I had several inquiries asking if the BCI 20%/10% guidelines applied to high-volatility securities in terms of the protection we receive from declining share values, explains Alan Ellman of The Blue Collar Investor.

This article will present a case that our 20%/10% guidelines do have broad application as a diverse group of implied volatility securities will be highlighted to show the relationship between IV and Delta.

Definitions

Implied volatility: This is a forecast of the underlying security’s volatility as implied by the option’s pricing in the marketplace. It is generally stated in one-year terms and based on one standard deviation (accurate 68% of the time).

Delta (as defined for purposes of this article): This is the amount an option value will change for every $1.00 change in share value. The greater the chance of the strike expiring in-the-money (with intrinsic value), the higher the Delta.

20%/10% guidelines: Sets up protocol as when to buy back the short calls and is based on the total option premium originally generated. We buy-to-close (BTC) when premium declines to 20% or lower of the original sales price in the first half of a contract and 10% or lower in the latter half of a contract.

Technical Reason the 20%/10% Guidelines Have Broad Application Among a Wide Range of IV Securities

High IV securities tend to have high Deltas resulting in a quicker movement to reach the 20%/10% thresholds. This is precisely what option sellers want when highly risky securities are declining in value as it allows us to take more immediate action.

Securities to be Evaluated

- Amplify Transformational Data Sharing ETF (BLOK) - high implied volatility

- Vanguard High Dividend Yield Index ETF (VYM) - low implied volatility

- SPDR S&P Oil & Gas Explore & Prod. ETF (XOP) - moderate implied volatility

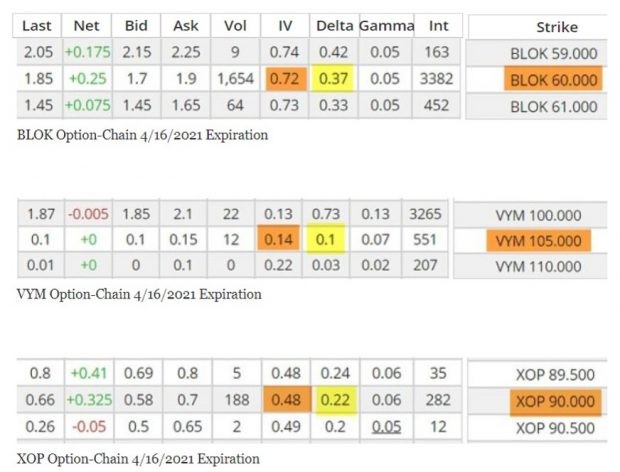

Option Chains for BLOK, VYM, and XOP for Similar Out-of-the-Money (OTM) Strikes

3 Option Chains from www.cboe.com

- Brown cells on the far right indicate the OTM strike price

- The brown cells in the middle of the screenshots indicate the implied volatility ranging from 14% to 72%

- The yellow cells represent the Delta stats ranging from 0.1 to 0.72

Takeaways

Higher implied volatility securities tend to have higher Deltas and vice versa. This will allow us to take more immediate action relating to our position management arsenal when share price of risky securities begin to decline in value.

A Change in Implied Volatility Should Not be Confused with These Conclusions

A rise in the implied volatility of a call will decrease the Delta for an in-the-money option, because it has an increased probability of moving out-of-the-money, while for an out-of-the-money option, a higher implied volatility will increase the Delta, since it will have a greater probability of finishing in-the-money.

Discussion

Our 20%/10% guidelines have broad application among a wide variety of implied-volatility securities. This relates to the fact that Delta plays a mitigating role.

Learn more about Alan Ellman on the Blue Collar Investor Website.