Toys “R” Us managers told 33,000 U.S. employees March 14 that all stores will close soon. It is a lesson for investors … and a confirmation of what I’ve been telling you: Steer clear of lousy managers, writes Jon Markman, editor of The Power Elite and Tech Trend Trader.

Another iconic American store is on deathwatch.

That’s according to a Wall Street Journal report that “We’re putting a for-sale sign on everything,” according to CEO Dave Brandon.

It would be easy to blame Amazon.com (AMZN). The online pioneer has become a scapegoat for every shuttered storefront, every desolate suburban mall.

Critics have embraced this zero-sumism with ease. If Amazon.com is winning, then everyone else must be losing.

It’s not like that. Not really.

Like Walmart (WMT) before it, Amazon emphasizes the things it does well. That means vast selection, low prices, fast delivery and, most important, best-in-class customer service.

Toys “R” Us has a few things working in its favor. It is a 70-year-old empire. In the U.S. alone, it operates 735 stores. It has scale, an established supply chain and a big brand name in a niche market. Managers should be able to compete.

But this store hasn’t towered above the competition for some time…

Today, Toys “R” Us is unrecognizable from the chain Charles Lazarus founded in 1957. He was able to grow the business by leveraging its scale. In exchange, customers got vast selection, low prices and a fantastical (at least for kids) shopping experience.

By 2005, its high margins and cash flow were the envy of the retail industry. Private equity investors sat up and took note. After a bidding war, a consortium led by KKR & Co., Bain Capital and Vornado Realty Trust (VNO) took the company private in a $6.6 billion leveraged buyout.

That’s when the wheels began to fall off…

Its cash flow, once used for expansion, went to service $5 billion of debt. Margins shrunk, which led to operational problems. To rein in expenses, the number of stores was slashed … and then slashed again.

Toys “R” Us became a much-smaller business. It no longer had scale.

Last September, the company filed Chapter 11 bankruptcy. Initially, the plan was to close 180 stores and restructure operations yet again. Now, seven months later, it appears that the entire business is going to be closed.

The fall of Toys “R” Us is a sad story of bad management. Greedy private-equity firms took a great retail business, leveraged it to the hilt and then consistently underperformed by not paying attention to customers.

As an investor, you need to avoid these businesses. (I can help. Here’s how…)

It is not easy. There are plenty of them. They are masquerading as blue-chip conglomerates and storied innovators. They are airlines, car companies and many other businesses Wall Street says you should own.

Ignore all of that.

Finding great businesses to invest in is hard work. I have been doing this for decades, and I know there is no substitute for focused managers who relentlessly look forward and create lasting shareholder value. This means tirelessly building competitive advantages, leveraging strengths and forging relationships with customers.

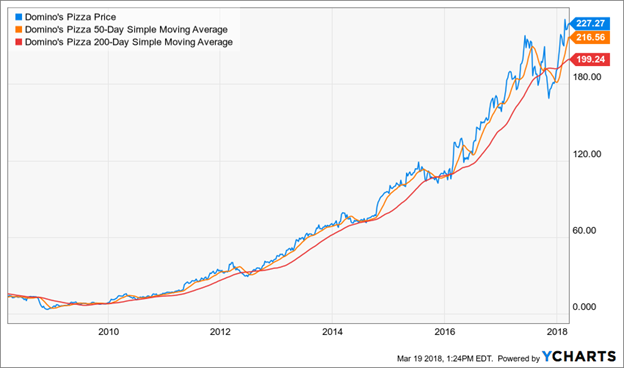

In 2008, shares of Domino’s Pizza (DPZ) went for four bucks — less than a pizza. The business was not unique. It held few competitive advantages, and its pizza was not especially well-liked. Customers routinely complained the crust tasted like cardboard.

Over the course of the next two years, the company brought in new managers, reengineered its recipes and started to rebrand its business around great products, low prices and fast delivery.

With a better product in hand, managers then began to lever its scale. They refined the supply chain to increase profitability. They used software to improve delivery times at its 9,000 stores.

The Michigan pizza giant also committed to digital. Since the early years of the iPhone, Domino’s managers have focused on reducing friction in the ordering experience.

Its smartphone app is the highest-rated food application in the Apple ecosystem. Orders placed via smartphone or computer accounted for 60% of all sales in 2017. And Domino’s development teams committed to Amazon Alexa and Google Home to ensure it is a big player in voice.

In 2017 the company began delivering pizzas in the Netherlands and Germany using a diminutive self-driving robot developed by Starship Technologies. It has a similar trial program with Ford (F) in Florida.

Meanwhile, growth has gone ballistic. The company now has 14,800 stores in 85 markets worldwide. In 2017, sales were $2.8 billion, up 12.8% over 2016.

The share price, at $229, is up some 1,600% since 2008.

Domino’s managers didn’t only reinvent their pizza recipes. They reimagined the experience. They developed a plan to create shareholder value and used their unique strengths to implement it.

Keep an eye out for companies like Domino’s that dominate important niches, and are growing fast but are underappreciated.

Strangely enough, this description still applies to Domino’s, which has a market cap of just $9.9 billion, a tenth the size of industry powerhouse McDonald’s (MCD).

Best wishes,

Jon D. Markman

P.S. Domino’s is one of a small group of stocks I call The Power Elite. There are only about 30 names on this list. And they average $10 million each in new wealth creation, every day. That’s $300 million in total daily profits! See how you can get your piece of the pie here.

Subscribe to Jon Markman’s Power Elite newsletter here

Subscribe to Jon Markman’s Tech Trend Trader here

Subscribe to Jon Markman’s Strategic Advantage here