The bull vs. bear tug of war is at another critical juncture as they battle over 4,000. The two previous skirmishes were won by the bears, states Steve Reitmeister of Reitmeister Total Return.

I am referring to the big rallies that ran out of steam in mid-August and early December. The hawkish Fed was the main catalyst each time to swing things back to the downside. Will that be the case once again after the February first Fed announcement? That is the topic that most deserves our attention at this time and will be the focus of this week's Reitmeister Total Return commentary.

Market Commentary

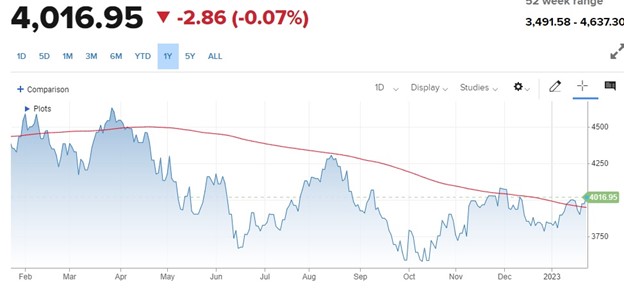

The boiled-down version of today’s commentary can easily be labeled: Stock Buyers Beware! That’s because price action is saying one thing...but fundamentals are saying another with the final verdict likely coming after the February first Fed announcement. Now let’s go back to the starting line by evaluating this picture of where we stand now with a possible breakout above the long-term trend line (aka 200-day moving average in red below).

Yes, it appears that we have a breakout forming at this time. However, see how similar events happened back in late March and late November before the bears took charge once again. Chartists will also note that this is still quite bearish. First, because we are officially in a bear market. We would need to cross above 4,189 to state that a bull market was in place.

Second, we have a series of lower highs which is a negative trend until it is officially reversed. To be clear, this could be the forming of a new bull market. And you should never fully ignore the wisdom of the crowd as it appears in price action. Yet viewing this without the context of the fundamental landscape is a bit hollow. So, let’s switch in that direction where we have another crossroads. That being investors who are solely focused on the state of inflation (and likely future Fed actions) vs. those who see a recession forming.

The main theme is that, yes, inflation is coming down faster than expected. But before you cheer that good news it is BECAUSE there is a recession forming which is normally the root cause of bear markets. That recessionary forecast only grew darker this week starting Monday with a worse-than-expected -1% reading for Leading Economic Indicators. Check out this quote from Ataman Ozyildrim, Senior Director, Economics at the Conference Board (who creates this indicator):

"The US LEI fell sharply again in December—continuing to signal recession for the US economy in the near term. There was widespread weakness among leading indicators in December, indicating deteriorating conditions for labor markets, manufacturing, housing construction, and financial markets in the months ahead. Overall economic activity is likely to turn negative in the coming quarters before picking up again in the final quarter of 2023."

Next up to bat was the S&P Composite PMI Flash report on Tuesday coming in at 46.6. This was an even-handedly bad showing as Services at 46.6 was on par with the nasty 46.8 showing for Manufacturing. (Remember under 50 = contractionary environment).

These poor economic readings make it hard to be bullish at this time. Even worse is that we are running headlong into the next Fed announcement on February first where they are likely to repeat their “high rates for a long time” mantra. Bulls keep jumping the gun expecting a Fed pivot only to get smacked down again. Such was the case in mid-August when the 18% summer rally ended with the famed Jackson Hole speech from Powell had us making new lows in the weeks ahead. Then the October/November rally ran out of steam when Powell poured cold water on bullish aspirations with the higher for longer rate expectations.

To be clear, the Fed no doubt sees the same signs of moderating inflation. And yet just as clearly, there will be no change in their stance given how the higher for longer mantra was repeated all month long at nearly every Fed speech in January including similar sound bites from Powell. These guys are singing from the same song sheet on purpose. That is part of their mission to provide clarity to all market participants. And thus to expect them to abandon the higher for longer mantra as soon as the February first announcement is borderline insane.

Yes, they likely will downshift to quarter-point hikes. That seems appropriate at this time. But that is greatly different than ending rate hikes or going lower in time to stave off the formation of the recession at hand. To boil it down, bulls could stay in charge of price action going into the February first Fed announcement. This could have stocks looking like they are breaking out with some investors getting drawn in by serious FOMO.

However, going back to the main theme of this article, I would say strongly; STOCK BUYER BEWARE! Simply getting bullish now coming into that February first announcement given the facts in hand seems quite risky. The bears still have the upper hand til proven otherwise. If, by some amazing stretch of the imagination, the normally slow and steady Fed officials do a 180-degree turnabout to become undeniably dovish on February first, then certainly join the bull party that afternoon.

Long story short, the risk to the downside is greater than the risk to the upside which is why I remain entrenched in my bearish portfolio and recommend the same to others.