Fundamental value investors like me tend to get jealous when a new growth investor comes on the scene and generates huge returns, observes Jack Forehand, quantitative investing strategist and president of Validea.

We go through various stages of denial as we watch their returns far exceed our own. We point out the overvaluation of their holdings. We predict that there is no way the returns can continue. And then we cap it all off by breaking out the word “bubble” to describe the holdings in their portfolio.

Two things are typically true of this process we go through. First, we are typically correct in the long run, as no investor can sustain 30%+ returns forever. But we are also almost always very early in making these calls, and a large portion of the growth manager’s returns come after people like me are saying the returns just can’t possibly continue.

In the same way this process played out with the Janus Twenty fund back in the day, it also played out in recent years with ARK Funds. But if you think I will be taking some sort of victory lap in this article, you would be mistaken.

Even after ARK’s flagship ETF — ARK Innovation ETF (ARKK) — had fallen 65%, its returns still exceeded the returns of many value guys, myself included. So no victory lap is warranted. But I do think there are some lessons all of us can learn from what happened here that we can apply to our own investing.

Here are the five main lessons I have taken from the rise and fall of ARK.

1) Valuation is Not a Short-Term Timing Tool

It was easy to look at the valuations across ARK’s portfolio throughout its rise and to use words like “ridiculous” and “unsustainable”. And by any traditional valuation standards, they were those things. But one of the biggest lessons I have learned in investing is that valuation is useless as a short-term timing tool.

There is no level of overvaluation that tells us anything about the returns of a stock, or a fund, over the next year, or even the next two. But that doesn’t mean we can just throw valuation completely out the window.

2) Valuation Does Matter – Eventually

While valuation might not help us in the short-term, it is much more useful when it comes to predicting long-term expected returns. At one point, the ARK Innovation ETF’s portfolio had a median Price/Sales over 20.

If you look at the long-term returns of a basket of those types of stocks, the word bad doesn’t do justice to how terrible it is. That doesn’t mean there won’t be stocks that will do well within that basket (we will get to that in a minute), but on average, ultra-high valuation stocks are not a good long-term investment

