Long-term interest rates took a small jump starting on July 20, with the yield on 10-year Treasury notes rising from 2.85% to 2.97% in two days. Here’s what that means for investors and traders who worry about a recession, writes Dr. Marvin Appel Thursday.

The catalyst was an announcement from the Bank of Japan that they were considering stepping back from quantitative easing, although subsequent pronouncements suggest that the printing presses in Japan will continue to pump out currency for at least another year, until after a pending tax increase has taken effect. (The Bank of Japan has a balance sheet of approximately 100% of Japan’s GDP, compared to less than 20% for the Federal Reserve relative to U.S. GDP.)

The bond market’s action demonstrates that long-term interest rates are artificially depressed due to quantitative easing. This is good news to those who worry that the relationship between short and long-term interest rates, called the yield curve, in the U.S. are signaling a coming recession.

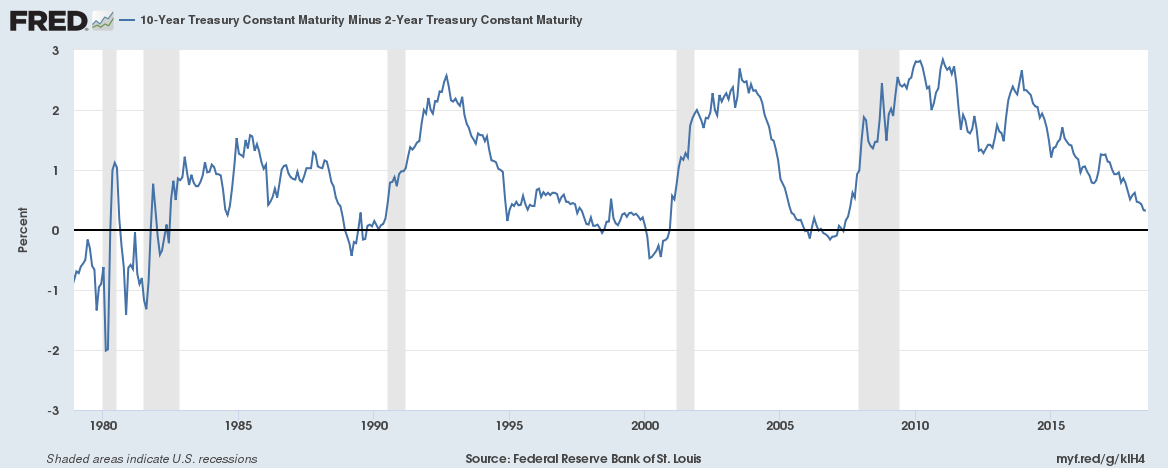

The yield curve is the difference between long and short-term interest rates. An example would be 10-year Treasury note yields minus 2-year note yields. Normally, long-term rates are higher but occasionally the reverse is true.

When short-term rates are higher than long-term rates the yield curve is said to be inverted. Much of the time, inversions of the yield curve are followed by recessions. You can see this in the chart below. There were some occasions when the yield curve inverted and then renormalized well in advance of the onset of the eventual recession. Nonetheless, yield curve inversion has been a reliable economic warning signal.

Now, the spread between two-year and 10-year Treasury note yields is just 0.32% (32 bp), the narrowest since 2007. Many are concerned that as the Fed continues to raise short term interest rates while long term rates remain stable, as they have for almost six months, that the yield curve will invert again.

My own expectation is that the yield curve, if it inverts, will not be as effective an economic signal this time because past yield curve inversions did not occur in the setting of quantitative easing.

If central banks (particularly the Bank of Japan and the European Central Bank) are distorting the bond market, what other signals can you watch for a recession warning?

I propose looking at the high-yield bond market.

