Tractor Supply (TSCO) is the largest operator of farm and ranch stores in the United States. Stores target recreational farmers and ranchers in primarily rural areas. The 85-year-old company operates 2,181 Tractor Supply stores in 49 states and 192 Petsense stores in 23 states, highlights Tom Hutchinson, editor of Cabot Dividend Investor.

It’s a significant company and a serious powerhouse in its area. The stores are huge with an average of 15,500 square feet of selling space and a similar amount of outside space. It does have some competition from big boys like PetSmart and Lowe’s (LOW), but it offers a uniqueness that makes it its own destination for rural customers. It also blows away smaller competitors with size and scale.

The store provides an environment and experience that its customers love. It also has the advantage of being partially insulated from e-commerce competition by offering many products that serve an immediate need or are expensive to ship.

Here’s a sample of the things people buy at Tractor Supply:

- Clothing

- Power tools

- Equine and pet supplies

- Fencing

- Tractor/trailer parts

- Welding and pump services

- Lawn and garden supplies

- Sprinkler and irrigation parts.

In 2022, here’s how overall company revenue was distributed among the product categories: Livestock and Pet (50%); Hardware, Tools, and Truck (19%); and Seasonal Gift and Toy (21%). Tractor Supply has a diversified product offering that enables the store to thrive in just about any economy. That’s a big part of the reason the company has been able to generate 31 consecutive years of sales growth.

Resilience was evident in the second quarter. It’s basically a lousy consumer environment with tepid growth and inflation, at least in rural areas. As a result, sales of bigger-ticket and seasonal items struggled.

But the company still grew net revenue 7.2% and earnings per share (EPS) by 8.5% versus last year’s quarter. Pet and livestock sales grew at twice the rate of its competitors, and it also got double-digit growth from its consumable, usable, and edible (CUE) product subcategory.

Tractor anticipates adding 80 new stores in 2024 and an average of 90 stores per year thereafter. That’s serious 37% store growth over the next 10 years. Tractor Supply had anticipated growing the bottom line by 8% to 11% per year for the next decade. But it may be more now.

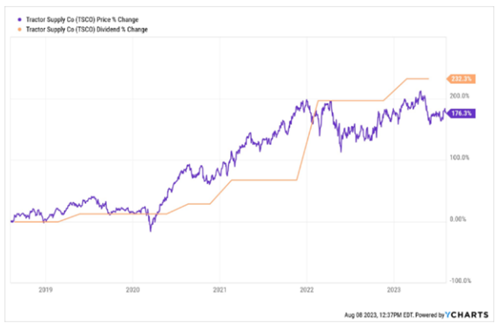

TSCO currently pays an annual dividend of $4.12 per share, which translates to a 1.8% yield at the recent price. The payout is well supported with a 39% payout ratio where retained earnings provide expansion money, and the company is buying back shares.

Recommended Action: Buy TSCO.