When we write covered call options and sell cash-secured puts, our goal is to generate cash flow in a low-risk manner, states Alan Ellman of The Blue Collar Investor.

Frequently, a second important goal is to avoid the exercise of the options, which means avoiding the strikes from expiring in-the-money (ITM) or with intrinsic value. In the case of covered call writing, this will avoid selling our shares and in the cash of cash-secured puts, it means avoiding having the shares put to us. This article will utilize at-the-money (ATM) implied volatility (IV) and the BCI Expected Price Movement Calculator to result in ultra-low-risk trades that generate lower but still significant premium returns, with an approximate probability of 84% of avoiding exercise (expiring ITM).

What is the BCI Expected Price Movement Calculator?

A spreadsheet that generates an approximate trading range for a specific contract cycle, using implied volatility statistics and a conversion formula inherent in the spreadsheet. The formula will recalibrate the published IV annualized stats into one specific for the contract cycle being traded.

Why 84% approximate probability of success?

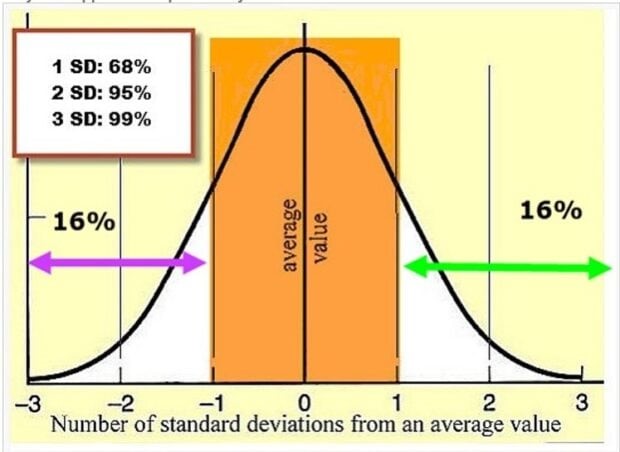

- IV is based on one standard deviation (approximate 68% probability of falling into the range)

- Of the 32% that falls outside the one standard deviation range, 16% is to the downside and 16% to the upside

- This results in an approximate 84% probability that the stock price will not move above or below the one-standard deviation range

- For example, if we do not want to exercise of a call option, our risk is 16% to the right of the graphic (green arrow)

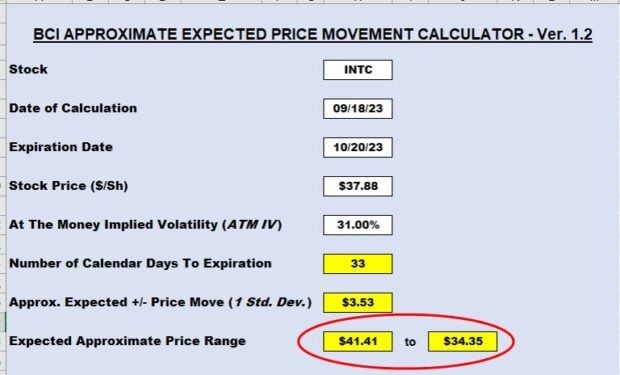

Real-Life Example with Intel Corp. (INTC)

- The ATM $38.00 strike (INTC trading at $37.88) has an IV of 31%

- This is an annualized IV based on one standard deviation

Expected Price Movement Calculator

- If we were seeking an OTM call option, with an approximate 84% probability of avoiding exercise, we would choose a $41.00 or $42.00 strike

- If we were seeking an OTM put option, with an approximate 84% probability of avoiding exercise, we would choose a $34.00 or $35.00 strike

Discussion

Upper and lower limits of a trading range for our underlying securities can be achieved with an approximate 84% probability of success, using IV and the BCI Expected Trading Range Calculator. This strategy approach is particularly useful when seeking to generate ultra-low risk with lower, but still significant, option returns.

Learn more about Alan Ellman on the Blue Collar Investor Website.