Rising inflation, growing demand for fossil fuels and a looming supply shortfall will power what’s likely to be a multi-year supercycle in commodities and related stocks alike, forecasts Elliott Gue, editor of Energy & Income Advisor.

We believe WTI remains well-supported should it dip to the $65 to $70/bbl range and should average in the low-$70s to low $80s/bbl. In addition, the chance of sharp upside spikes in oil, even as high as the $100/bbl range, remains much higher than the odds of a collapse back to below $65/bbl.

Crude oil prices experienced a long bear market from late 2014 through much of 2020 that was primarily driven by excess supply and OPEC’s decision, albeit in fits and starts, to combat rapid, unrestrained growth in US shale oil output.

Arguably one of the more dangerous fallouts from the OPEC-shale “war” of 2014-2020 is that the generally low oil prices of this era fed predictions that the long era of petroleum (and fossil fuels more generally) was finally over.

After all, it’s much easier to forecast “Peak Demand” for oil when prices are in the $40s/bbl or lower or to claim, as some have, that new oil discoveries represent a stranded asset because falling demand will render these hydrocarbons worthless.

Similarly, it’s much easier for governments to adopt aggressive targets for green energy or carbon emission reductions when retail energy and fuel prices are relatively low.

The real test, as we’re seeing right now, is how these targets and mandates fare as consumers begin to revolt against rising prices, fuel shortages and as the danger of triple-digit oil prices grows. The fact is that, as we’ve explained, we’re already seeing signs of push-back in Europe and it’s only a matter of time before that becomes a larger story, particularly if the European winter is harsh.

Our view remains that the lack of investment in new oil and gas projects outside shale following the 2013/14 price crash will come back to haunt global markets, leading to a shortfall in oil and gas supplies over the next few years relative to growing demand. That’s long before electric vehicles will have enough of an impact on global demand to provide significant relief.

As we’ve written extensively in recent issues, US shale producers including EOG Resources (EOG), Pioneer Natural Resources (PXD) and Occidental Petroleum (OXY) remain top plays on the current more constructive environment for crude oil.

PXD’s “breakeven” oil price is around $30/bbl WTI and we believe the company will emerge as one of the industry’s premier income stocks in 2022 thanks to its formulaic approach to returning capital to shareholders via special quarterly dividends. At current oil and gas prices, PXD could yield well north of 10% in 2022. We’re raising out buy under target from $155 to $175 to reflect the increasingly bullish outlook.

Occidental will likely prioritize paying down debt over dividends and capital return near-term as it seeks to reduce debt accumulated via the ill-timed acquisition of Anadarko back in 2019.

However, as leverage drops down closer to the industry average in 2022, we see OXY closing some of the valuation gap with its peers.We see OXY reaching $40 in the first half of 2022 and we’re raising ourt buy target accordingly from $28 to $32.

And don’t forget the supermajors.The naysayers derided Exxon Mobil (XOM) for spending big on exploration and development of new projects while most companies in the industry were cutting back and focusing on returning cash to shareholders. But that move looks increasingly prescient as XOM will be bringing world-class, low-cost oilfields onstream over the next few years when that supply will be sorely needed. We rate XOM a buy under $68.

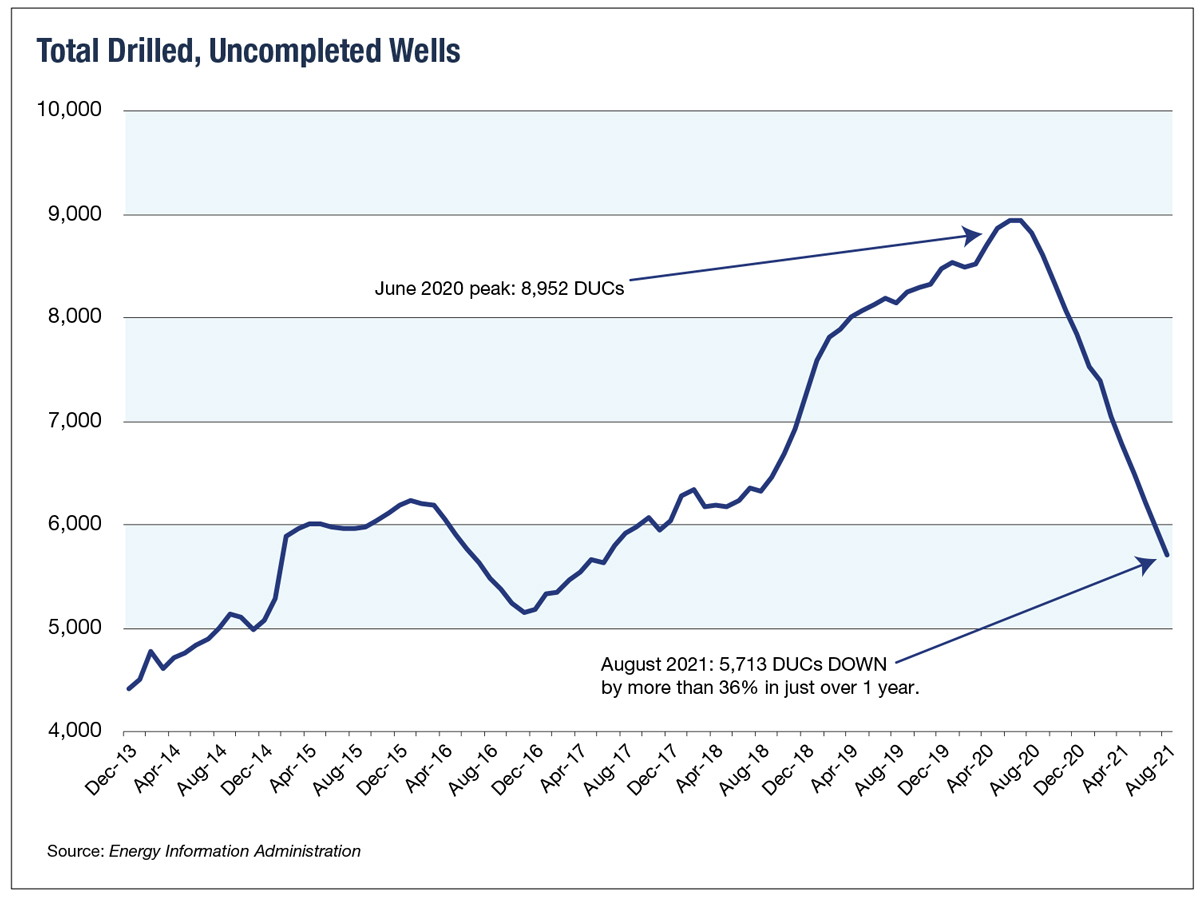

We’ll also be watching the oil services space carefully over the next 3 to 6 months as 2022 could be multiple upside catalysts for the group. The chart below shows the total number of DUCs in shale regions covered by the monthly Drilling Productivity Report.

These are wells that have been drilled but not yet fractured and put into production; as you can see, producers have quickly burned through muc of their DUC inventory and we’re approaching levels unseen since late 2016.As shale producers run out of DUCs to complete, they’ll need to start drilling new wells more aggressively just to maintain current output or grow oil output slowly over time, in line with current plans.

We’re looking for signs that this phenomenon might boost demand for services and equipment used to drill US shale wells. We already believe the recovery in the services market outside the US is well underway.

And, as more producers recognize the looming supply challenges caused by underinvestment in new supply since the 2013/14 oil price crash, we believe the need for significant catch-up spending will play right into the hands of Schlumberger (SLB) with its focus on international services work.