While our intermediate to long-term outlook for natural gas is cautious, we see the potential for a sizable spike in gas prices this winter due to short-term supply/demand imbalances, explains Elliott Gue, editor of Energy & Income Advisor.

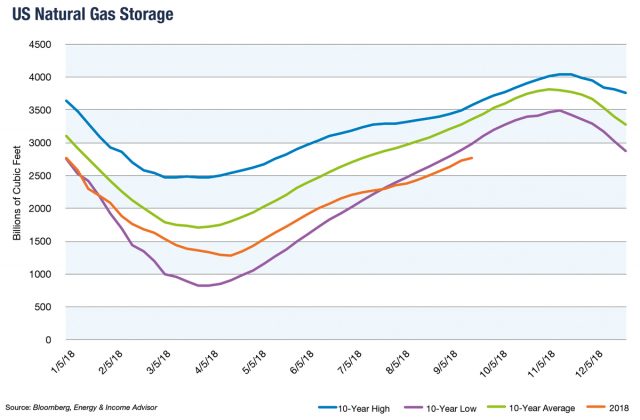

This chart below shows total natural gas in storage in the US each week year-to-date in 2018. I’ve also included lines showing the 10-year seasonal average, 10-year maximum and 10-year minimum storage levels for each week of the year.

The winter months are the season of peak demand for natural gas so there’s a clear seasonal pattern in gas storage. Historically, gas in storage bottoms out in early April, following the winter heating season and producers inject gas into storage through the summer months. Storage levels typically peak in early to mid-November and then begin to draw down once again through the cold weather months.

It’s particularly crucial to understand where gas inventories top out in November and bottom out in April. That’s because storage significantly below average heading into a season of peak demand acts like an accelerant, setting the market up for a significant rally on any hint of cold weather.

In contrast, if natural gas inventories enter winter heating season at over 4 trillion cubic feet (near 10-year highs) gas prices should struggle to see significant upside over the winter months, even amid cold weather, as ample storage cushions any near-term heating-driven spikes in consumption.

In short, with natural gas storage levels as low as they are today, it will not take much of a catalyst to drive gas prices higher this winter.

The stock on our Focus List with the heaviest natural gas weighting is Canada’s Peyto Exploration & Development Corp (Toronto: PEY; OTC: PEYUF).

The company has consistently drilled wells in the Deep Basin region of Alberta at some of the lowest costs in the world. Second quarter total cash costs excluding royalties came in at just 79 cents per thousand cubic feet (CAD4.73 per BOE).

The company is not immune to weak natural gas prices, shutting in 15 thousand cubic feet per day (MMcfe) during the quarter to avoid having to sell at 97 cents per MMcfe. That curtailment likely carried over into the third quarter, as AECO hub gas prices scraped as low as 12 cents during the summer.

The current AECO price of USD1.68 is barely half the price of gas sold at the Henry Hub in Texas. Construction of new gas transportation capacity out of Alberta should help reduce that huge price discount in coming years.

But in the meantime, Peyto continues to mitigate the shortfall with a combination of cost cutting and locking down long-term contracted sales in Alberta.

Management’s target of 20 percent of sales to “direct connect” customers should be attainable as the province phases out coal-fired electricity by 2030. The company also projects 40 percent of sales to the US, as pipeline capacity becomes available.

Peyto has a large and growing presence in the Montney and Duvernay shale, which is being unlocked by improved transportation capacity. That includes natural gas liquids, which command a premium price to dry gas. The company is also taking advantage of a strong balance sheet to add drilling lands from cash strapped rivals.

Peyto shares have largely run in place since we added it to the Focus list. That’s actually a strong outperformance of other Canadian producers, particularly those more weighted toward natural gas. We continue to rate the stock a buy up to USD10 for patient investors.