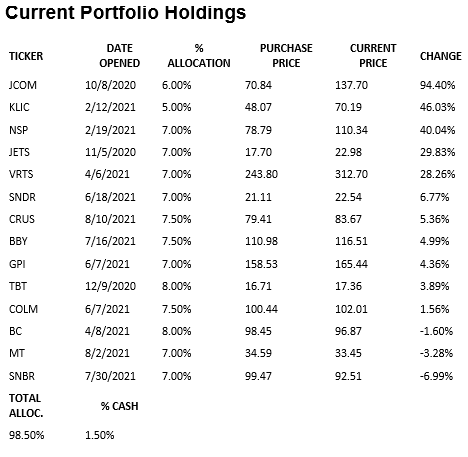

Portfolio Update

Insperity (NSP): This is the third straight close above $110. So yes, it is possible it is ready to continue its run higher. However, I suspect that it is more likely to consolidate around $110 a little longer to gather up the strength for the next leg north.

Plain and simple, if you believe the economy is rebounding (which is obvious) and more people will get back to work (in motion) then it is hard not to appreciate the ample positives of these shares. However, if NSP does make a run at $120-125 before the next earnings report I may be tempted to take profits on 20-30% of our position. If not, then more than happy to go into the next quarterly announcement with a full allocation given that the odds of success are skewed in our favor.

Virtus Investment Partners (VRTS): The recent move below $300 has been firmly rejected and shares look ready for an elongated run above $300. Again, the key driver of their growth is that as the stock market goes up they have more assets under management, which begets higher assets under management fees, which begets higher profits. This is why the average target is still at $400 and we have no plan to sell anytime soon.

Brutal Day for Consumer Discretionary Stocks, But...(BC, BBY, SNBR). What a nasty sector rotation out of these stocks Monday. And indeed, all their peers were hit with equally ugly red arrows. Why? Best I can tell it was from the weak Consumer Confidence report, which blended with recent weakness in Retail Sales and Consumer Sentiment reports has some folks questioning the strength of the consumer.

I still find these stocks attractive and perhaps worth a little time spelling out the positives of each next...

Best Buy (BBY): They served up a 60% earnings beat.

Repeat...they served up a 60% EARNINGS BEAT!

That is not supposed to happen for an established large cap like Best Buy. But it does tell you how conditions are quite favorable along with their stellar management in recent times. This has earnings estimates exploding higher and analysts fawning over them with raised price targets. The average target is now up to $135, but some top analysts are saying $150 or even $157 is more appropriate. So, we can sit tight with our shares below $120 knowing there is a lot of runway ahead.

Brunswick (BC): 5-star analyst, Eric Wold of B. Riley, cannot believe that investors continue to overlook the positives at BC. That is why late last week he reiterated his Buy rating including a street high $135 target price. The logic in that valuation makes a heck of a lot more sense to me than the dive back under $100 Monday. I sense that ridiculousness will soon be corrected.

Sleep Number (SNBR): Shares almost fully erased the red ink until it got beat upside the head Monday. Just like BBY and BC I can point to a strong earnings report in the bank. And lots of analyst love. But if I am being honest, this is my least favorite of the 3. So, if it continues to stumble around I will cut it loose to try our hand at another stock that may be more timely.

That is a great lesson for all investors. We go into these trades with the benefit of our POWR Ratings system that does a deep dive on 118 different factors putting the odds in our favor. And beyond the POWR Ratings, the other catalysts behind these three companies are relatively equivalent (strong earnings outlook and undervalued). But that doesn’t mean that each stock will respond in equal fashion. That is where we do need to watch the action of the shares. Not so much to be hypersensitive to every little ripple and sell in a panic too early. It’s important that we are patient on the one hand, but realistic enough to know when shares have been given ample time, yet not responded appropriately. We are not there yet on SNBR...but will be there soon. Hopefully SNBR responds favorably to this “tough love” speech and puts any negativity to bed.

Schieder National (SNDR): Fitting in with the theme above, I wanted to share that early last week I wrote a note to myself to keep a close eye on SNDR as I was a bit surprised it was not rising more in the face of their sparkling earnings report. Literally the next day shares started to press higher and has kept that momentum. My bet is that it will get closer to $25 into the next earnings report. if they do beat again then we are looking at $30 by year's end.

Kulicke & Soffa (KLIC): Shares touched $70 back on August 10 and then got a case of altitude sickness. Now shares have closed above that mark for the second straight day increasing the odds that a new breakout is unfolding. And why not? They gave us a stellar earnings report that has analysts downright giddy with upside expectations. Given the still ongoing chip shortage, which begets higher demands for semiconductor equipment, then I would not be shocked if shares are north of $100 by early next year.

Closing Comments

Volatile or not, this bull market has worked in our favor. I fully expect that to remain the case for a long while in the future. Keep that notion in mind so that it gives you the patience needed to ride out any of these short-term storms.

Learn more about Steve Reitmeister at StockNews.com.