When I last updated Gladstone Capital (GLAD) in late March, the Fed had just made its first rate hike of 2022 of 25 basis points, explains Jim Pearce, editor of Investing Daily's Personal Finance.

At that time, the Fed’s “dot plot” did not include another 400 basis points of rate hikes before the year was over. Nevertheless, Gladstone has generated remarkably consistent results despite the Fed’s unexpected hawkishness.

On November 14, Gladstone released its fiscal 2022 Q4 and year-end results (ended September 30) which included a 15.6% increase in total investment income compared to the previous quarter. Total expense grew by 23.8%, resulting in a 7.6% gain in net investment income.

For the full fiscal year, net investment income grew 23.6%, which allowed the company to increase its monthly cash distribution in October to 7 cents per share, up from 6.75 cents per share. As a result, Gladstones dividend has been fully restored to what it was prior to the outbreak of the coronavirus pandemic.

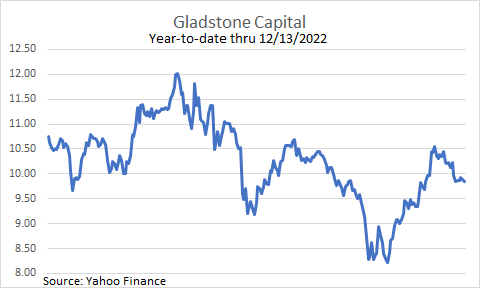

What has not been fully restored is Gladstone’s share price, which peaked above $12 in April. Six months later it fell below $9 as the Fed raised rates. By November it was back above $10 after third quarter GDP growth was positive and inflation started to subside.

Although the company did not provide guidance for fiscal year 2023 its president, Bob Marcotte, insinuated that another dividend hike may soon be in the offing: “We expect the current interest rates as well as more favorable spreads and conservative leverage metrics of the current lending market to sustain this earnings momentum and support potential increases to the common distribution rate in the coming quarters.”

I am surprised that Marcotte felt compelled to make such a statement. At a share price of $10, the forward annual dividend yield for GLAD works out to 8.4%. Until the share price moves higher, the company may be better off using its excess cash flow to pay down debt. Instead, it increased one of its credit lines by $20 million in October.

One reason why Gladstone’s share price has been less volatile than most other BDCs is that 89% of its loans are secured by collateral, with 71% of them holding a first lien on that position. If a recession does upend the small business sector in 2023, at least Gladstone should be able to recoup most of its investment capital.

Also adding stability to Gladstone’s share price is its diversified loan portfolio, which is evenly spread across a broad spectrum of industries. Its exposure to the automobile and oil & gas sectors, which are both vulnerable to extreme shifts in demand, totals only 7%. Until the threat of a recession becomes more apparent, Gladstone Capital remains a buy up to $12.