It’s over. The second quarter is now in the history books. And while the S&P and Nasdaq ended the quarter kissing new highs – up 14.5% and 18.1%, respectively – the Dow Industrials and Transports along with the Russell are not really celebrating, writes Kenny Polcari, chief market strategist at SlateStone Wealth.

At the end of the quarter, the Dow was ahead by 3.8%, the Transports were down 3%, while the Russell was barely positive at +1%.

Meanwhile, on Friday we learned personal income was up 0.5% versus the 0.4% estimate, but personal spending was a bit weaker at +0.2% versus the expected +0.3%. The one that everyone was waiting for was the May PCE report and that came in inline – not hotter, not cooler – which some found to be a disappointment.

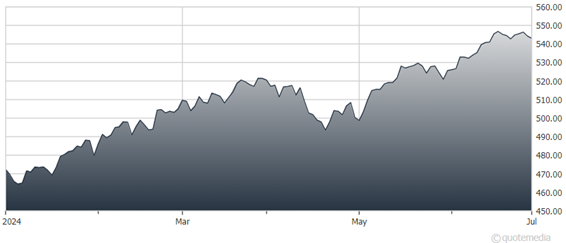

S&P 500 ETF Trust (SPY)

In other markets, oil remains in the $80/$85 trading range. Oil barometers are now reporting that asset managers have boosted their long positions in oil – as they expect the commodity to rise over the coming summer months as demand surges and supplies come into balance.

Remember: The Saudis continue to hold production at lower levels to try and get prices higher. Calls for $90 oil are now common. We are now well above all three trendlines and have the April high of $85 as the next target. Gold was recently trading at $2,345. It remains in the broader range of $2,300/$2,400 that we have been discussing.

Of the 11 S&P sectors, this is how they ended the quarter: Tech up 28%, Communications +26%, Financials +9.2%, Energy +9%, Utilities +7.5%, Consumer Staples +7.5%, Industrials +6.9%, Healthcare +6.9%, Consumer Discretionary + 5.2%, and Materials + 3.1%. Real Estate remains in negative territory at -4.1%.

If we move further down the line, we see that Semis were up 28%, Homebuilders +5.6%, Retail +3.6%, and Airlines +3.3%. The Growth trade is +28%, while the Value trade is up 4.5%.