The stage is set for Q3 earnings to be the third consecutive quarter of bottom-line growth above 20%, a feat not achieved since 2010 when the market was rebounding from the financial crisis (i.e. cycling extremely low/negative growth comparisons), writes Lindsey Bell.

This time around, the solid record of growth has been driven by tax reform and fiscal stimulus that aided in returning sales growth to double digits and helped drive margin expansion. When combined with buybacks, bottom-line growth has been significantly better than expected at the start of the year.

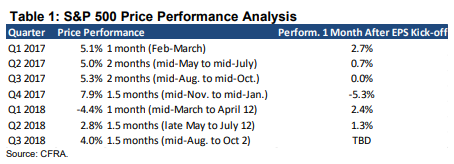

As we head into the reporting period, the S&P 500 (SPX) is coming off a 7.2% advance in price for the third quarter. The performance is the best quarterly increase year-to-date, but more significant is how much better the results are versus the historic average given the quarter is well-known for being the weakest of the year.

Going back to 1990, the S&P 500 has declined by 0.2% on average in the third quarter; in the fourth quarter, which includes the five-week period when third quarter results are reported, the index has advanced by 5.0% on average. Stronger than expected economic data, solid second quarter results and positive trade news helped drive upside in the market.

Over the past seven quarters, strong market performance in the month to two months prior to the reporting period beginning results in muted performance for the market the month after companies begin announcing earnings.

One might argue that estimates have been reduced going into the quarterly reports, and that guidance or preannouncements have been more negative than usual, thus the bar has been set low for earnings to be better-than-expected, which will push stocks higher.

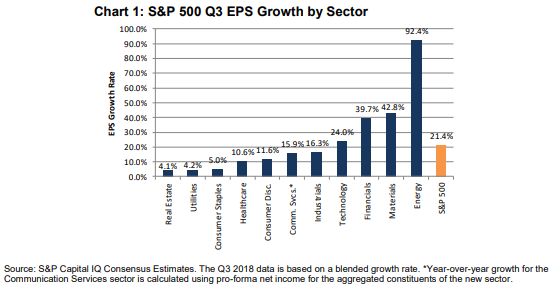

Third quarter year-over-year growth estimates have declined by about 100 basis points during the quarter, to 21.4%, which is a stark contrast to the increase in growth rates recorded as the first two quarters of 2018 progressed.

The decline, however, is still significantly lower than the five-year average reduction of 390 basis points during a quarter. Perhaps the third quarter move signifies a change in sentiment regarding the probability for earnings outlooks to continue to move higher as the fourth quarter ushers in the final stage of the tax reform benefit, and as $200 billion in additional tariffs on Chinese goods went into effect at the end of September.

Fourth quarter growth estimates have been reduced by 70 basis points since mid-August.

Individual stock and overall market reaction will primarily be driven by management guidance for the final quarter of the year and any commentary they provide on expectations for 2019. While we are in very early innings, guidance has been conservative thus far, with several companies lowering guidance and the ones that raise guidance taking a cautionary tone.

It is the view of CFRA that corporate management teams have no incentive to be overly optimistic given the current tariff situation, which could escalate as we enter the new year. We expect that tariffs will be the most highly discussed topic on earnings calls. The dollar will also likely be heavily discussed as it has been a cause for several revenue misses and lowered guidance thus far.

The consensus projects third-quarter growth at 21.4% on EPS of $40.08. Most sectors’ growth rates have been reduced since mid-August, with the largest declines coming in the energy and materials sectors. Despite that, this is expected to be the third quarter in a row for earnings growth of greater than 20%.

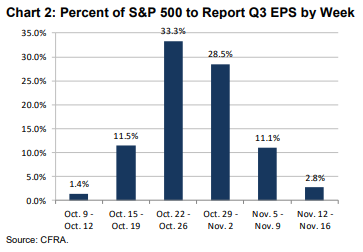

The few companies that already reported have announced strong bottom-line results, with only two of 19 companies missing EPS estimates. Said another way, 90% of companies beat projections. On sales, 68% of companies have beat expectations to-date, below the 87% beat rate at this time last quarter. Both beat rates are historically strong for this early in the season. Stocks haven’t reacted favorably, declining 0.5% on average, led by consumer staples and consumer discretionary.

Historically, quarterly growth ends 3.5%-4.5% points higher than the initial estimate, which would mean growth of more than 25% would be a possibility in the third quarter, following the 25.2% increase recorded in the second quarter.

EPS growth hasn’t fallen short of expectations since first quarter 2009 and six of the last eight quarters have reported better-than-average beat rates (of 5.7% in Q2 2018, 7.0% in Q1 2018, 4.4% in Q3 2017, 4.6% in Q2 2017, 5.8% in Q1 2017 and 5.2% in Q3 2016).

Q3 EPS growth by sectors

Digging into third-quarter earnings growth, the energy sector will lead with 92.4% growth as it continues to emerge from a two-year earnings recession.

Materials, with growth of 42.8%, is the second best in the index as the group is benefiting from higher commodity prices and higher volumes.

After energy and materials, financials and information technology will lead with growth ahead of the index’s 21.4% rate. It will be the ninth consecutive quarter the information technology sector recorded double-digit growth. In each quarter over the past six quarters, the information technology sector recorded growth of 21% or better.

No sectors are expected to report a decline in earnings. The 21.4% growth rate is above the average growth of about 8% per quarter characteristic of the index prior to the earnings recession.

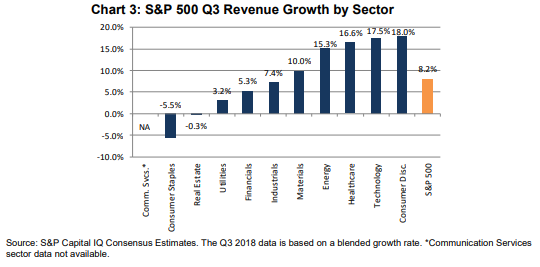

Revenue analysis

On the top line, growth is expected to be in the high-single digits, with analysts currently modeling an 8.2% increase in revenue.

Consumer discretionary, technology, health care, energy and materials lead with double-digit growth rates.

Financials, while projected to be a bottom-line leader, has sales growth pegged at an increase of 5.3% as loan growth has struggled to expand in a robust way and net interest margins remain low by historical standards. Consumer staples and real estate are the only sectors expected to report a decline in sales.

View CFRA, services and research including Marketscope Advisor here.

View brief video interviews with Lindsey Bell of CFRA:

Lindsey Bell’s picks: Apple, AI, Nvidia, Intel, semiconductors here.

Duration: 3:14

Q2, Q3, the worst. Q4 good news here.

Duration: 3:53

Recorded: MoneyShow Las Vegas, May 15, 2018.