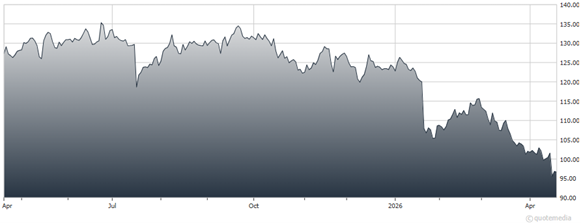

Shares of Abbott Laboratories (ABT) are now down more than 22% in 2026. The medical device maker and healthcare products and services provider got no help from its Q1 earnings release. But we continue to think very highly of Abbott and its strong financial position, writes John Buckingham, editor of The Prudent Speculator.

First-quarter sales climbed 7.8% year-over-year to $11.1 billion, topping consensus estimates of $11 billion, while adjusted EPS of $1.15 edged past the average forecast. Medical Devices again did the heavy lifting, with solid growth in cardiovascular and diabetes care. Established Pharmaceuticals delivered another solid quarter, while Diagnostics was mixed (core lab strength was offset by softer respiratory testing). Nutrition continued to work through pricing missteps and volume adjustments.

Abbott Laboratories (ABT)

Shares have struggled over the past year as investors digest the comedown from pandemic-era testing profits, a difficult Nutrition reset (including WIC-related disruption and pricing actions), and the near-term dilution and integration questions tied to the Exact Sciences acquisition. All are headlines that have outweighed steady device-led fundamentals (like the Freestyle Libre continuous glucose monitor).

Investor concerns were not helped by Abbott’s near-term outlook. For Q2, ABT guided adjusted EPS to $1.25–$1.31, slightly below what the Street had been calling for.

Yet we remain mindful that short-term fluctuations are a normal part of the business landscape, particularly for a diversified healthcare company navigating shifting demand patterns. We believe Abbott’s diversified revenue stream and growth potential from medical devices (particularly from its growing Diabetes Care and Medical Device businesses) in the years ahead offer resiliency to our portfolios.

This is supported by Abbott’s R&D pipeline which appears primed for new product launches that position the company well going forward. Shares trade at 17 times NTM adjusted EPS expectations, below historic norms, and carry a dividend yield of 2.6%.

Recommended Action: Buy ABT.