In February, publicly traded Altus Midstream merged with privately held EagleClaw Midstream to create the only pure-play midstream company operating in the Texas Delaware Basin, notes Tim Plaehn, editor of Monthly Dividend Multiplier — and a participant in The Interactive MoneyShow Virtual Expo, July 26-28. Register here for free.

The Delaware is one of the more prolific production regions in the larger Permian Basin. The newly combined company, Kinetik Holdings, Inc. (KNTK), has tremendous prospects for growth.

Business Overview

In the Delaware Basin, Kinetik operates water takeaway pipelines, natural gas pipelines, natural gas processing, crude oil gathering, and storage. The company’s natural gas pipelines, NGL pipelines, and crude oil pipelines bring energy commodities out of the basin.

According to first-quarter results, the midstream logistics of gathering water, gas, and oil from the wells generated 65% of Kinetik’s EBITDA. Pipeline transport chipped in the other 35%.

In the logistics segment, the company processed 1.1 billion cubic feet per day (cfpd) of natural gas, 68,000 barrels per day (bpd) of crude oil, and 152,000 barrels of water per day. Pro-forma EBITDA came in at $191 million with distributable cash flow of $145 million, providing 1.5 times dividend coverage.

Growth Prospects

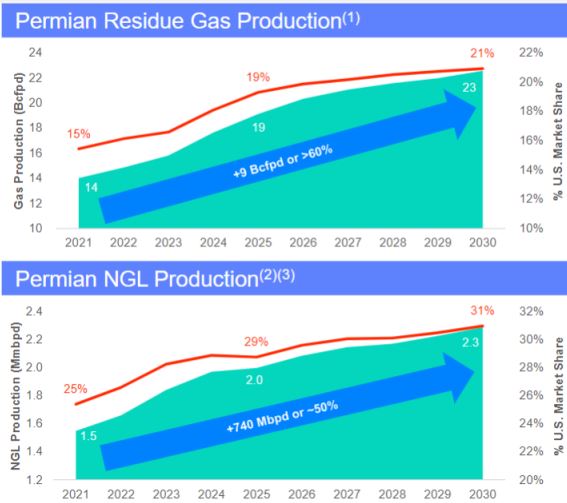

The Delaware Basin is at capacity for natural gas and NGL processing. Bringing on new projects will take years. This is where Kinetik stands out from the midstream crowd. Crude oil producers will see growing residual natural gas from their wells.

Kinetik’s in-basin natural gas processing, the Diamond Cryo facility, is being upgraded to handle two billion cfpd. As noted above, in the first quarter, they processed 1.1 billion cfd. During the latest earnings call management noted they have already contracted 450,000 cfpd of the soon-to-be-added capacity. The company is also expanding capacity on two Basin-to-Gulf Coast pipelines.

The bottom line is that Kinetik is uniquely positioned to rapidly increase capacity to serve Basin upstream producers with little or no competition from other midstream companies.

Investment Considerations

KNTK will now pay a $0.75 quarterly dividend following a two-for-one stock split in June. The shares yield about 7.0%. Management has already guided to at least 5% annual dividend growth.

This stock gives more energy sector exposure to our portfolio, a very attractive yield, and good visibility for dividend increases. It’s an excellent addition to the Monthly Dividend Multiplier portfolio. (Disclosure: Tim Plaehn has a personal long position in KNTK.)