What does price behavior closing out week of August 6-10 tell us? An orderly decline, with additional downside-risk for the front half of the week the week of August 13, writes Ziad Jasani Sunday.

View my weekly strategy session here

Recorded: August 10, 2018.

Duration: 1:30:26.

Equities

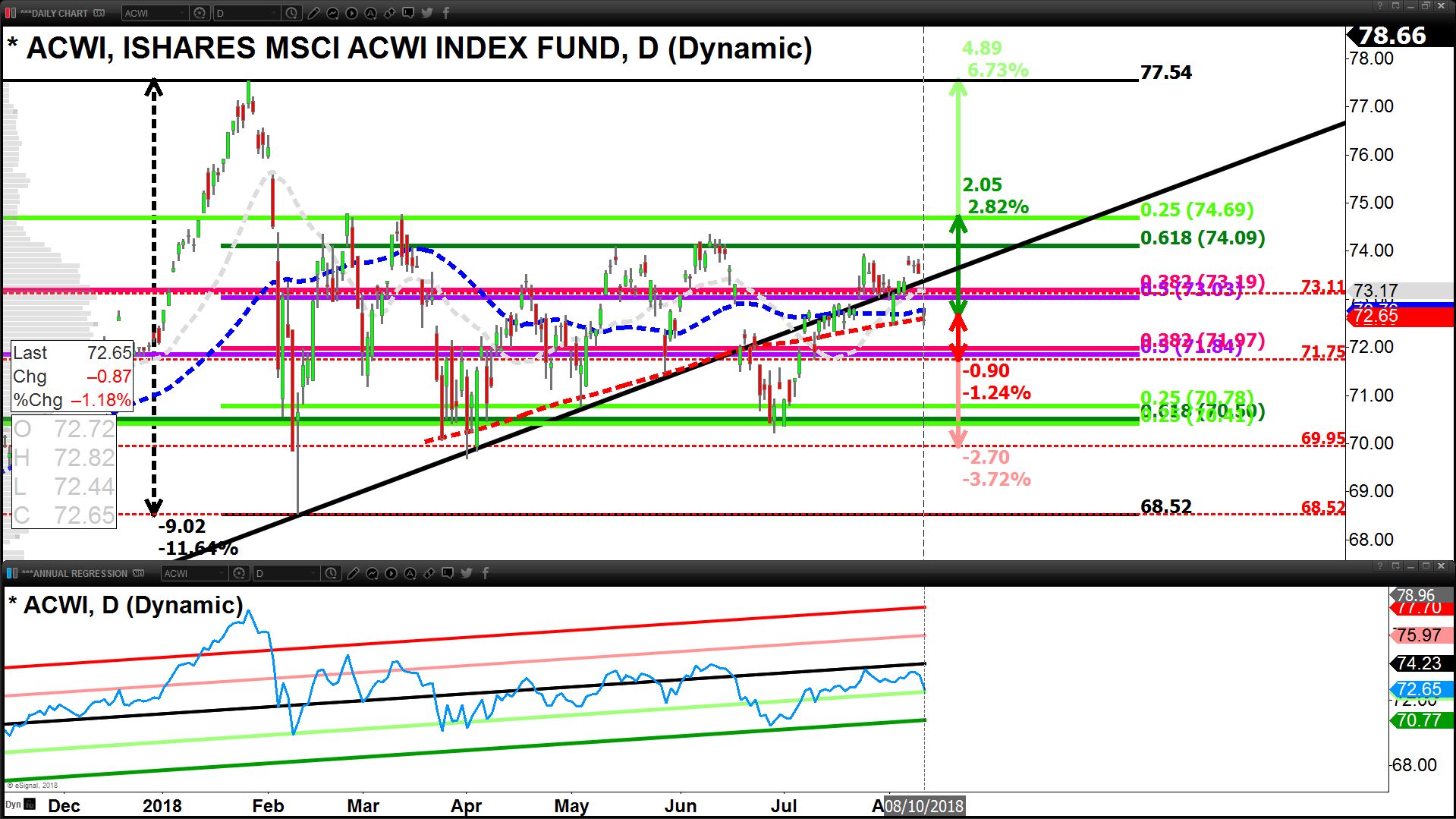

• The Global Equity Market (ACWI) is in a confirmed swing-high formation and below the 50% retracement level of Jan. 26 highs to Feb. 9 lows closing above its 200-day average but not depicting enough strength, implying a move down to $71.97 or $70.50 completing the sideways-channel-pattern-move.

