Selling cash-secured puts is a strategy similar to, but not precisely the same, as covered-call writing, explains Alan Ellman.

It is generally used to generate cash flow as a stand-alone strategy, but also can be implemented to buy a stock at a discount or used in conjunction with covered-call writing (PCP strategy). During the COVID-19 crisis in September 2020, interest rates were near zero as the 10-year Treasury yielded well below 1% and one-year CDs were near 0.1%. This article will highlight a low-risk put-selling strategy that can be used to generate an 18% annualized return.

Selling Cash-Secured Puts to Generate Cash Flow

We select an elite-performing stock and sell out-of-the-money (OTM) puts. Our broker will require a certain amount of cash available to complete the trade should the put buyer exercise the option and the shares are put to us. The amount of cash required is set by this formula:

[(put strike – put premium) x 100 x # contracts]

Put-sellers looking to generate cash flow generally do not want to be share owners but must be willing to accept the shares if the options are exercised and then can either keep the shares, write covered calls, or sell the shares. The options can also be bought back (buy-to-close) to avoid exercise and assignment.

Strategy Proposal: A Real-Life Example with Apple Inc. (AAPL)

Apple Computer has been a top performer in 2020, and we will look to sell weekly deep OTM puts to generate an 18% annualized return. We will circumvent the four weeks of earnings reports. We will look for strikes with Deltas below -0.10 creating scenarios where there is less than a 10% probability of the options expiring in-the-money.

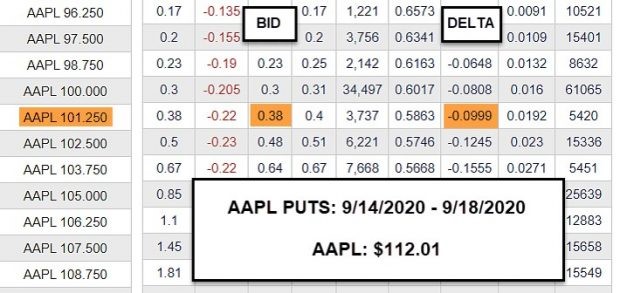

AAPL Put-Option Chain on 9/14/2020

AAPL: Put Option-Chain on 9/14/2020

Note the following:

- With AAPL trading at $112.01, the deep OTM $101.25 put generated a bid price of $0.38

- The delta of the $101.25 strike was -0.0999

- Length of trade is five days

Calculations to Meet Strategy Goals

Let’s assume we sell five contracts. The broker cash requirement formula is:

[($101.25 – $0.38) x 100 x 5] = $50,435.00

The time-value dollar return for the five contracts is:

$0.38 x 100 x 5 = $190.00

The 1-week percentile return is $190.00/$50,435.00 = 0.376%

This annualizes to a 48-week return of 18.08%

Delta Considerations

With the delta less than 10%, exercise is possible but unlikely. We still must have a plan in place if share price declines below the put strike.

Position Management Considerations

If share price moves below $101.25 by expiration, we can take the following actions:

- Buy back the put (could represent a gain or loss)

- Roll the put to the following week

- Allow assignment and retain the stock for the long-term

- Allow assignment and sell the stock

- Allow assignment and write a covered call

Note: AAPL closed at $106.84 on expiration Friday as the puts expired worthless, freeing up the cash to secure additional puts on Monday, September 21.

Discussion

Option-selling strategies can be crafted to meet a myriad of trading goals and personal risk tolerances. By selling weekly deep OTM cash-secured puts on elite-performing securities, we create low-risk opportunities to generate significant annualized returns. This can be particularly useful in low-interest rate environments. The role of delta must be understood and reasonable exit strategy plans must also be in place.

Learn more about Alan Ellman on the Blue Collar Investor Website.