The fixed income sector is finally getting a little love. Here, Joon Choi compares the outlook for investment grade bonds vs. high yield bonds.

As investors’ expectation of a recession has been rising in recent months, they are flocking into the fixed income space, driving down long-term yields. Last week, the 10-year Treasury note yield fell to its lowest level in three years (1.53%) and even got close to its historical low of 1.4% in 2012. Whether a recession is looming around the corner remains to be seen, but there may be a sign to avoid high yield bonds. In fact, investment grade bonds may be a better bet than high yield bonds for the foreseeable future.

Overview

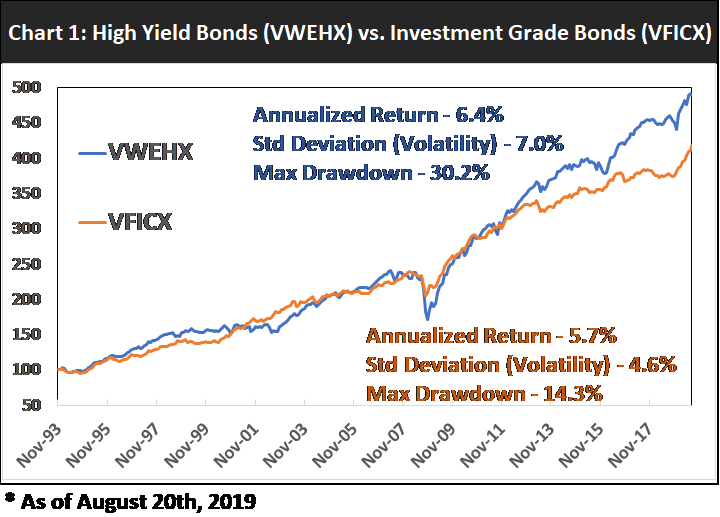

Vanguard has many index funds dating well back to the 1970s and I will be using their funds for my study. I selected the Vanguard High-Yield Corporate Fund Investor (VWEHX) for the high yield representation and the Vanguard Intermediate-Term Investment-Grade Fd;Inv (VFICX) for the investment grade bonds because they both have similar maturity of 5.5 years. Judging solely by SEC yield VWEHX seems like a much better bond space than VFICX: 5.0% vs. 2.5% respectively. However, we need to analyze the longer-term performances of both funds to see if VWEHX is a clearly a better choice.

The Study

I chose monthly total return data for both funds from November 1993 (VFICX inception) and displayed their equity curves (see chart below). VWEHX had an annualized return of 6.4% compared to 5.7% for VFICX but with it achieved slightly higher returns with much higher volatility (7% vs. 4.6%). In addition, the maximum drawdown was more than double for the high yield bond fund (30.2% vs. 14.3%). It appears like 0.7% additional annual return came at the expense of much higher volatility. Notice that both investment vehicles had the same overall return until 2012 when VWEHX started to pull away from its counterpart.

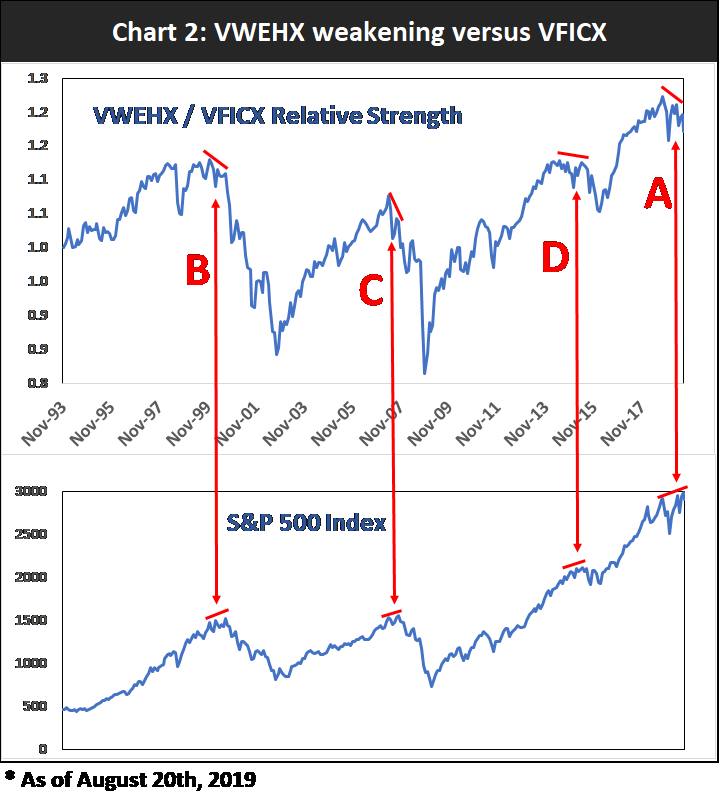

Although both bond categories have been performing well this year, there is an unsettling negative divergence forming between VWEHX/VFICX relative strength and the S&P 500 Index (see point A in chart below). This implies that high yield bonds have started to underperform investment grade bonds even as the stock market is making new highs. This is significant because we have experienced similar divergences in the past.

The first occurred in 1999/2000 during the internet bubble (point B) and the next one in 2007 (point C). The last occurrence was in 2015 (point D). Following each of these divergences we saw significant losses in VWEHX (and continued outperformance by VFICX). Moreover, these divergences also preceded stock market declines in addition to the losses seen in high yield bonds. All four of these divergences are similar in that the unfavorable divergences occurred after extended economic expansions.

Conclusion

Additional monetary stimulus across the globe is giving stock investors hope that a further economic slowdown may be averted. In addition, the Trump administration may embark on wage tax cuts to stimulate the U.S. economy. However, investors seem to be positioning themselves for an unfavorable climate for the stock market as high yield bonds are lagging its investment grade counterparts since last October. It may be prudent to lower exposure in high yield bonds in favor of investment grade bonds, unless you have access to a proven high yield bond models that we employ. I continue to prefer high yields over equities but only with a risk management strategy in place.