Closed-end funds — which we call our Shadow Funds — have been working for us since the beginning of the year; the BlackRock Health Sciences Trust (BME) is the newest addition to our Shadow Fund recommendation list, notes Steve Mauzy, editor of Wyatt Research's Dividend Confidential.

The fund owns a diversified stock portfolio composed of the largest healthcare companies in the world. You’ll readily recognize the names: UnitedHealth Group (UNH), Abbott Laboratories (ABT), Pfizer (PFE), Johnson & Johnson (JNJ), Eli Lilly (LLY), and other names I’m sure you know. The fund holds 140 different healthcare-centric companies in total.

Unlike the individual securities that populate the portfolio, the BlackRock fund is managed to generate a higher income yield than the individual securities. The fund pays a distribution that generates a 5.8% starting yield as I write.

Through judicious use of low-cost leverage, BlackRock amps up the distribution. The distribution to you is nearly double the average of the stocks in the portfolio. What’s more, that distribution is paid in monthly installments, as opposed to the quarterly installments the securities themselves pay.

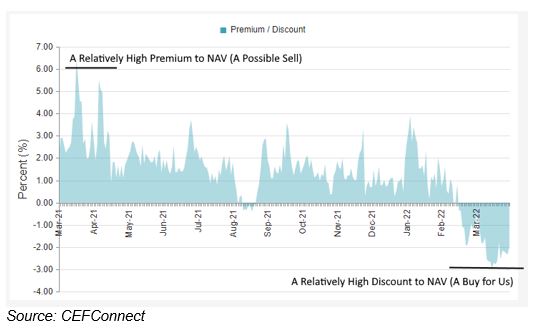

We pay attention to relative discounts and relative premiums, particularly relative discounts. If the relative discount is greater than the historical average discount, a buy opportunity could be emerging. If the relative discount exceeds the historical average by a wide margin, a buy opportunity has likely emerged.

The BlackRock fund’s shares trade at a 2.0% discount to the investments that populate its portfolio. The discount might appear trivial in isolation, but when compared to the historical average discount, it’s a big deal. The BlackRock fund’s shares typically trade at a premium to net asset value (NAV). The premium has been as high as 6% over the past year.

BlackRock Health’s Premium/Discount (Mostly Premium)

Sticking with the topic of relative value, BlackRock’s z-score further buttresses my buy recommendation. The z-score is a statistical measure of value. It tells you the value today compared to historical value.

The higher the z-score, the less appealing the value proposition. Here, we seek the negative. Our interest is piqued when we cross paths with a closed-end fund that sports a z-score of -2 or greater. BlackRock’s z-score is -2.2. The BlackRock fund is a relative value today.

Seasoning is another reason I like the BlackRock fund. The fund has been around since 2005. It’s been battle-tested. It has survived the battles. Indeed, it has more than survived, it has thrived. The share price has nearly doubled since its April 2005 public debut. This is a big deal among closed-end funds.

When you vet the closed-end fund universe, you’ll find that most funds fail to maintain their IPO price. Even years later, you’ll find closed-end funds that trade 50% or more below the IPO price. (Mostly because of continual distribution cuts.)

This fact leads to my first law of closed-end-fund investing — never buy a new closed-end fund. Give it time, at least a couple of years. We want proof that a fund is capable of sustaining its high-yield distribution. Many prove otherwise. BlackRock has proved it can. The evidence is found in continual distribution increases and a rising share price.

Though I don’t rely on Morningstar to perform my analysis, I will note that the fund-rating agency rates the BlackRock fund a five-star fund — its highest rating. Morningstar’s rating is a rarity among closed-end funds.

As with all of our Shadow Fund recommendations, we expect to profit from the high-yield distribution BlackRock pays today. We expect to profit tomorrow from a rising portfolio value (and rising share price) and a tightening of the share-price discount to NAV.

History has shown that buying when everyone is selling is frequently the opportune time to buy and profit from a closed-end fund. I expect the BlackRock Health Sciences fund to adhere to form.