• The World-Ex-US (ACWX, EEM, EFA, FEZ) is causing the bigger drag as the risk-off trigger is Emerging Markets, which is infecting the Eurozone Far East & Australasia. Lte June 2018 lows have not been taken out, but short-term bearish momentum suggests they are tested before a bounce up can occur.

Note: If EEM & EFA do not test late June 2018 lows, but make a higher low, it would be termed a bullish-divergence opening the door for Strong Buys to play a bounce.

• S&P 500 (SPX) closing below 2,835 implies more down-side risk; a break and implied closed below 2,824 implies down-side risk to the 50-day average 2,785 – this is a more likely out-come vs. a bounce higher to open the week.

• Nasdaq or “Technology Engine” is below its danger-line 7,850.

• Dow or the “Industrial-Material Engine” is below its danger-line 25,373 pointed to 25,000.

• TSX attempted to cling to its 50-day average (16,340) but closed slightly below 16,326; a break below 16,285 opens room for a drop to the 200-day average(15,949).

• Our Global Risk-Ladder suggests an orderly decline that persists only for a few days followed by a bounce up with haste.

• Relative routines globally suggest that the next Global-Equity-Market bounce is led by the World-Ex-US.

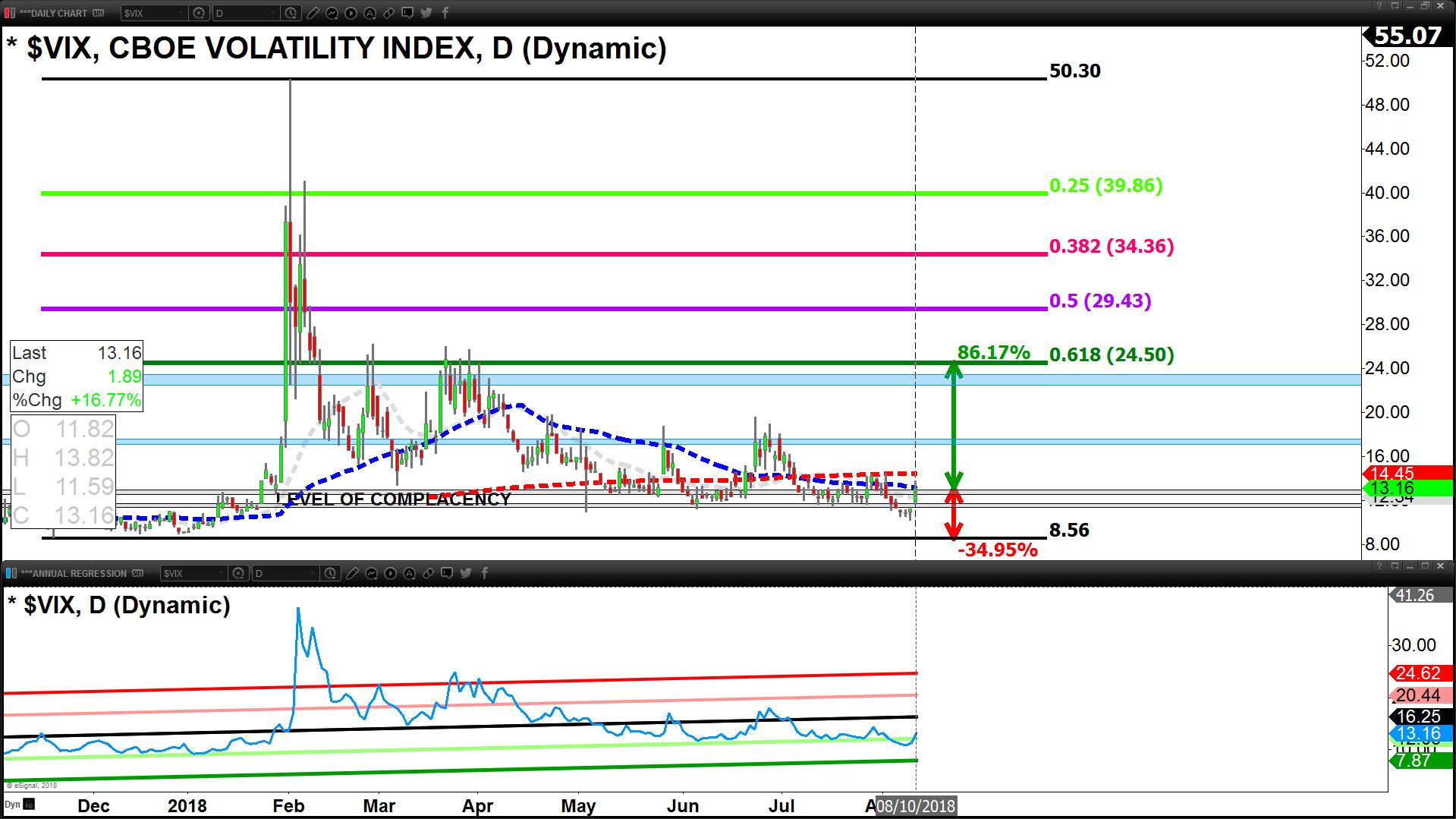

• S&P 500 Volatility Index > 50-day average implying more likely equities point down to start the week.

• Overall: We’re looking for a few more days of equity-price weakness before a bounce up that we can play. We do not see August 10 as the beginning of Correction 2.0. We ended the week net short (or long inverse ETFs): S&P 500, Nasdaq, Russell 2000, Dow, Emerging Markets, Eurozone and long Volatility; while maintaining Hold decisions broadly in the TSX (with tight stops) and have closed all if not most of our short-to-mid-term long-side swing-trades within the U.S. markets. We did a long on Oil over the weekend.

Bonds

• The Global Bond Market continues to present as dislocated and expensive on traders’ routines, but is likely to sustain a bid as the current risk-off event for markets plays out to open the week; no significant break-outs have presented on the current basing pattern for Bonds suggesting a further rotation into fixed income is warranted at this time, but playing out trades for the next few days works.

