With the major market indexes down 20% or more from their recent highs — and the NASDAQ Composite and Russell 2000 down more than 30% — investor sentiment has shifted toward income from growth, notes Steve Mauzy, editor of Dividend Confidential.

It’s understandable that investors should switch their attention to the "bird in the hand" as opposed to the two in the bush while in a bear market. Income is tangible, growth is speculative.

Income tends to soothe nerves frayed by volatile price swings. If the income is high enough to maintain purchasing power, especially given inflation today, all the better. The good news is that we found a new high-yield closed-end fund that soothe nerves and maintains purchasing power.

Thornburg Income Builder Opportunities Trust (TBLD) is that fund. It is new to the closed-end fund (CEF) scene. Its shares were floated in October 2021. The fund’s shares have traded publicly for only a year.

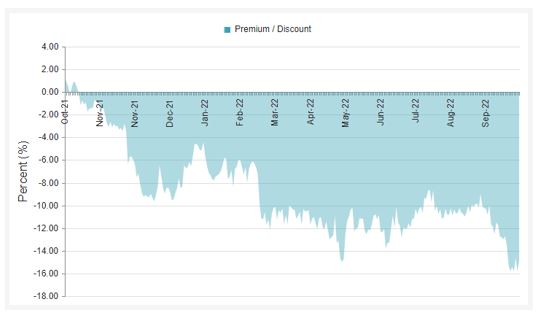

It IPO was favorably timed for Thornburg, but less so for investors who bought during the first days the fund traded publicly. The shares hit the market at $20.00 each a year ago. A year later, they trade near $13.00.

The fund’s net-asset value (NAV) is $480 million. The portfolio is composed mostly of large-cap stocks and debt. Stocks account for 67% of the portfolio. Debt accounts for the other 33%. The fund is, if anything, well diversified. Roughly 28% of the portfolio is composed of U.S. stocks. Top-10 holdings include Qualcomm (QCOM), Microsoft (MSFT), and Pfizer (PFE).

U.S. debt composes 24% of the portfolio. This includes corporate and government-agency bonds. The fund also owns mortgage-backed securities — both commercial and residential. The other 48% of the fund is allocated to international equities and debt. The international allocation covers all the major markets in Europe, South America, and the Far East.

The Thornburg fund checks all the right boxes: high-yield income, a steep discount to net-asset value (NAV) and exceptional value. The Thornburg fund shares are priced at a 14.9% discount to NAV. The shares were trading at a 1.2% premium a year. Relatively speaking, the discount is significant. The discount is near the all-time high.

Income is the leading attraction. The fund pays $1.25 per share in distributions annually. The distributions are paid monthly at $0.1042 per share. The annual distribution generates a generous 9.5% yield on investment.

History has shown that buying when everyone is selling is the best time to buy and profit from a closed-end fund. One caveat: Because the Thornburg fund is relatively new, I’m slotting it into the “aggressive” category.

I do that because of the relative newness of the fund. The lack of a track record adds an element of risk that a history will negate. That said, I expect a good outcome with the Thornburg fund.