At the Independent Investor Institute, our online community of active & affluent investors/traders were guided to lower short-to-mid-term long-side equity risk exposure as of Sept. 21. And we talked scenarios, strategies and tactics Tuesday in this video for Oct. 8-12.

View my weekly strategy session video here.

Recorded: Oct. 9, 2018.

Duration: 1:14:25

What does the Fixed-Income (Bond) Market tell us about the week ahead for Equities?

Break-outs on U.S. Treasury yields (10-year, 30-year, 30-year long-term) coupled with breakdowns of major support level on U.S. Treasury Bonds (TLT) last week add downside risk for Equities this week.

High-Yield or Junk Bond Markets (JNK, HYG) are coming down to major support levels, which have so far held. Outside of fear-based trading behavior that could continue the bond-route, inflation data due on Oct. 10 & 11 will have the most sway with bond traders.

If we get cooler than consensus estimated prints on PPI (Oct. 10) and especially CPI (Oct. 11) a bounce for Bonds, and a modicum of stability is reintroduced into capital markets (globally).

In this scenario we would be willing to accumulate the following ETFs on swing-trading basis: TLT, LQD, AGG, EMB, XBB-T, JNK.

However, if the data comes in hotter, we would be willing to short or play inverse on Bonds via these two ETFs: TBT, SJB.

Our economic modeling suggests the inflation data comes in cooler, affording a bounce for Bonds and at minimum stabilization for Equities, if not a bounce in tandem.

