We’re coming down to the wire, the last few trading days of 2018. I hope you are enjoying the holiday season, and I wish you and your family all the best ahead of Christmas and New Year’s Day, writes Mike Larson. He's presenting at MoneyShow Orlando Feb. 9.

But let’s face it, neither the month of December nor the year itself were what many bulls were hoping for.

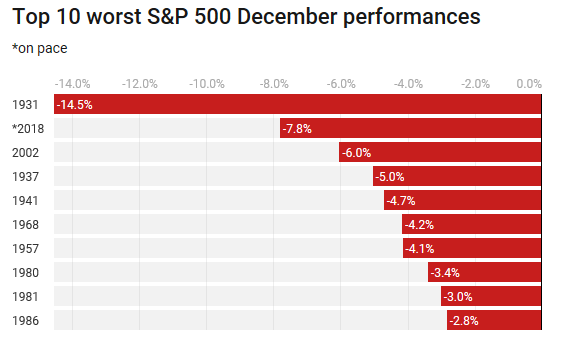

As of earlier this week, the S&P 500 (SPX) was down almost 8% for the month. That put it on track for its worst December since 1931! Yes, that was during the Great Depression.

Source: CNBC

Meanwhile, the Wall Street Journal reported last week that investors were running away from the markets as fast as they could. Investors yanked $39 billion out of global stock funds and $8.4 billion out of investment-grade bond funds in the week ended Dec. 12. That was “the greatest week of redemptions ever,” according to the story.

And if that doesn’t sound grim enough, remember what I said at the end of November: This has been a “Nowhere to run to baby, nowhere to hide” market in 2018. Some 90% of the 70 different asset classes that Deutsche Bank tracks – from stocks to bonds to commodities and everything in between – were losing money for investors at the time.

But seeing as the new year is fast approaching, it’s only natural to wonder what will happen next? Can the bulls expect some relief in 2019? Or were the trials and tribulations of 2018 just a prelude to even worse times ahead?

I’ve always prided myself on telling like it is, whether the news is good or bad. So, I’ll be honest: I believe that anyone expecting the late, great bull market to resume in 2019 is going to be sorely disappointed. This looks, smells, walks and growls like a new bear market. In fact, it’s unfolding just as I predicted eight months and hundreds of Dow points ago.

To understand why that’s the case, you have to appreciate what drove the bull market in the first place ...

First, the Fed and its foreign counterparts engaged in a global print-fest that ballooned central bank balance sheets to more than $20 trillion. At the same time, they cut interest rates more than 667 times globally in the post-crisis era.

Second, the flood of cheap, easy money those measured unleashed didn’t provoke an explosion of “real economy” inflation like in the 1970s. Instead, just like in the last two major easy money cycles, it mostly got diverted into the “asset economy.”

Yet unlike the previous two cycles, the resulting boom/bubble wasn’t mostly contained to dot-com stocks or housing. It grew to become one of the biggest, broadest asset bubbles in history.

It not only swept up traditional assets like stocks, bonds or commercial and residential real estate, but also a whole host of esoteric ones. Think artwork, comic books, NFL teams, baseball cards, even vintage whiskey.

Just one telling example: Heritage Auctions hosted a sale of vintage comics and comic book art in Chicago in May 2018. The total take: More than $12.2 million. That was a world record haul, up more than 17% from the previous record of $10.4 million in 2012.

A single piece of comic art by Frank Frazetta, depicting a horseback-riding barbarian swinging an axe, netted $1.79 million. That was triple the pre-auction estimate and double the previous record for an individual work of art.

Third, after actively encouraging these developments under the Bernanke Fed, policymakers failed to recognize that things were starting to get overheated again and “lean against” that under the Yellen regime.

Indeed, every time the Dow dropped a few hundred points, they would backtrack on plans to unwind their Great Financial Crisis-era policies – even though the crisis ended years earlier.

Fourth, that helped fuel an incredible amount of wild speculation and madcap risk-taking on Wall Street ...

Fund managers herded into high-risk growth stocks to an extreme degree only seen once before in U.S. market history – around the peak of the dot-com bubble.

Investment bankers flooded the public markets with the greatest percentage of money-losing IPO companies ever, and investors were only too eager to ignore the lessons of history and snap them up.

Merger and acquisition volume soared to never-before-seen levels, rocketing 79% year-over-year to more than $1 trillion in the first half of 2018.

And private equity buyers ... flush with so much cheap cash ... paid record-high multiples to earnings to buy out scores of companies. It was enough to make even the reckless corporate raiders of the 1980s blush.

Fifth, U.S. corporations went bonkers in this cycle, just like mortgage borrowers did in the last one, taking advantage of the easy credit environment to issue all the debt they could. Corporate debt outstanding soared 84% to $6.09 trillion last year from $3.31 trillion a decade earlier.

Worse, a huge chunk of those funds were frittered away on unproductive, short-term-focused things like stock buybacks rather than long-term investments in property, plant, equipment, or research and development.

TrimTabs Investment Research said the 2018 tally of buyback announcements just topped $1 trillion. Not only was that an all-time record, it was also up a whopping 64% year-over-year.

In sum, my greatest worry ... but also a growing expectation ... is that this has set the markets up for a “Final Crash.” Not final in that stock prices will never, ever drop again. But final in the sense that this will be the third, broadest, and potentially biggest bust in the “trilogy” (after dot-coms and housing). As such, it will be severe enough to force real, lasting policy change – to get us off the boom/bust treadmill that reckless monetary and fiscal policymakers keep putting us on.

In practical terms, this means 2019 should be another year where playing defense is the best course of action for investors. That means keeping cash levels high, hedging against downside with inverse ETFs, avoiding overloved, overowned, overvalued sectors and stocks, and staying focused on strict risk-management.

Have a happy new year, and I’ll be back in touch with you again in 2019!

Until next time,

Mike Larson

P.S. If you didn't see the news already, I’m participating in the 2019 Money, Metals & Mining Cruise. The Ft. Lauderdale-to-San Juan cruise runs from Dec. 6-14, 2019, on board the Crystal Serenity.

Our host will be Brien Lundin, president & CEO of Jefferson Companies. He's an expert on the gold markets and junior miners. We'll also be joined by other, selected investment experts who are eager to share their knowledge and insights with you.

Interested? Then click here for more details. Or call 800-797-9519 for everything you need to know about pricing, itinerary and more. I hope to see you aboard!

Check out Mike Larson’s Yield Picks OGS and GTY here.

Recorded: MoneyShow Dallas, Oct. 5, 2018.

Duration: 3:15.

Check out Mike’s Defensive Sector Ideas here.

Recorded: MoneyShow Dallas Oct. 5, 2018.

Duration: 7:24.

Check out Mike’s short video, 2 Safe Yield Stock Picks here.

Recorded: MoneyShow San Francisco August 24, 2018.

Duration: 4:42.