The Focus Stock of the Week ended September 10 is Eli Lilly and Company (LLY), which carries CFRA's highest investment recommendation of 5-STARS, or Strong Buy. We see several catalysts that make us bullish on shares of LLY in the medium to long term, notes Sel Hardy, analyst at CFRA Research.

LLY is a large producer of brand-name prescription drugs covering a wide range of therapeutic areas, including endocrinology, which includes its diabetes drug portfolio that generates roughly half of its total revenue, as well as cardiovascular, immunology, neuroscience, and oncology. The firm's top-selling drugs include Trulicity, Verzenio, Taltz, Jardiance, Humalog, and Humulin. Collectively, these six drugs comprise 62% of total 2022 sales of $28.5 billion.

We are increasingly optimistic on LLY's many ongoing efforts, including late-stage therapies, such as Donanemab (for Alzheimer's disease), Pirtobrutinib (for certain forms of leukemia and lymphoma), and Tirzepatide (obesity along with heart failure and cardiovascular outcomes).

Eli Lilly and Co.

Such innovations could complement LLY’s 10 key current drugs, which represent about 70% of LLY’s total revenues. Essentially, we think the thesis for LLY rests strongly on future pipeline development with ongoing growth from current key products. Over the next five years, LLY will face several key exclusivity expirations that it hopes to offset with growth in newer drugs.

LLY's development pipeline includes potential new treatments for a wide range of conditions including diabetes, obesity, pain, pancreatic cancer, Parkinson's, Crohn's, and Alzheimer's diseases. The most critical upcoming regulatory event, in our view, is the potential full FDA approval of Donanemab for Alzheimer's disease by the end of 2023.

LLY applied to the FDA in Q2 2023 to receive traditional approval for its Alzheimer's drug following promising Phase III clinical results, which showed a significant slowdown in cognitive and functional decline for early-stage Alzheimer's disease patients. The company has been focusing major acquisition dollars on promising development assets.

In keeping with a focus on growing its oncology portfolio, in February 2019, LLY acquired Loxo Oncology for approximately $8 billion. In February 2020, LLY closed the acquisition of Dermira, a biopharmaceutical company developing new therapies for chronic skin conditions, for approximately $1.1 billion. And in January 2021, LLY acquired Prevail Therapeutics, a gene therapy platform, for $880 million.

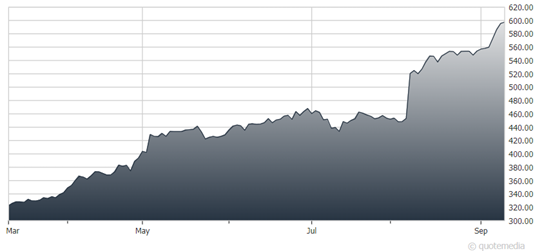

Our 12-month target price is $614, reflecting a 51.1x multiple applied to our projected 2024 EPS of $12.02, a premium to LLY's historical forward P/E average. This is justified by LLY's strong revenue and earnings growth potential, as well as its robust balance sheet.

Key risks to our view include slower-than-expected growth in prescription drug demand, a significant downturn in the global economy negatively impacting LLY's sales, intense generic and biosimilar competition, as well as unfavorable regulatory or legal developments.

Recommended Action: Buy LLY