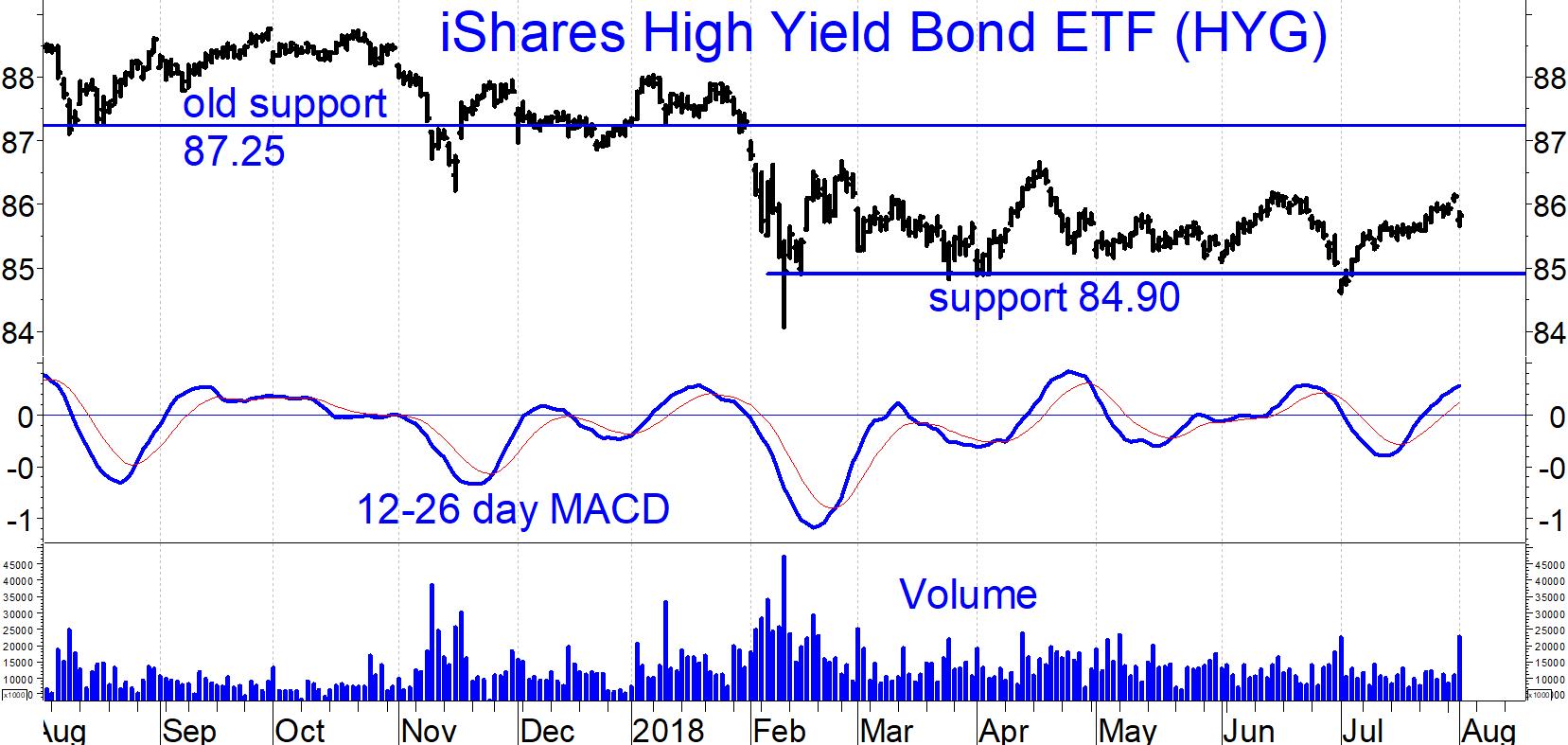

High-yield bond issuers are riskier than most other borrowers, so they are particularly sensitive to any deterioration in the economic climate. Unlike Treasuries and high-rated investment-grade bonds, high-yield bonds fall when recession fears mount because of their default risk. High-yield bonds peaked in 1989, 1998 and 2007 in advance of recessions.

High-yield bonds also stall (but generally suffer only mild losses) during periods of broadly rising interest rates such as 1994 or 2013.

The chart below shows iShares iBoxx $ High-Yield Corporate Bond ETF (HYG, price-only). Interest rates jumped in January, eventually contributing to a breakdown in high-yield bonds in early February. The good news is that HYG has been holding its ground since its February low, with a new support level of 84.90.

You could also look at the difference between the yields on high-yield bonds and Treasury notes of comparable maturities. This is a measure of how the bond market assesses credit risk. Like the price of HYG, interest rate spreads between high-yield bonds and Treasuries have been stable since February. (See chart.) Lower spreads reflect bullish market sentiment about high-yield bonds.

Of course, if spreads remain stable then any increases in long term Treasury rates (such as the yield on 10-year Treasury notes) will cause commensurate price declines in high-yield bonds. But as in 1994 and 2013, such losses will be well contained and largely offset by interest income.

Implications

Our high-yield bond timing models remain on buy signals. However, our investment-grade bond model is on a sell signal, suggesting that long term interest rates could rise further. For example, the chart below shows the long-term uptrend in 10-year Treasury note yields since 2016 remains intact.

As long as the 6-19 week MACD of yields remains above zero, rates are at risk of rising. I interpret this constellation of observations as suggesting that high-yield bond funds remain profitable, but gains are likely to be gradual, with some of the interest income offset by capital losses resulting from rising interest rates.

Our bond timing models afford us potential protection in case the rise in yields turns out not to be so gradual.

Bottom line: A high-yield sell signal may be the most reliable recession warning in the current environment, and it is good news that no such sell signal has been forthcoming.

Sign up here for a free three-month subscription to Dr. Marvin Appel’s Systems and Forecasts newsletter, published every other week with hotline access to the most current commentary. No further obligation.

Watch Dr. Marvin Appel share ideas on MACD during interviews at TradersExpo New York:

I find a weekly MACD is most effective for bonds.

Duration: 3:41

Recorded: Feb. 25, 2018.

Duration: 2:57

Recorded: Feb. 25, 2018.