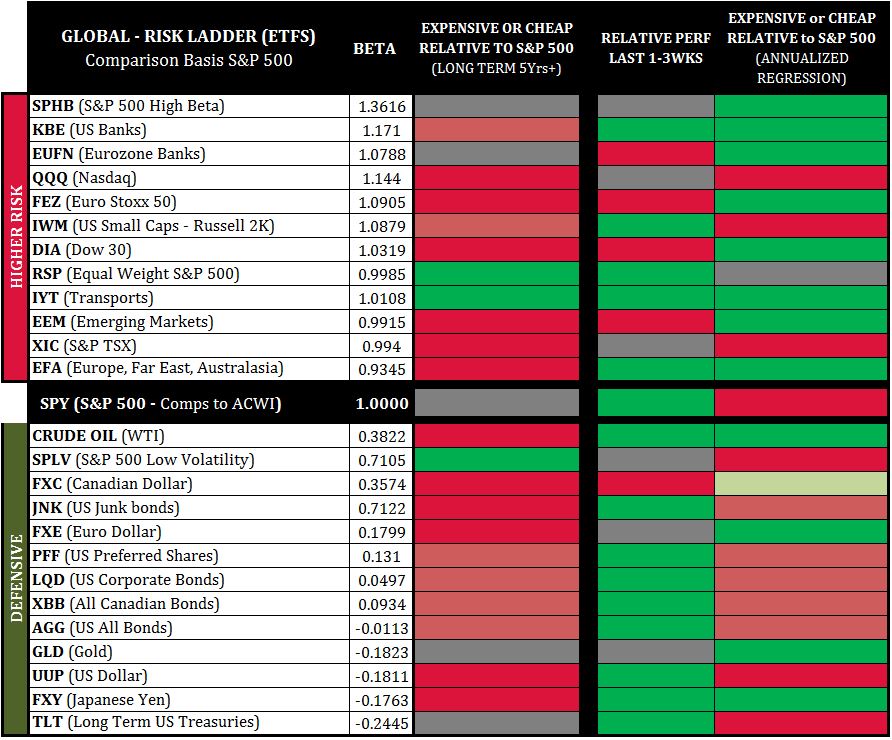

Higher-risk asset classes are polarized. Some very expensive and most very cheap, indicative of the geopolitical and trade war issues. Cheap: Dow, Eurozone Financials, US Banks, Hi-Beta, EuroStoxx 50, Emerging Markets, Eurozone Far-East & Australasia, Transports, Oil.

Watch Ziad’s Weekly Coaching Workshop here

Recorded: Friday July 20, 2018:

Duration: 1:55:40.

Global Risk Sentiment

Looking at the third column to the right we see a comparison of higher risk asset classes and defensive asset classes back to the S&P 500 (SPY) on an annual basis.

Comparison to the S&P 500 creates a “risk-ladder” where market risk is considered neutral.

When we see more green above the SPY-line (middle line) and more red below we have a general “risk-on” signal and vice-versa - red above, green below would be “risk-off.”

Currently, higher-risk asset classes are polarized.

Some very expensive and most very cheap, indicative of the current geopolitical and tariff trade war issues.

Cheap: Dow, Eurozone Financials, US Banks, Hi-Beta, EuroStoxx 50, Emerging Markets, Eurozone Far-East & Australasia, Transports, Oil.

Expensive: Nasdaq, Russell 2K, TSX, S&P 500, USD, US Treasuries.

While defensive-asset classes present as mostly expensive.

For equities to advance, the USD must continue soften up along with US Treasuries.

Overall, our global risk ladder signals risk-on into the week ahead, but the signal is suspect when married with the price action to close the week and technical tools pointing us down.

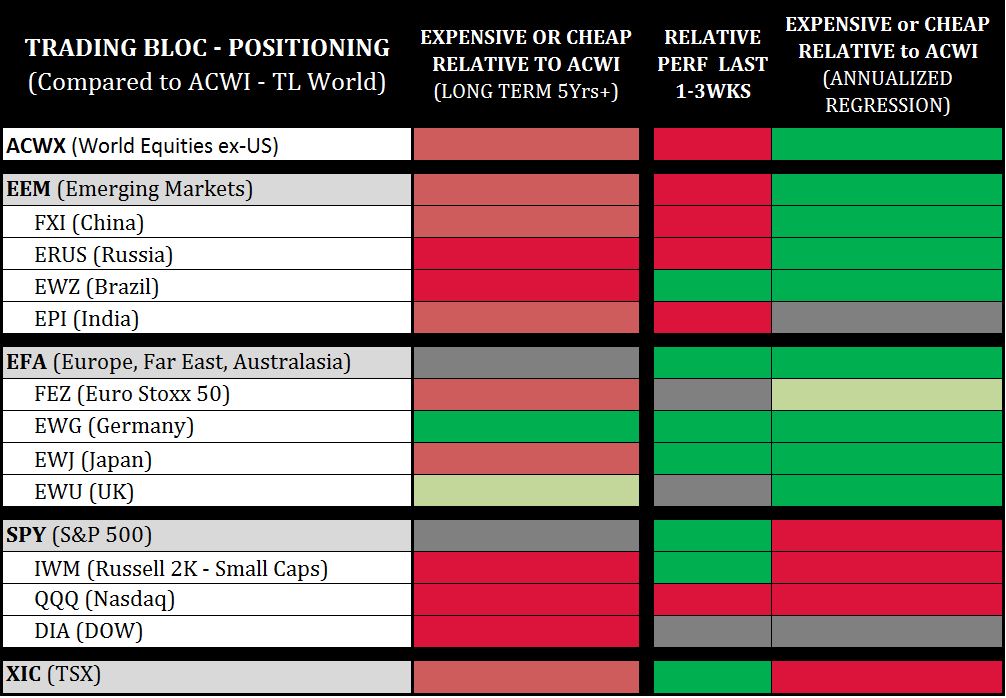

Trading Bloc Positioning

This chart compares major Trading Blocs back to the entire global equity market (ACWI), to determine which spaces are relatively cheaper or more expensive.

Why? Capital-flows usually tilt towards relatively cheaper spaces, especially if the June 28 macro-market swing low continues (i.e. S&P 500 > 2,805).

US markets (ex the Dow DIA) present as the most relatively expensive while Emerging Markets (EEM), and the Eurozone Far East & Australasia (EFA) present as cheap (on annual routines).

The TSX presents as 2 standard deviations expensive, which implies the TSX is likely to under-pace the world on the way up and/or move faster down.

If markets rise, expect out performance from Equities outside of North America.

If markets move down, expect North American markets to move down at a faster pace vs. the world.

View the Independent Investor Institute trading ideas and strategies videos here.