It’s great to be back after a few much-needed days off and a grand 1,500-mile adventure across the American West. The S&P 500 Index (^SPX) has risen 3% three weeks in a row only three times since 1950 if memory serves. In each case, it was overwhelmingly positive a year later by an average of 33%, says Keith Fitz-Gerald, editor of 5 With Fitz.

I had hoped that Iran would be behind us by now but that looks not to be the case as I type. Try hard not to get consumed by the headlines though. This could be one of the most important earnings seasons in a while. It doesn’t matter if you’re a trader or an investor. And earnings are pretty dang good so far.

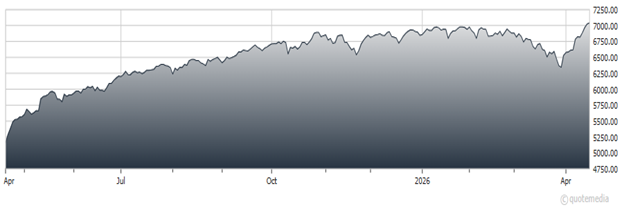

S&P 500 Index (^SPX)

Just 10% of S&P 500 companies have reported so far. But the early “print” – meaning what the numbers say – is outstanding. Some 88% of the companies that have reported have beaten on earnings and 84% have beaten on revenue.

The big banks have already come and gone — JPMorgan Chase & Co. (JPM), Goldman Sachs Group Inc. (GS), Bank of America Corp. (BAC), etc. — and the message was consistent across the board. Client activity picked up, capital markets came back to life, and credit quality held up far better than the recession mongers and doom artists predicted.

What I like most though was this: The blended earnings growth rate sits at 13.2% for Q1. If it holds, that would mark the sixth consecutive quarter of double-digit growth. As I noted to the super-savvy Stuart Varney recently, I think it could finish earnings season at 15%-20%.

Take a moment and let that sink in. The legion of doom has been very vocal the entire time and VERY wrong the entire time…about the sky falling, about the economy, about the AI bubble babble, and more. Meanwhile and as always, we’ve stayed true, which raises an important point yet again.

The sooner you learn to focus on great companies putting up great numbers, the sooner your portfolio will thank you.