Recently, the semiconductor group fell by more than 9% on a Friday, bounced 5% on a Monday, then rolled over again on a Wednesday. The answer isn’t that the fundamentals changed three times in five sessions. It’s the plumbing, counsels Lance Roberts, editor of the Bull Bear Report.

Leverage is the real issue underneath this market, and it’s worth explaining WHY an index this large now trades like a momentum stock.

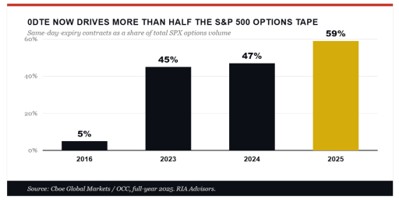

Start with the options tape. In 2025, zero-day-to-expiry contracts made up roughly 59% of all S&P 500 Index (^SPX) options volume, about 2.3 million contracts a day. Back in 2016, that share was 5%.

When more than half the flow expires the same session, dealers hedge in real time, buying strength and selling weakness straight into the close. That mechanic doesn’t start a selloff. It pours gasoline on whatever is already moving, which is exactly why the round trips have been so violent.

Underneath those options sits a record pile of borrowed money. FINRA margin debt hit an all-time high of $1.3 trillion in April, up better than a third in a year. It now runs near 4% of GDP against a long-run median closer to 1.5%.

The retail crowd has fresh tools, too. There are about 377 single-stock ETFs now, 276 of them launched in 2025 alone, many of them levered 2x to a single name. Make no mistake, these are accelerants, not investments.

Here’s what should keep you honest, though, because it cuts against the bearish story. If this were the start of something systemic, credit would be screaming. It isn’t. High-yield spreads sit near 300 basis points, close to the tightest since 2007 and a fraction of the 490 average.

The bottom line: Don’t confuse violent with fragile, and don’t confuse quiet credit with safe. Keep your hedges, trim what’s levered, and watch high-yield spreads. As long as they stay calm, this is a structure-driven shakeout. The day credit widens alongside the CBOE Volatility Index (^VIX), the housekeeping becomes something worse.