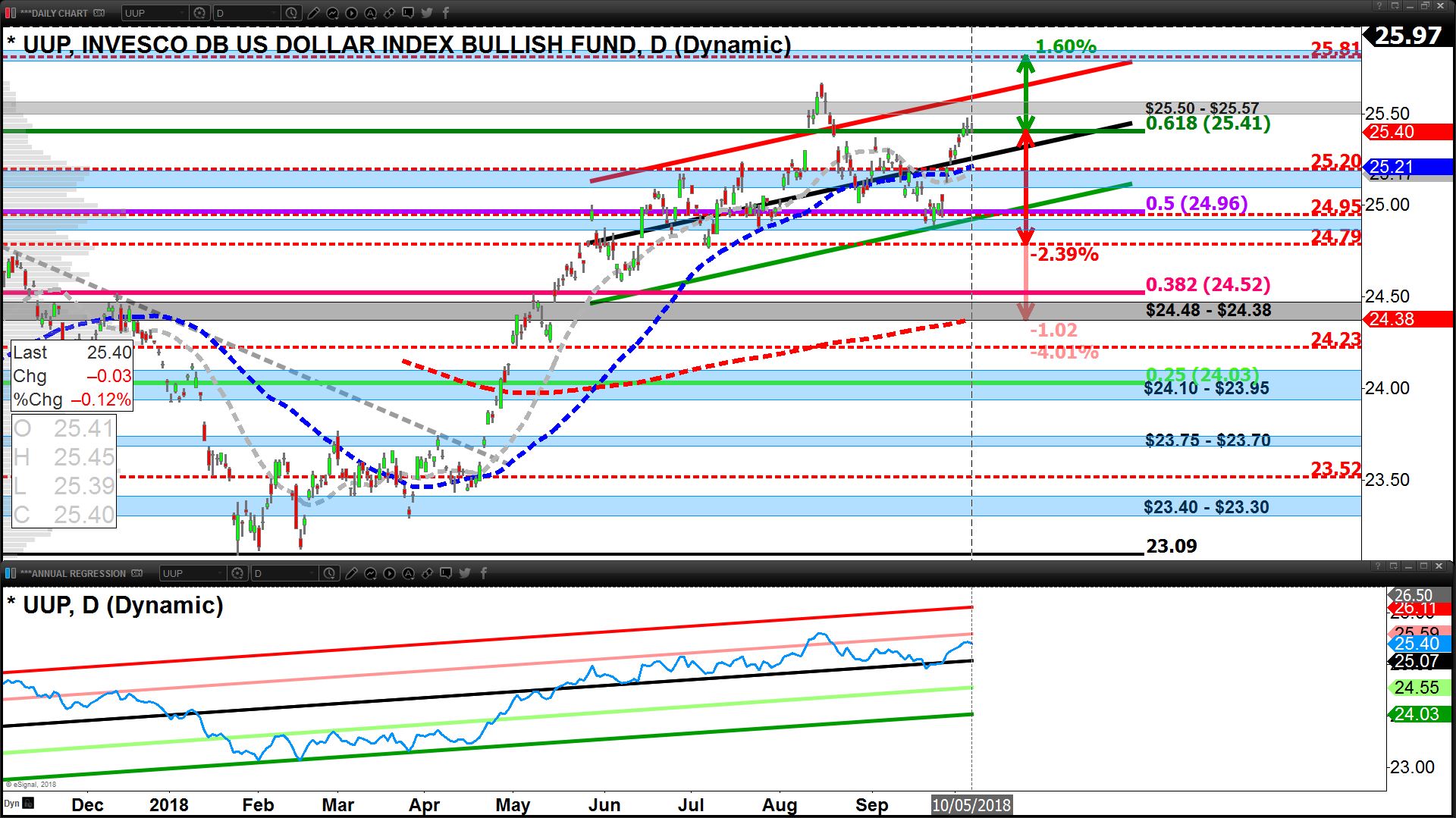

What does the Currency Market tell us about the week ahead for Equities and Commodities?

As Traders de-risked from Equities last week, and as Treasury yields broke resistance structures a re-coupling (positive correlation) took place with the USD and Treasury yields. This bodes well if U.S. inflation data comes in cooler.

Why? As yields soften so likely would the USD. Furthermore, the major currency pairs are all set up technically to push the USD (UUP) down; with the EUR/USD (euro) and GBP/USD (pound) in an inverted head and shoulders pattern, and the USD/CHF (Swissy) and USD/JPY (yen) in swing-high formation.

If U.S. inflation data comes in cooler we would be buyers of: FXE, FXY, FXB, FXF.

