If one didn’t know better, you’d never guess that stocks are in the ninth year of the second longest bull market in Wall Street history. The financial skies are blue with nary a single cloud in sight, observes Jim Stack, money manager and editor of InvesTech Research.

Fearful money that has been on the sidelines for years is now finding its way back into the stock market. In other words, it’s a very comfortable time to be invested. And that, in itself, makes us more nervous.

In a renewed show of solidarity, the broader market indexes are uniformly confirming the recent highs in the S&P 500. However, the new highs in these market indexes are masking some internal divergences, which could be a sign of an overheating market as investors stampede into “growthier” stocks.

One such discrepancy, that has developed this year, is between the Growth and Value segments of the large-cap Russell 1000 Index. In fact, the first quarter of 2017 saw the largest quarterly outperformance by the Growth Index since 2009, and that gap has continued to widen since the end of March.

This growth-value disparity is also apparent within the S&P 500 Index where high momentum stocks have dramatically outperformed their more conservative index counterparts.

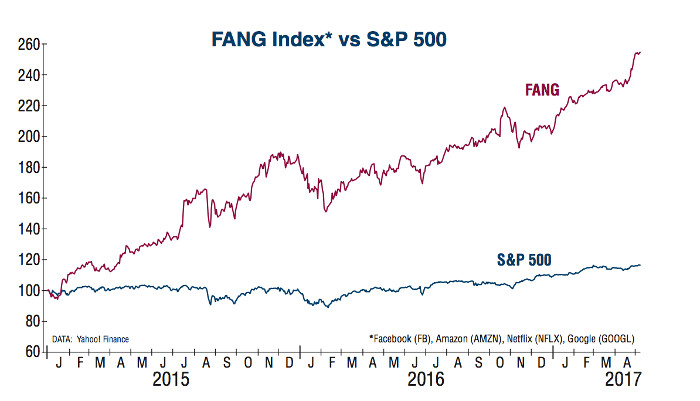

Notably, the “FANG” stocks, Facebook (FB), Amazon (AMZN), Netflix (NFLX), and Google (GOOG) have soared to such lofty levels that these four frothy stocks now comprise over 6% weighting of the S&P 500, and have contributed nearly one-quarter of the gain in the S&P 500 since the beginning of 2015!

The new highs that we’re seeing in the S&P 500 and secondary market indexes are a sign of broad market participation by investors, as well as speculators. Yet this is also a high-stakes game of musical chairs, and when the market outlook becomes cloudy and stocks begin to weaken, a cascade of selling could appear as speculators head for the door.

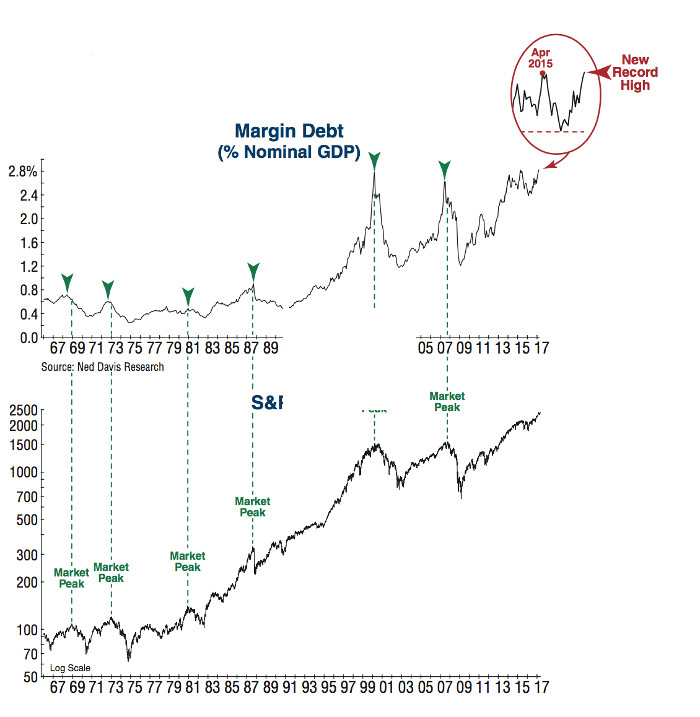

Margin debt as a percent of U.S. GDP is a measure of how much speculators are willing to borrow in order to capture a larger portion of market gains. The graph at right shows that when this indicator peaks (green arrows) and starts to decline precipitously, a market top has historically been imminent or already in place.

Following the election, speculators have once again become more active, pushing margin debt to a new record high. However, if this key indicator were to drop sharply below the low in early 2016 (red dotted line), this aging bull market will likely have met its demise.

For now, the key technical evidence and leading economic indicators continue to support a favorable outlook for the economy in 2017, and more new bull market highs ahead. But pressures are emerging that give us ample reason for caution and maintaining a healthy cash reserve.

We are not the only ones steering a more defensive course, as Warren Buffet — the consummate value investor — is holding 22% cash (nearly $100 billion) in his Berkshire Hathaway (BRK.A).

Most of today’s investors are piling into “index funds” of various types — thinking it’s a prudent risk-averse strategy. Long forgotten is the fact that the premier Vanguard S&P 500 Index Fund (VFINX) tumbled more than 55% in the last bear market — and valuations today are higher than at the start of that bear market!

As we’ve seen over the years, a bubble is invisible to those inside the bubble, and a momentum mania feels normal to those intoxicated by the ride. With extreme market valuations, record high margin debt, the FANG momentum mayhem, and indexing mania, there is only one way this is going to end – badly!

While the current bull market remains intact, and both technical and leading economic data supports more new highs ahead, we cannot ignore the inherent risks in an aging 8-year-old bull market. The time will come to move aggressively to the sidelines, and we intend to be among the first to do so.