We recommend investing your full allocation to equities in large-cap U.S. stocks (S&P 500 Index). And to developed country foreign stocks: iShares MSCI EAFE Index ETF and emerging markets iShares MSCI Emerging Markets Index ETF, or Vanguard VWO, says Marvin Appel, MD, PhD.

The year 2017 was a strong year for business profits and stock prices, while interest rates remained stable. The S&P 500 Index (SPX) rose almost 20% and did so with unusually low volatility: The S&P 500 went the entire year without so much as a 3% correction.

Corporate defaults among junk bond borrowers remained low at 1.5% and the spread between U.S. corporate high yield bonds and U.S. Treasuries contracted slightly to 3%, the lowest level since 2014.

So far the stock market is starting the year off with continued gains but the bond market is getting restive.

Let’s see what the crystal ball predicts for 2018.

Stocks are priced for perfection, so gains will be harder to come by this year

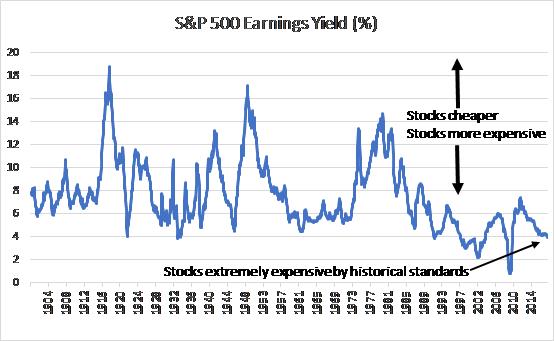

Relative to underlying earnings, stocks are very expensive by historical standards. The chart below shows that each dollar invested in the basket of stocks in the S&P 500 Index produced less than four cents of underlying business profit in the past twelve months. (That is, the earnings yield on the S&P 500 Index is just below 4%.) The only time profits were lower than this was during the tech bubble and bust, and temporarily during the financial crisis of 2008-2009. The S&P 500 Index has more than doubled since the end of October 2011, but earnings have grown by less than 30% since then.

That means that the vast majority of the stock market’s gains in the past seven years have come not from improved business performance but instead from investors being willing to pay more than they used to. This is unlikely to continue indefinitely.

That’s the bad news.

The good news is that corporate profits are growing briskly, so even if stock prices merely keep pace with profit growth there will be gains ahead.

I expect the economy to continue to expand with inflation remaining under control, allowing stocks to grow in tandem with growing profits at a slower rate—5% to 10%—than in 2017.

Note that the new tax law is projected to increase profits by 7%-10% by lowering corporate tax rates. The impact of this new business tax break should already be priced into stocks.

Stability in interest rates will be crucial for continued stock market gains

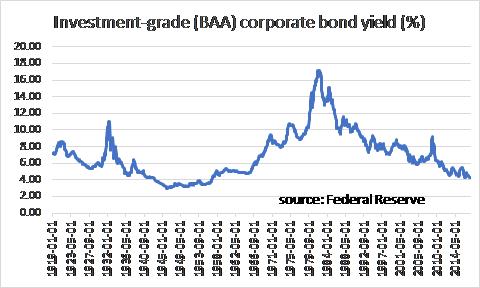

One reason why stocks have performed so strongly is that interest rates have remained at historically low levels. Even with stock dividend yields of under 2% and earnings yields under 4%, investment-grade bonds yielding just 2.5% are not attractive alternatives.

Just as stock earnings yields are near historic lows, so too are interest rates. For example, the chart below shows that investment-grade corporate bond yields are at levels not seen in more than 60 years.

In part as the result of the presidential election of 2016, interest rates jumped significantly, with the yield on 10-year Treasury notes nearly doubling from its low of 1.37% in mid-2016 to its high of 2.6% in March 2017. Since then, yields have been very stable.

One reason is that although interest rates are low in the U.S., they are even lower abroad. Corporate junk bonds in Europe pay just 2%—less than 10-year U.S. Treasury notes.

European and Japanese investors can get much better levels of interest income here than in their own countries (if they can tolerate the currency risk). As long as this remains the case, interest rates here should remain under control.

The implication for stocks is that I expect only modest gains in interest rates in 2018 which will not be sufficient to cause a significant market correction or a sustained downward pricing of stocks. Further down the road, however, inflation will accelerate and force interest rates higher, putting a drag on stocks.

Foreign stocks should outperform U.S. stocks

From 2011-2016 an American investor would have made far more money with the S&P 500 Index than in most broad-based foreign stock indexes. That trend appears to be at an end.

I perceive greater opportunity in foreign stocks over the next several years.

For example, even as U.S. stock market indexes such as the Dow Jones Industrial Average or the S&P 500 have made new highs, the iShares Emerging Market Index ETF (EEM) is still below its peak level from 2007. (See bottom half of the chart.)

The top half of the chart shows the relative performance of emerging markets compared to the S&P 500 Index (large U.S. companies).

Emerging markets lagged the S&P 500 consistently from 2011-2015. In 2016 emerging markets started to outpace the S&P 500 until the presidential election. In 2017, emerging markets were stronger than the S&P 500 Index. However, they have a long way to go before they recapture the ground lost in 2011-2015.

European and Japanese stocks have also lagged the S&P 500 Index over the past 10 years, and both began to keep up with the S&P 500 in 2017. In 2018 I expect emerging markets to keep up with or outperform the S&P 500 Index.

Investment implications

As we start 2018, the trends for stocks remain up and our models continue to indicate favorable conditions for U.S. and foreign equities.

We recommend investing your full allocation to equities in a mix of large-cap U.S. stocks (e.g.: S&P 500 Index).

In addition, some of your equity portfolio can be allocated to a combination of developed country foreign stocks: iShares MSCI EAFE Index ETF (EFA) and emerging markets iShares MSCI Emerging Markets Index ETF (EEM), or the Vanguard analog, (VWO).

Subscribe to investment newsletter Systems and Forecasts here…