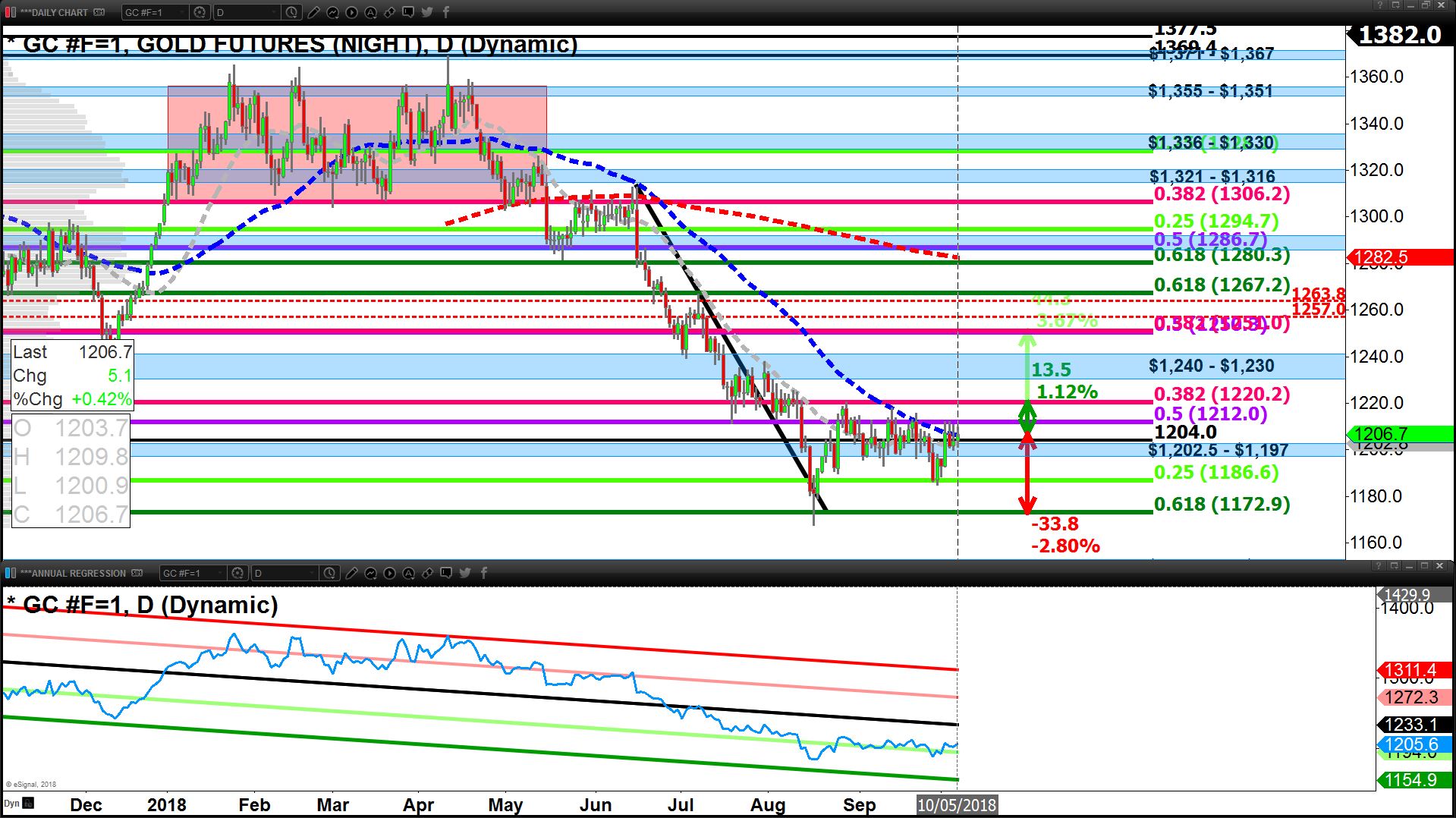

To add, a softening of the USD would present the opportunity for Precious Metals (GLD, SLV, CGL-T), Base Metals (DBB, CPER, SLX) and Miners (XME, GDX, SIL, XGD-T) to rise, and stabilize the recent weakness in commodity-laden Currencies (USD/CAD, AUD/USD), if not actually create a bounce.

We ended last week building small positions in currencies on the other side of the USD, primarily the yen as de facto short-term short on the USD.

What does the Commodity Market tell us about the week ahead for Equities?

Ingoing presentation suggests commodity-laden Equity Markets/Sectors are likely to struggle to start the week, however, the odds of a turnaround by/on Thursday Oct. 11 are at 62%.

Short-term (30-day) correlations between the USD and Oil have turned positive (29%) and the inverse correlation with Gold has weakened to -35%. Nonetheless, a softening of the USD on cooler inflation data would perk up the Global Commodity Complex (DBC).

Oil starts the week in a swing-high formation and is pointed down to the $73-$72 level, despite our modeling suggesting inventories are likely supportive; we are in the market to buy a bounce on Oil at the $73-$72 level (USO, UCO, HOU-T).

A sharp drop on the USD would afford Gold a breakout above resistance of $1,212 putting us on the buy-side (GLD, CGL-T, UGLD).

The recent breakout on Natural Gas is taking a breather, but net bullish over the next two weeks, we look to buy a bounce off $3.05 this week (UNG, HNU-T). Our base case for the week is commodities pointed down into mid-week, and the up to end the week; and that includes precious and base metals.

Enjoy a complimentary-no-strings-attached 30-day subscription to Ziad Jasani’s Daily Insights. Simply send Ziad an email with FREE TRIAL in the subject: ziad.jasani@educatedtrader.com