3) A Great Company is Not Necessarily a Great Stock

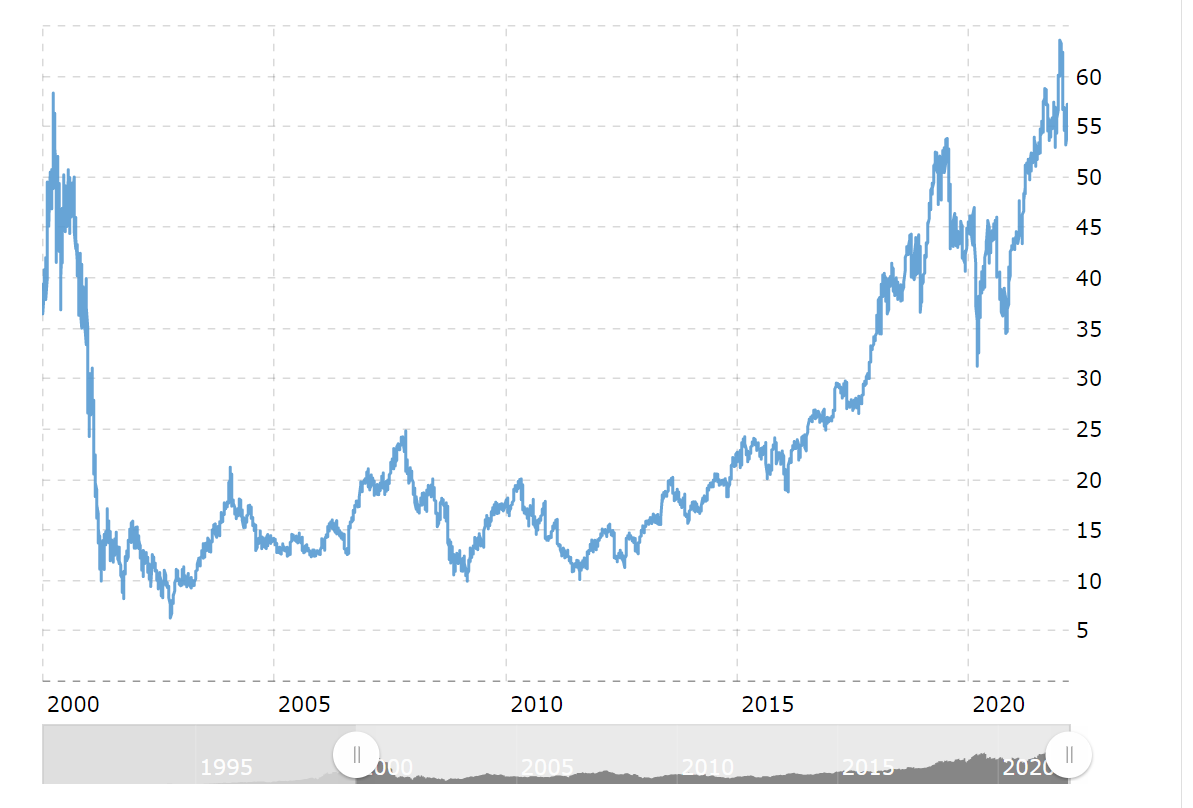

Take a look at this chart.

If I told you this is a chart of a business that has performed very well in the 20+ year period the chart covers, you would likely tell me I am crazy. How could that happen with a stock that was flat for 20 years?

I don’t know if you guessed the company, but this is a chart of Cisco Systems (CSCO). Over the period covered by this chart, Cisco has grown its sales and earnings substantially. So why did the stock go down?

It is all about expectations. We recently had Michael Mauboussin on our podcast to discuss his book “Expectations Investing: Reading Stock Prices for Better Returns” (which he co-wrote with Al Rappaport). The idea they present in the book provides us with the answer as to why we could see a chart like the one above for a company that performed well.

The answer is that the expectations that were embedded in Cisco’s stock price in 2000 were so high that even the very strong performance of its business since then was not enough to meet them. There are many similar examples of this idea throughout history.

There is a very real possibility that some of the companies within ARK’s portfolio will end up being great companies. But there is also a possibility that it won’t matter for investors who bought the fund at the valuations it traded at in the beginning of 2001 because the embedded expectations were just too great.

But that doesn’t mean that the story of Ark has been written yet and the ending will have to be a bad one. And this leads to my next point.

4) Growth Investing is About the Few, Not the Many

I mentioned earlier that growth stocks as a whole don’t perform well. But that is only half the story. The other half is that the best individual performers in the market typically come from the growth group.

Growth investing is a process of finding diamonds in the rough. Amazon (AMZN) and Google (GOOGL), for example, are two stocks that have had massive runs, but have spent the vast majority of those runs living inside the expensive bucket.

With a focused fund like ARK, if one or two of those diamonds are in their portfolio and they can hold on to them, it can easily make up for all the other names that don’t do well. So even though many value guys like me want to write ARK off, the story hasn’t been completely written yet. And this brings me to my final point.

5) A Strategy is Only as Good as an Investors’ Ability to Stick With It

One of the things that has impressed me about ARK’s shareholder base during this 50%+ decline is that for the most part they haven’t sold. The fund has had outflows, but they are nothing like what you would expect for this level of decline.

If the ARK story has a positive ending eventually, whether that ending is also a good one for its shareholders will be a function of their ability to sit through these major drawdowns. And doing that is complicated by the fact that there is a good chance the ending won’t be a good one.

As we sit here today, there is certainly a chance ARK will never recover its current losses and the fund will be a poor investment going forward. Value guys like me will tell you that chance is a pretty good one. But if we are wrong about that, it will be the ability of the ARK shareholder to endure that wild ride that will allow them to tell us I told you so.

The Future of ARK

However this story ends, I can promise you that the ending will look obvious to those on one side or the other in hindsight. If ARK goes on to suffer more major losses, value guys like me will talk about how we saw it coming all along.

If not, the other side will wonder how we couldn’t have seen how obvious the growth potential of ARK’s portfolio companies were. But either way, I think there are timeless lessons all of us can take from this — even if those lessons are coming from a disgruntled value guy.