Earnings season is a busy time at Guild Investment Management, since our management style emphasizes the careful selection of individual stocks rather than broad indices, notes Monty Guild, in Global Market Commentary.

That means that we typically have two or three dozen company conference calls to listen to; we find that significant details are often neglected in the summary reports of these calls provided by broker analysts, so we like to listen so that we can judge for ourselves.

As we often say, “Earnings are the mother’s milk of stock prices,” so let’s see how earnings are shaping up in the U.S.

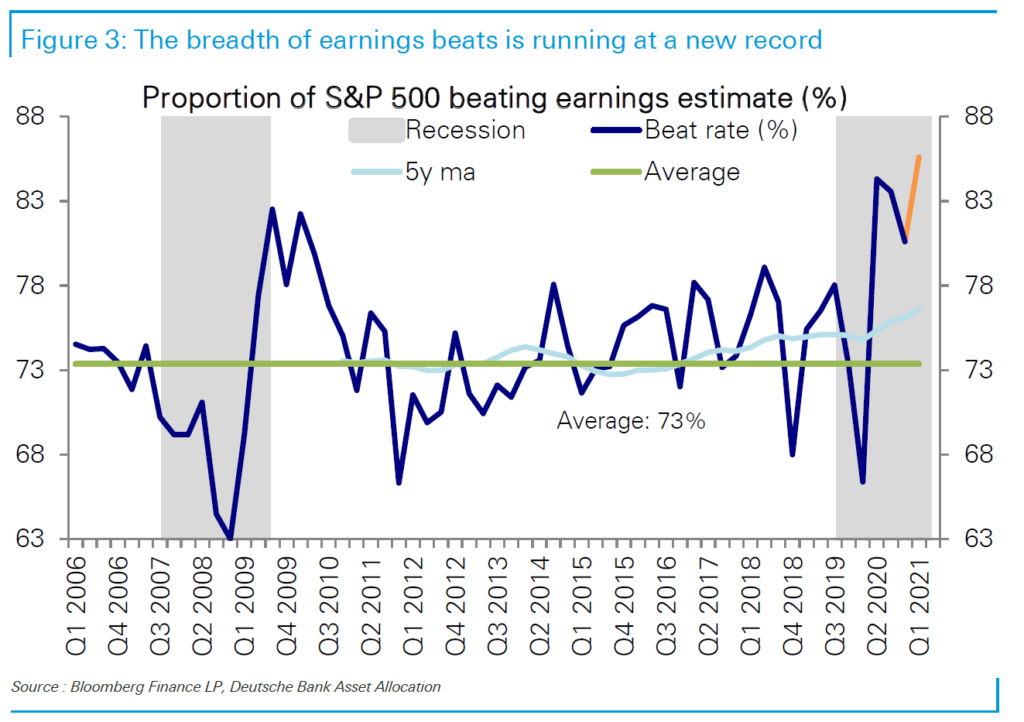

Looking at the U.S. stock market as a whole, the quarter is shaping up to be the fourth consecutive one with strong earnings beats.

As of the end of last week, 86% of companies were delivering earnings beats, exceeding estimates by an average of 19.8% and by a median of 12.3%. (Historically, 73% of companies beat estimates, by an average of just 4.3% and a median of 3.4%.) 78% of companies have beat on sales, compared to a historical average of 57%.

Source: Deutsche Bank Research

In short, earnings are very strong. Year-on-year, as we lap the beginning of the pandemic, earnings are coming in at an impressive 46% gain. (Japan thus far has shown a 46.8% increase, and EAFE as a whole 68.4%, showing in part the depth of Europe’s decline last year.)

Interestingly, companies that beat have sold off by an average of 0.5%; companies that missed have sold off as well, but more severely. Is this cause for alarm? Not necessarily.

Particularly for cyclicals, the rule is often, “Sell on good news, and buy the dip.” The fact that we are seeing this trend play out suggests that cyclicals have more gains in front of them in the mid-term, even as a near-term correction remains a possibility.

As we listen to calls, and as we get on-the-ground intelligence from our network of friends and contacts in various sectors and industries, we hear a common story.

As the pandemic gradually resolves, and as the policy responses that subdued economic activity gradually fade, sales are exceeding expectations. Some of those sales are inventory restocking, which in itself is a positive sign, as dealers wouldn’t be restocking if they didn’t expect demand to continue.

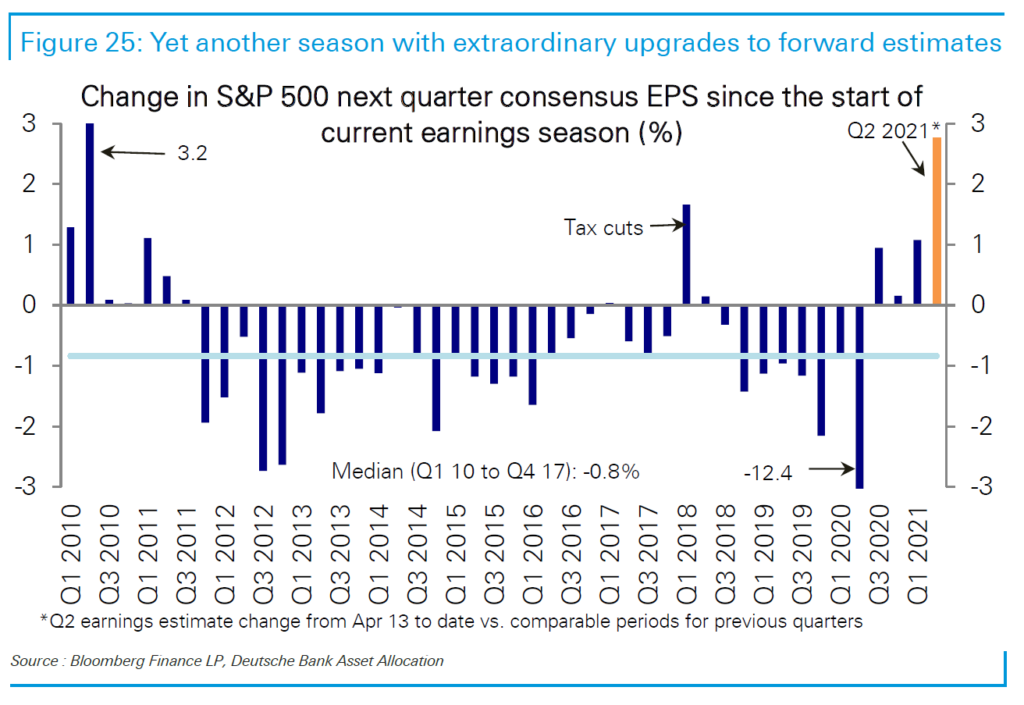

Companies providing construction equipment, commercial and residential building equipment, and industrial automation equipment are all bullish about the prospects for growth. That’s why many of them are raising estimates for the full year, and analysts are following suit.

Source: Deutsche Bank Research

The fly in the ointment, as we suggest above, is that this might be “as good as it gets” — in other words, as we noted last week, many year-over-year data points are reaching peaks as we lap the most intense phase of pandemic restrictions last year.

We think that’s more likely to lead to a correction — probably a modest one, or a sideways consolidation — than to a larger decline. In spite of a manufacturing economy that’s growing faster than it has since the 1980s, total industrial production is still significantly below pre-pandemic levels.

Source: Federal Reserve Bank of St Louis

Investment Implications: In our view, cyclicals remain good bets as we continue to move forward into the post-pandemic economic recovery. We think that investors could intelligently make use of weakness occasioned by earnings reporting, or a broader market decline, to add exposure to cyclicals and the recovery theme.