After a decade of massive outperformance, the tide has finally turned against growth investors this year, explains market strategist Jack Forehand, editor of Validea.

The combination of stretched valuations, less favorable fed policy and rapidly rising inflation has produced an environment that is much less friendly for growth stocks, and many of the most expensive names are now 50%-90% off their highs.

While the underperformance of growth may give value guys like me an opportunity to take a victory lap, I am not sure we really deserve one given that most of us were talking about the inevitable collapse of growth many years before it actually occurred.

But rather than dwelling on the past, now that growth multiples have come down, I thought it would be an interesting time to take a look at the arguments for both value and growth going forward given where we are today.

Here are the best arguments I can come up with on both sides of the debate.

The Value Case

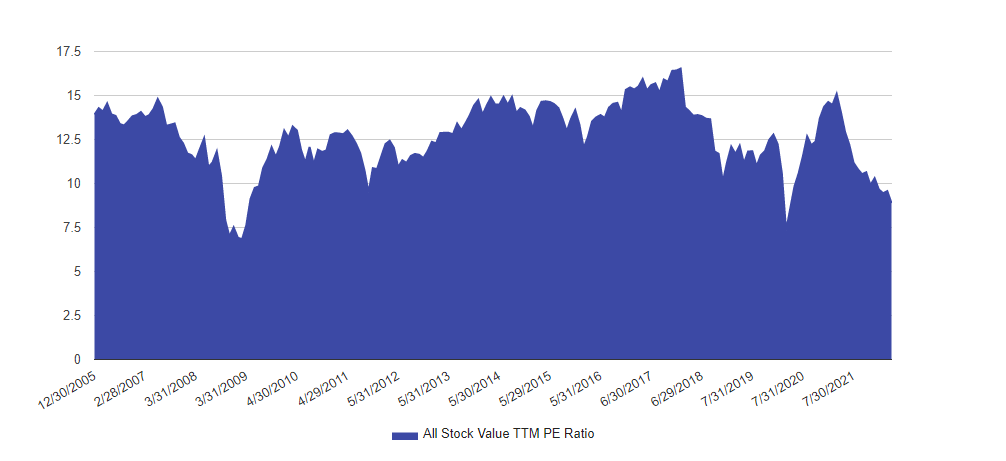

1) Value Remains Cheap

The value case is a pretty easy one for me given that my natural inclination is to believe it. The core part of the argument is that value is cheap both on an absolute and a relative basis.

This chart shows the median valuation of the cheapest 20% of our database using the PE Ratio. On an absolute basis, value is in the 5th percentile using data from the period from 2006 to today. It was only cheaper at the bottom of the 2008 and 2020 bear markets.

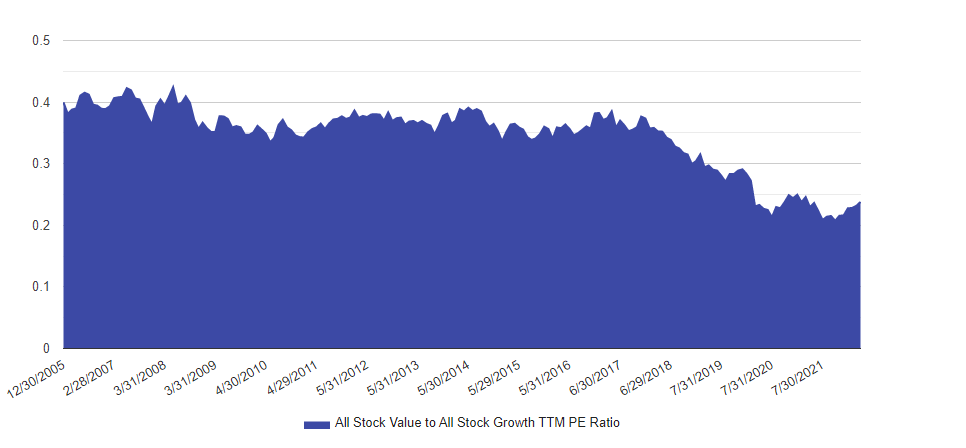

On a relative basis, value is cheap too. Relative to growth, it is currently in the 10th percentile. It was is the 1st percentile not that long ago, but the big drawdown in growth has reduced that to some degree.

