Four months ago, I expressed my frustration with Wall Street’s lack of enthusiasm for International Business Machines (IBM), a holding in our growth portfolio, recalls Jim Pearce, editor of Personal Finance.

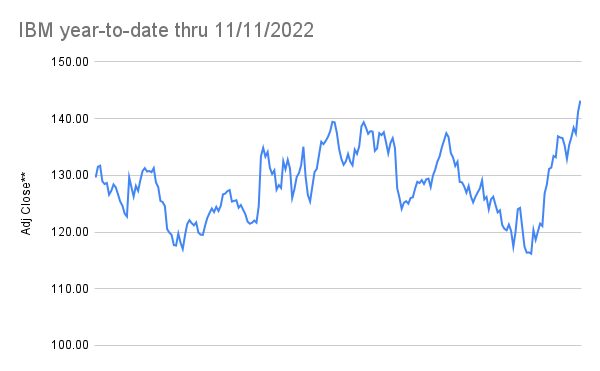

Despite posting solid fiscal 2022 Q2 results, IBM suffered a steep decline. By October its share price fell below $120, its lowest point since late last year. The strong U.S. dollar was partly to blame for IBM’s poor reception, which dilutes the value of the company’s considerable overseas income.

I said then, “I’m okay with it since that is something over which the company has no control, and it is executing well on the factors over which it does have control. Eventually, the dollar will weaken at which time IBM’s profitability could soar.”

Turns out, we didn’t have to wait for the dollar to weaken for Wall Street to abruptly change its tune on IBM. After releasing even stronger Q3 results (ended September 30) on October 19, IBM has staged an impressive rally that pushed its share price to its highest reading in over a year. That put the stock in positive territory for 2022 and has it pushing up against long term technical resistance that it may soon break through.

What was so different about IBM’s third quarter results that got Wall Street so excited? It was revenue growth of 15% on a constant currency basis (6% after adjusting for currency conversions) that surprised the market. In particular, the company’s hybrid cloud business, on which it has staked its immediate future, grew 20% on a constant currency basis over the past year and 15% after currency conversions.

Currency conversion was less of a problem for IBM’s hybrid cloud performance since more of that is transacted in U.S. dollars. The reasoning is simple; if IBM can grow its biggest segment at that rate while only losing a small fraction of it to currency conversions, then its operating margins and earnings metrics should grow faster than anticipated.

The company confirmed that hypothesis by upping its guidance for revenue growth this year. Without specifying a range, IBM stated that it “now expects constant currency revenue growth above its mid-single digit model.”

Combined with good news on the inflation front in the form of a lower-than-expected increase in the Consumer Price Index (CPI) for September, IBM’s overseas sales may contribute more to its performance next year on an adjusted basis than anticipated.

In short, IBM’s third quarter results and guidance confirmed what I have believed all along. After unloading its large but gradually diminishing services business last fall by spinning it off as Kyndryl (KD), IBM is free to focus on its faster growing and more profitable hybrid cloud business.

For that reason, Wall Street is willing to assign a higher multiple to IBM’s future earnings. At the end of last year’s third quarter, IBM was trading at a forward earnings multiple of less than 12. At the end of this year’s third quarter that multiple was nearly 15, a 25% relative gain. That fact alone explains most of IBM’s share price appreciation during the past year.

IBM has also been the beneficiary of Wall Street’s abandonment of “new tech” which has witnessed huge share price drops in former tech sector darlings Amazon (AMZN), down 40% this year, Alphabet (GOOGL) losing 33%, and Meta (META) giving up a whopping 66% of its share price in 2022.

Despite those big price drops, those three companies still trade at higher forward earnings multiples than does IBM, but the difference is considerably less. In addition, none of them pay a dividend while IBM’s most recent quarterly cash dividend of $1.65 equates to a forward annual dividend yield of 4.6% even after its recent run up the charts.

It appears that Wall Street is starting to figure out that IBM’s more focused growth strategy is a keeper. The fact that it can execute that strategy while generating $10 of consolidated free cash flow that can be used to pay dividends and fuel growth makes it especially attractive while the economy is barely growing at all so IBM remains a buy up to $150.