• US Treasury yield charts suggest a further flattening into this week but a steepening in the back-half of the week is expected when the 10-year yield bounces up off of support at 2.807%.

• Emerging Market Bonds (EMB) sold off with Emerging Markets (EEM) on August 10 affirming the negativity has legs into the week of August 13.

• High-Risk-Credit (Junk Bonds – JNK, HYG) are holding-up through the negativity with Oil adding further evidence of an orderly decline for Equities.

• Overall: Bonds are likely to enjoy a few days of upside, prior to Equities bouncing and Bonds generally swinging high under the top end of basing channels.

Currencies

• USD (UUP) continues to charge higher as a safe-haven through the current risk-off event August 10; however, the stark dislocation (expensive) suggests either a “new-normal” is forming or reversion to the mean (downwards) is to kick-in in the week ahead; If the EUR/USD breaks below 1.1350 we can side with a new normal being established – If the EUR/USD bounces up off 1.135 we are likely seeing the Equity-Risk-Off event ending and see opportunity in currencies on the other side of the USD.

• The yen (FXY, USD/JPY) maintains its defensive status through the current risk-off event, a swing-low in the USD/JPY would be an early indicator of Equity sentiment turning risk-on.

• The Canadian dollar (FXC, USD/CAD) was bullied down by the Saudis during week of August 6 – 10 and despite strong Jobs data on August 10 and Oil reversing positive the sell-off continued on August 10 we maintained long DLR-T over the weekend. Wewill be looking for a strong bounce on the CAD with Oil when sentiment turns risk-on for the global equity market. In effect we are looking for a swing-high on USD/CAD near 1.3204 and a bounce on FXC at $74.60.

Overall: The strength of the USD is likely to pivot weaker closer to Wednesday, August 15 timed with the release of U.S. Retail Sales which we are expecting a meet-to-a-miss on vs. the consensus estimate. To open the Week (Aug 13th – 17th) we are expecting further USD strength and euro weakness, but are expecting the yen to hold its ground, which in-turn is likely to keep Gold toggling between $1,220-$1,216 holding it back from a bounce; a bounce on Gold above $1,220 is expected on Wednesday.

Join Ziad at MoneyShow Toronto Sept. 15 when he discusses Portfolio Management Strategies for Active Investors. Information: ZiadJasani.TorontoMoneyShow.com