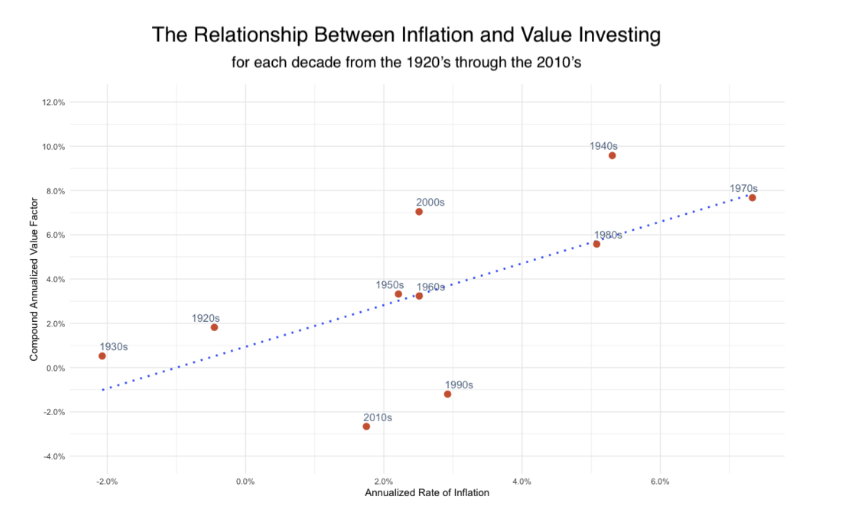

2) Value Should Be More Equipped to Weather Inflation and High Rates

In theory, value stocks should perform better when inflation is higher and rates are higher. Since value stocks have more of their future cash flows in the near term, higher discount rates have less of an impact on their present value. Growth stocks, on the other hand, are more valued using cash flows that are both more uncertain and further out in the future. Higher rates and higher inflation aren’t good for that.

But when you break rates and inflation out separately, you get different conclusions on their impact on the performance of value vs. growth. The data to support better value performance during high inflation environments is fairly strong. This chart from Euclidean Technologies looks at the relationship over time.

The data to support value outperformance during high rate environments — as opposed to high inflation — is less strong, though. But despite the fact that the data on the relationship between the performance of value and inflation and interest rates isn’t as compelling as some think, there still is reason to believe value should have an edge over growth in a period like the one we are in.

Narratives have become so important in markets that it might not matter all that much what the data shows. If the story of value winning because of high inflation and rates takes hold, it can become a self-fulfilling prophecy.

The Case for Growth

Now that we have the case for value out of the way, it is time for the value guy to try to make the case for growth. What you will not see me do, though, is to try to make a case for a return to the period a couple of years ago with many firms trading at 20 and 30 times sales.

Those valuations were never sustainable and we are very unlikely to see them again for a long time. But that doesn’t mean that a case can’t be made for growth to outperform. Here is my best shot at making that case.

1) The 2000 Comparison is Too Easy

Every value guy, myself included, wants to compare the current period to 2000. If that comparison is valid, the underperformance of growth could go on for years. But I think there are some key differences today. The most important one is that the leading growth companies of today are just better companies than the growth names of that era.

That doesn’t mean they deserve to trade at limitless valuations. But it does mean that their businesses are likely to continue to grow, and when you combine that with price declines, multiples are falling and we might not see the same growth carnage now we saw then.

2) Inflation Might Not Be the Problem Many Think It Is

I think we are clearly at the point where we can say that inflation is not transitory, at least not in the way the Fed meant it when it used the term. But it is important to keep in mind that what matters is not what inflation is today.

What matters is what the market expects it to be in the future, and what the reality ends up being relative to that. And there is an argument to be made that we might be near peak inflation. If future numbers come in below expectations, that could benefit growth.

Also, it is important to keep in mind that inflation is a revenue story for companies as well as a cost one. For growth firms with high operating leverage, the revenue impact can end up being bigger than the cost one, which leads to higher profits.

