The Dow stocks are a good list to look for investors desiring income. The list contains many established companies with safe dividends and demonstrating an ability to pay one for long periods, suggests Prakash Kolli, editor of Dividend Power.

So far, 2022 has not been a good one for many stocks. The Growth, Technology, and Consumer Discretionary categories did well during the pandemic. However, inflation, rising interest rates, and a return to normal caused investors to become more risk-averse. As a result, the major indices are either in correction or bear market territory.

However, one group of stocks has performed well as a group. The 2022 Dogs of the Dow are up 1.1% year-to-date (as of this writing), far better than the S&P 500 Index or Nasdaq. However, several of them still have high dividend yields and are at desirable levels for investors seeking income to live off dividends.

Below, we discuss three Dow Industrial Average stocks for income.

Dow (DOW)

The first Dow stock for income is Dow, the company. It traces its history to more than 125 years ago. The company has grown into one of the largest global chemical companies through acquisitions and reorganization.

The company acquired Union Carbide in 2001 and Rohm & Hass in 2008. Next, in 2015, Dow merged with DuPont forming DowDuPont, followed by the acquisition of the remaining interest in DowCorning. In 2019, the company de-merged, forming Corteva, Dow, and DuPont du Nemours.

Today, Dow is a maker of commodity chemicals with three operating segments: Packaging & Specialty Plastics, Industrial Intermediates & Infrastructure, and Performance Materials & Coatings.

The company generated $58,350 million of revenue in the last 12 months, with gross margins in the high teens. Demand collapsed during 2020, but the rapid recovery in 2021 gave Dow pricing power and led to solid revenue growth.

Although the company grows organically as a commodity chemical producer, it is sensitive to the economic cycle. Additionally, high oil and other input prices affect margins and thus profitability.

The current Dow only has a short operating history. The dividend increased once since the de-merger but has remained constant since 2020. But the company is the highest yielding "Dog of the Dow" with a dividend yield of approximately 5.4%, three times the average for the S&P 500 Index. In addition, the dividend is safe with a conservative payout ratio of about 28%.

Dow’s stock price has declined since the fear of recession has increased, and commodity chemical demand may decrease. The stock has fallen ~23% since early June, pushing the forward price-to-earnings ratio (P/E ratio) to about 6.6X. Investors are getting a high-yield stock at a relatively low valuation.

Verizon Communications (VZ)

Verizon is one of the successor companies of the original AT&T breakup. It is the second Dow stock for income. The company started as Bell Atlantic, but after the merger with GTE, it changed its name to Verizon. Today, the telecom giant is one of three market leaders in wireless in the US. Verizon’s network covers 99%+ of the US population.

Verizon’s business is vast with about 115 million retail wireless connections, of which ~91.4 million are postpaid, and the remainder are prepaid. Verizon’s scale makes it an oligopoly with AT&T (T) and T-Mobile (TMUS), which combined have 90%+ of the prepaid market.

In addition, it has seven million broadband connections, including ~6.6 million FiOS connections. The company has exited the fixed wireline market except in the northeast.

Verizon earned $134,300 million in the last twelve months, of which about 75%–80% is from the wireless business. Much of the company’s revenue is recurring and arguably inflation and recession-resistant. Consumers and businesses are less likely to give up cell phone service, which is a necessity.

Although Verizon has a stable revenue stream, it does not see much organic growth. Revenue growth averages about 1% to 2% annually. In addition, a significant acquisition or merger is unlikely based on the risk of reduced competition. However, Verizon has grown through bolt-on acquisitions like Tracfone and XO Communications.

The main argument for owning Verizon is the 5.0%+ dividend yield combined with consistent dividend growth and solid dividend safety. Verizon is a Dividend Contender with 18 consecutive years of increases. The dividend growth rate is remarkably steady at about 2% annually. In addition, the relatively low payout ratio of ~47% means the yield is safe.

The stock price is down only about 6.4% YTD and down 11.7% in the trailing 1-year. Furthermore, the valuation is only about 9.4X, below the 5-year and 10-year range. As a result, investors are getting an undervalued blue-chip Dow Jones stock yielding more than 5%.

