Many years ago, I learned that one good way to make money in the market is to understand the consensus view and then figure out where it is most likely to be wrong. Not that the consensus is always wrong – it’s usually right BUT fully priced into the market, writes Michael Murphy, editor of New World Investor.

That’s why I was interested in a recent Reuters poll of 116 economists that said a couple of interesting things. First, they said the risk of a US default over the debt ceiling was higher compared to prior stand-offs. That surprised me. The risk of a default in prior stand-offs was 0.0%, and the risk of a default in this one also is 0.0%.

The shameful play we have to watch over and over is manufactured political drama. Wall Street uses it to shake out some rubes and get a little cheap stock to sell when the debt ceiling is miraculously raised at the last minute, thus funding their kids’ summer camp.

But the other finding was more interesting. Over 60%, or 75, of the economists expect the Fed to hold the Fed funds interest rate steady this year despite the expected recession. I think they’re right. But the futures markets are pricing in at least a 50-basis point (0.5 percentage point) cut by the end of 2023.

Fourteen expected the funds rate to be even higher than 5.00%-5.25% at some point this year. Three of them also had a cut penciled in to take it back to the current level. Thirty predicted no hike and at least a 25-basis point cut. I think they’ll be disappointed, although being wrong by 25 basis points probably doesn’t matter much.

I think we’re in for two to four quarters of slightly positive or slightly negative GDP – the shallow recession that frustrates both bears and bulls. It’s not a time for extreme positions.

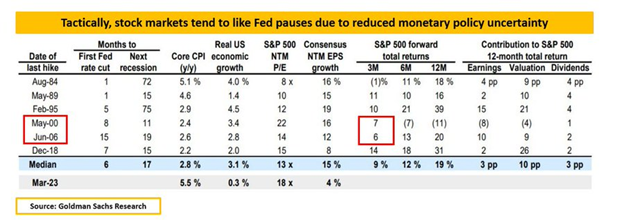

If I’m right that the Fed pauses at the June 14 meeting, how did markets historically trade during Fed pauses? As monetary policy uncertainty is reduced, the S&P 500 tends to rally in the first three months after the pause. After that, are we in 2001 or 2007?

Well, both institutional money managers and individuals have been negative and underinvested all year. They are worried about the economy and, lately, the health of the US banking system. Deutsche Bank showed overall equities positioning across systematic funds is at its highest level since December 2021, while stock market exposure among active managers is close to a one-year low.

But volatility has fallen dramatically this year as fears about US interest rate rises and the health of the global economy have eased. The VIX Fear & Greed Index, which reflects expected stock market swings over the next month, has closed below its long-term average 57 times so far this year, compared with just 23 times in the whole of 2022.

Low exposure to stocks has meant 2/3 of actively managed mutual funds failed to beat their benchmark in the first quarter as portfolio managers were caught off guard by the rally, according to Bank of America. They know they need to catch up.