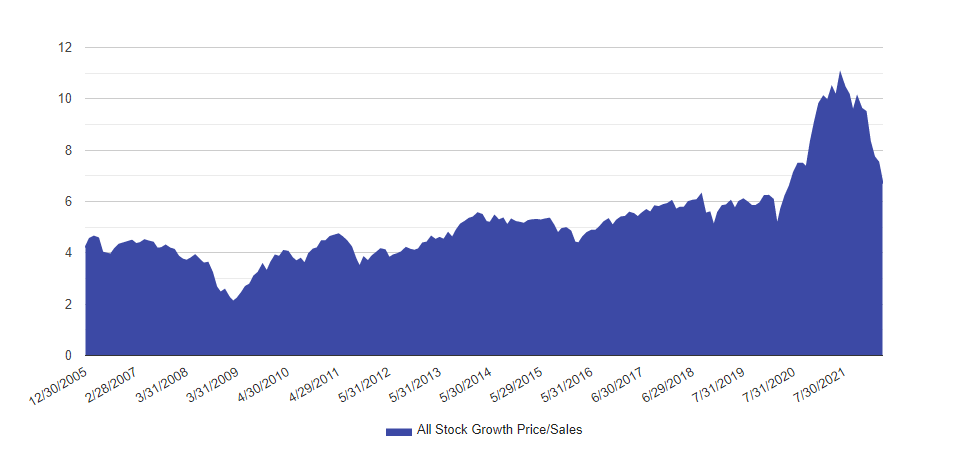

3) Multiples Have Come Down

It pains me to even write this as a value guy because it is hard for me to even speak about multiples this high, but the Price/Sales required to enter the top decile of our universe has fallen from 11 at the high to around 6.6 today.

That is down from the 100th percentile to the 80th. It is very difficult to call even these reduced valuations cheap, but they are down 40% from the peak. As I noted above, if growth companies continue to sustain their growth, multiples could continue to compress even without further big price declines.

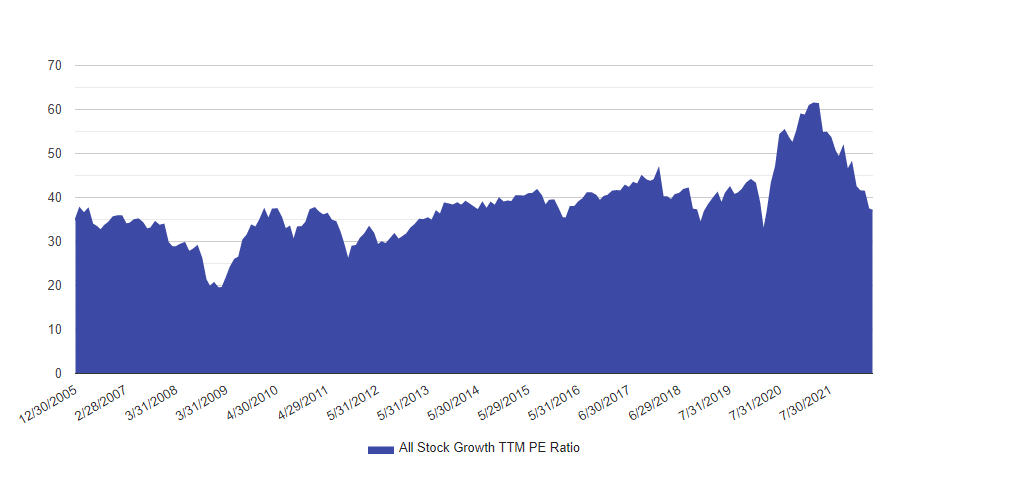

And if you look at the same thing using the TTM PE ratio, the median growth stock’s valuation is pretty middle of the road and is down from its ridiculous levels from last year.

The Benefits of Looking at Both Sides

My natural inclination is always going to be to believe in the case for value. But that inclination has sometimes steered me in the wrong direction. My support of value in 2014 is a great example of that.

Although I personally think the case for value is the stronger one right now, I also want to continue to look at the other side to keep myself honest and to think about what the world might look like going forward if I am wrong. And the recent decline in growth has at least got us to the point where we can have this debate. I guess that in and of itself is progress.