International Business Machine (IBM)

IBM is one of the largest global IT services companies and is the third Dow stock for income. It has recently gone through significant changes by acquiring Red Hat and divesting its Managed Infrastructure Services business. Today, IBM focuses on hybrid cloud, software, consulting, and mainframes. The company is the leader in mainframes with 90%+ market share.

Total revenue was $57,637 million in the last twelve months after accounting for the divesture of Kyndryl. Revenue is divided approximately into Sofware (~42%), Consulting (~29%), Infrastructure (~26%), with the rest from Financing and Other.

The company grows organically by selling more services and software to its large customer base. Additionally, IBM is conducting many tuck-in acquisitions for AI, security, cloud, and consulting, adding revenue and talent. Some recent additions include Rego Consulting, 7Summits, Bluetab, BoxBoat, Waeg, Turbonomic, SXiQ, and Envizi.

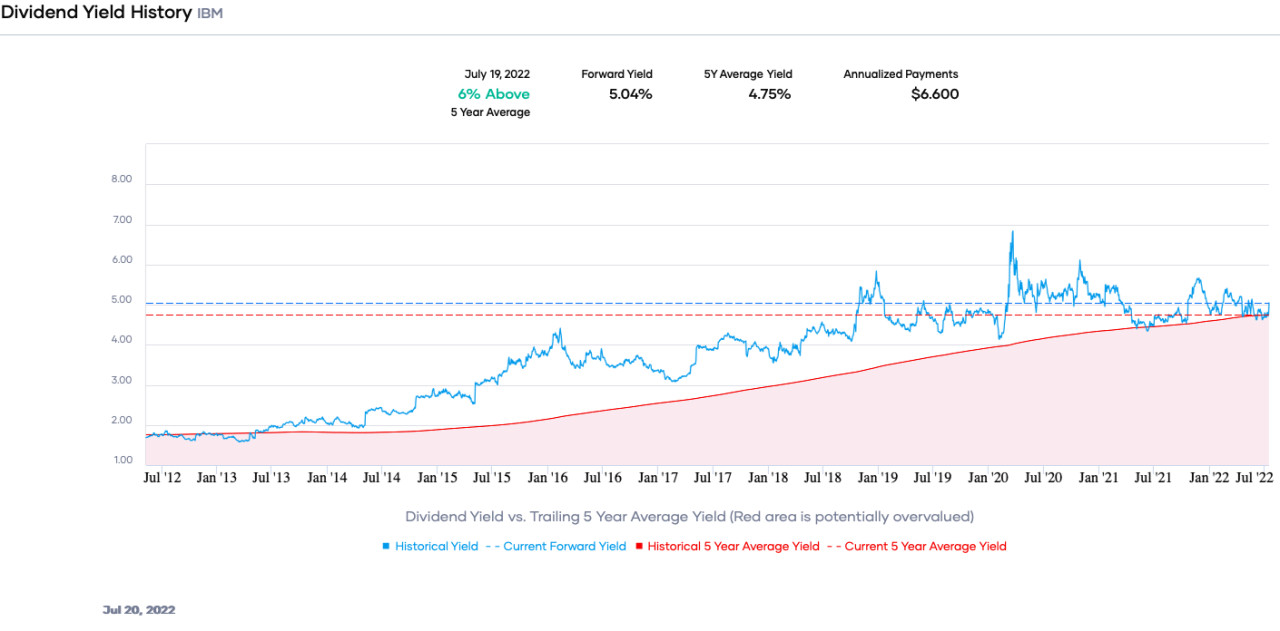

IBM is not the first company that comes to mind as an income or dividend growth stock. However, the dividend yield is ~5.0%, and the company is now a Dividend Aristocrat with 27 years of increases.

The payout ratio had risen but is now a more acceptable 68%. However, dividend growth has slowed to less than 1% annually as IBM focuses on deleveraging and growth.

Despite the bear market, IBM’s stock price is down about 5% for the year and 3.4% in the past 1-year. Moreover, the valuation has ticked up to about 13.9X at the higher end of the 5-year range, but IBM is not overvalued. (Disclosure: Prakash Kolli is long IBM.)