Think the Federal Reserve-fueled rally was a one-day wonder? Think again! Stocks rallied AGAIN yesterday amid ongoing optimism for cheaper money, as did gold. They’re slightly higher in the early going today, too, along with crude oil. Treasuries are mostly flat, while the dollar is up.

Sure, the US Fed pivoted toward a stance favoring future rate CUTS over HIKES. But its foreign counterparts aren’t ready to make that move...yet. Bloomberg reports that the European Central Bank (ECB), the Bank of England (BOE), and others aren’t willing to declare victory over inflation at this time. The central bank in Norway actually hiked rates yesterday.

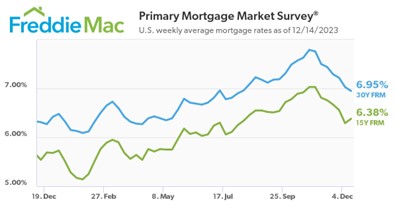

Still, foreign rate futures markets are pricing in eventual cuts on the global stage next year. And while I’m on the subject of interest rates, it’s worth noting that the average 30-year fixed rate mortgage now goes for just under 7%. That’s the first time this benchmark US rate has dropped below that key level since August. It’s still up from 6.31% this time last year, though.

Source: Freddie Mac

Shares of drugmaker Pfizer (PFE) have been in freefall over the past year amid shriveling demand for its Covid-19 vaccine and Paxlovid pills. This Wall Street Journal story covers how the company is responding to the 45% YTD drop in its shares, which left them trading at a 10-year low. Among its initiatives: Laying off thousands of workers, acquiring the biotechnology firm Seagen (SGEN), and promising to speed drug development.