Some companies will prosper if inflation and rising interest rates persist long then we expect. One that could prosper more than most — Ares Capital Corp. (ARCC), notes Steve Mauzy, editor of Personal Wealth Advisor.

Ares Capital is the leading business development company (BDC). It is the best of its breed as measured by market capitalization, total assets, and quality of assets.

BDCs are similar to banks. They are lenders, except they lend to businesses exclusively (no consumers). BDCs invest in private and public companies. They provide permanent capital to these companies through equity, debt, and hybrid-instrument financing.

Smaller companies are the target market, because it is the mandated market. A BDC must invest at least 70% of its assets in private or public U.S. companies with market values of $250 million or lower. These companies are often young businesses seeking financing to grow or businesses enduring financial difficulties.

Ares Capital does a lot of lending to a lot of companies. Its investment portfolio is valued at $21.2 billion. The portfolio is composed of loans and equity investments in 452 companies. Diversity reduces risk. Ares Capital’s portfolio is diversified across asset classes, industries, and geographic locations.

BDCs are income machines for investors because of another mandate. They must distribute at least 90% of their profits to their shareholders. By complying with this mandate, BDCs avoid paying corporate income tax on their profits.

High income to you is the by-product of the mandate. Many BDCs pay dividends that yield two-to-three times the dividend yield of most banks. Ares Capital pays a dividend that yields 9.0% as I write.

Ares Capital resembles a bank; it makes money like a bank. It borrows at one rate (lower) and lends at another rate (higher). Profits are earned on the spread, which can be impressive compared to the spread earned by most banks.

Ares Capital’s weighted average annualized yield on its total investment portfolio was 8.6% at the end of the latest reported quarter. The weighted average interest rate on its debt (its costs) was 3.6%. Ares Capital’s spread, 5.0%, is double that of most large commercial banks.

Business has been good this year. Ares Capital reported solid second-quarter results. Total investment income posted at $479 million, up by $20 million, or 4.3%, from the year-ago quarter. This led to a net GAAP income of $111 million, and core earnings per share (EPS) of $0.46.

The potential for even more investment income and EPS is why I like Ares Capital today. Roughly 87% of its debt portfolio (and debt investments constitute 90% of the total portfolio) is floating rate. When interest rates rise, Ares Capital can adjust the interest rate higher on its loans, thus collecting more investment income.

On the other side of the balance sheet, the liability side, 72% of the debt that Ares Capital owes is financed with fixed-rate unsecured notes. Interest rates might rise, but Ares Capital’s interest rate expense will remain relatively stable.

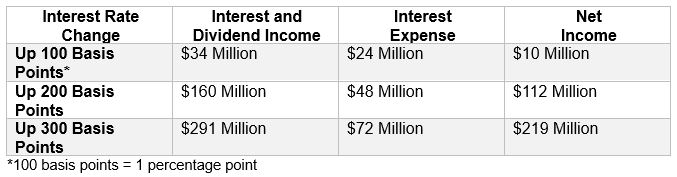

The floating-rate/fixed-rate dynamic is intriguing in this market. Rising interest rates are mostly all good from Ares Capital’s perspective. Management tells us so with its projections. Rising interest rates lead to rising net income. Rising net income, in turn, leads to rising dividends.

Ares Capital is an income investment first and that’s not a bad thing in the current environment. Its dividend outpaces the inflation rate, which enables you to maintain your purchasing power, while generating a positive return after inflation.

This isn’t to say that we should rule out share-price appreciation. After all, as the dividend goes, so, too, goes the share price. Buy Ares Capital at the market price.