The surprising result of the U.S. presidential election confounded many investors who had positioned themselves for a different outcome, explains Monty Guild of Guild Investment Management in their latest special premium commentary.

The incoming administration had won on an “America first” platform and had emphasized its intention to renegotiate trade agreements with many of the U.S.’ trading partners, particularly China and Mexico.

The instinctive, fearful reaction of many market participants was to imagine the arrival of a global trade war in which the new administration’s anti-globalist campaign rhetoric would rapidly translate into a curtailing of global commerce.

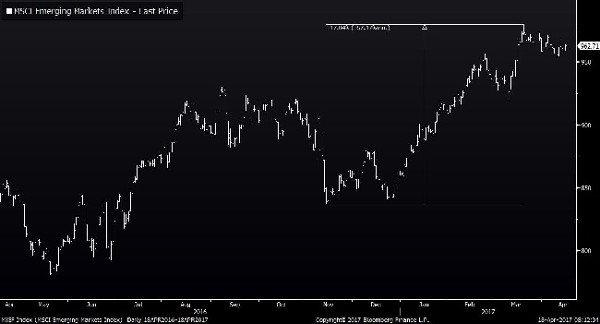

The stocks of many emerging-market economies had begun to rally earlier in 2016 with the reacceleration of global growth that followed the passing of the dollar and oil shocks that we have written about often in recent months.

In November, they declined sharply as nervous investors discounted the policies of a new administration that they assumed would be hostile to free trade.

But lo and behold: after two months of volatility, emerging markets continued their rally even more strongly. They are now correcting part of that move.

This performance is not out of touch with the performance of the U.S. stock market in the period following the post-election lows. However, another perspective appears when we examine the performance of emerging markets since the financial crisis, and compare it to the U.S.

In a seven-year snapshot, the U.S. is up substantially, and emerging markets are down 5%. Increased demand for raw materials was met with increased supply, so emerging markets did not fully benefit.

In the manufacturing sector, profits grew; but not at the rate that was projected. Part of this was due to increased conservativism on the part of consumers in the developed world, who are more price-conscious and somewhat more averse to conspicuous consumption than in years past.

This observation brings us to our main point. Over the past year, we have seen market sentiment fluctuate sharply according to prevailing perceptions of risky events, and prevailing sentiment about nebulous future risks to the global post-crisis economic recovery.

We could mention the panic that surrounded the Brexit vote; or the consternation and uncertainty that accompanied the election upset in the U.S.; or fears of secular stagnation among some members of the U.S. Federal Reserve Board of Governors.

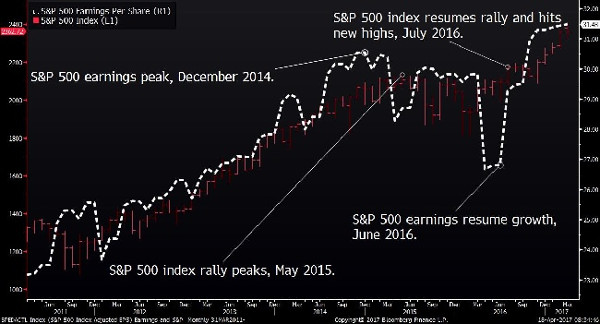

All of these events caused or accompanied significant market volatility. Yet underneath the news flow was a swell of positive financial and economic progress which ultimately lifted corporate profits and stock prices… and showed that prophecies of doom were premature.

“You can’t stump the Trump” was a rallying cry for the new president’s supporters at his more raucous campaign events last summer… but perhaps what you really couldn’t stump was the next up-leg in the global recovery from the Great Financial Crisis. And eventually, that translated into corporate profits and higher stock prices in the developed world.

What This Means For Emerging Markets:

After Underperforming for Years, Are They Ready To Catch Up?

Last year, negative news-flow and worrisome geopolitical events caused market volatility, even while the real underlying economic and financial fundamentals strengthened.

Emerging markets still face plenty of potentially destabilizing events. The new U.S. administration has begun to project a more engaged military stance, first in Syria, now in the Korean peninsula; isolationist rhetoric is giving way to a more recognizably mainstream Republican view.

While that may be reassuring to some on the basis of its greater predictability, it presents the prospect of market volatility arising from military action.

Also, since both commodity-exporting and manufacturing-centered emerging market economies depend on the vitality of growth and trade in the developed world, developed-market volatility has the prospect of spreading to emerging markets as well.

We believe, however, that the fundamental story for emerging markets is deeper than these surface disruptions will prove to be. A relatively minor part of that story is the new up-leg in the post-crisis global economic recovery, particularly in Europe. The main part of that story, though, is the relative underperformance of emerging markets for the past decade.

Earnings, and earnings expectations, have risen in developed markets, as they have been relatively stronger performers. The gap in 12-month forward price-to-earnings ratios between the S&P 500 Index and the MSCI Emerging Markets Index has grown wider than usual.

On average, since 2006, the S&P 500 has enjoyed a 22% premium to emerging markets in its 12-month forward price-to-earnings ratio. Currently, that premium is at 32% -- nearly a full standard deviation higher.

With basic positive global growth and trade data supportive, a few of the best emerging markets have the potential to narrow that valuation gap.

We note that we are not equally enthusiastic about all emerging markets; we continue to favor manufacturers over commodity exporters, and particularly manufacturers leveraged to technology, such as South Korea.

We also favor India, where electoral results are supporting the rational and growth-oriented policies of Prime Minister Modi. We note further that the positive global growth backdrop should still be watched closely, and that if the real fundamentals falter, EMs will face tough sledding.

Over the longer term, we expect the undervaluation to correct itself, and continue to support a catch-up in the best-growing emerging market stocks.

Investment implications: At the current juncture, we are particularly interested in India and South Korea. ETFs exist for both countries.