Iron Mountain Incorporated (IRM) is a unique REIT; indeed, we previously selected this as our "Best REIT pick of the Year", recalls income expert Rida Morwa, editor of High Dividend Opportunities.

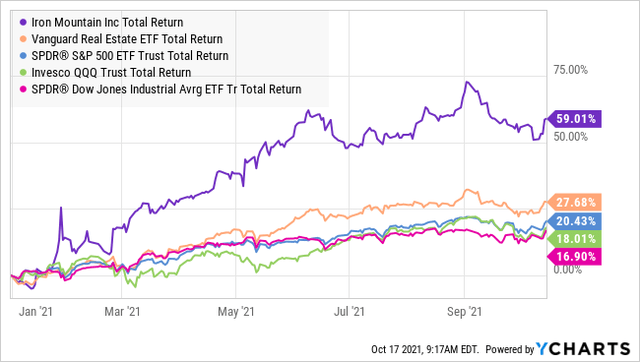

Here we are entering the fourth quarter, and IRM has returned more than 50% year-to-date, materially outperforming all of the indexes and most real estate investment trusts.

IRM is in the business of storing and managing data. For the past several decades, that has meant literally storing paper. All those corporations with piles of paperork and nowhere to keep it turned to IRM. IRM counts over 95% of Fortune 1000 companies among their customers.

It is no secret that computers are revolutionizing how we store and manage data. Over the past several years, IRM has invested heavily in its digital services. With the unique ability to bridge the physical and digital world, IRM has found a niche among companies that need to store data in both physical and digital ways.

We saw great potential for 2021 because of the strong tailwinds generated by improvements IRM made to their business in 2020. IRM did not sit idly by in 2020, it went to work finding ways to make its business more efficient and more profitable. The tailwinds we predicted were:

- IRM's core business of paper storage would continue to grow at a 2-3% rate.

- IRM would see substantial recovery in its "services" segments which provide shredding, data retrieval, and other physical services. This segment was impacted the hardest by COVID shutdowns.

- Momentum in IRM's digital services would continue to increase.

- "Project Summit" — IRM's cost savings/streamlining initiative — would materially improve margins.

We projected that these tailwinds would cause IRM to see growing cash flow for the first time in several years. These tailwinds came in during the first half and are still going strong. Rental growth on IRM's legacy business is maintaining its strong pace of growth.

IRM's data center business is the fastest-growing segment, up 13.3% year over year. That growth is likely to pick up speed as the projects that are currently under construction will increase IRM's capacity by 45%.

As a result of these tailwinds, IRM increased guidance in Q2. With Q3 earnings coming up, and IRM pulling back from all-time highs, now is a great time to add to this position before it takes another leg up. IRM is firing on all cylinders, improving earnings across all of its segments and that is providing growth for AFFO/share, and will start driving the dividend up as well.