News about trade issues is whipping the market around, writes Marvin Appel.

Between May 3 and May 13, the S&P 500 SPDR (SPY) lost 4.5% before bouncing some 3% through May 16 (intra-day). Although a significant market correction is unlikely with our U.S. equity timing model, the fact that stocks are so tuned into updates on the trade front is worrisome.

It does not look like China is willing to yield any ground on the fundamental issues of forced technology transfer and giving a cut to local partners as the price of access to the Chinese market. China and the United States had ostensibly reached agreement on many of these issues before Chinese negotiators reversed themselves to take a harder line (leading to the market’s recent losses). That leaves only two possible outcomes: First, the United States might cave in order to protect the economy and our exporting sectors in the near term. That would boost stocks and economic statistics for now but would ultimately hurt U.S. interest as we lose our intellectual property. Second, the United States might move towards an economic divorce from China, which would involve years of drag on multinational U.S. businesses as they develop alternative supply chains. The second path will hold back the stock market for now and will temporarily hurt some sectors of the economy but would ultimately leave our country in a stronger position in the years to come. It is a coin toss which way the trade issue will resolve.

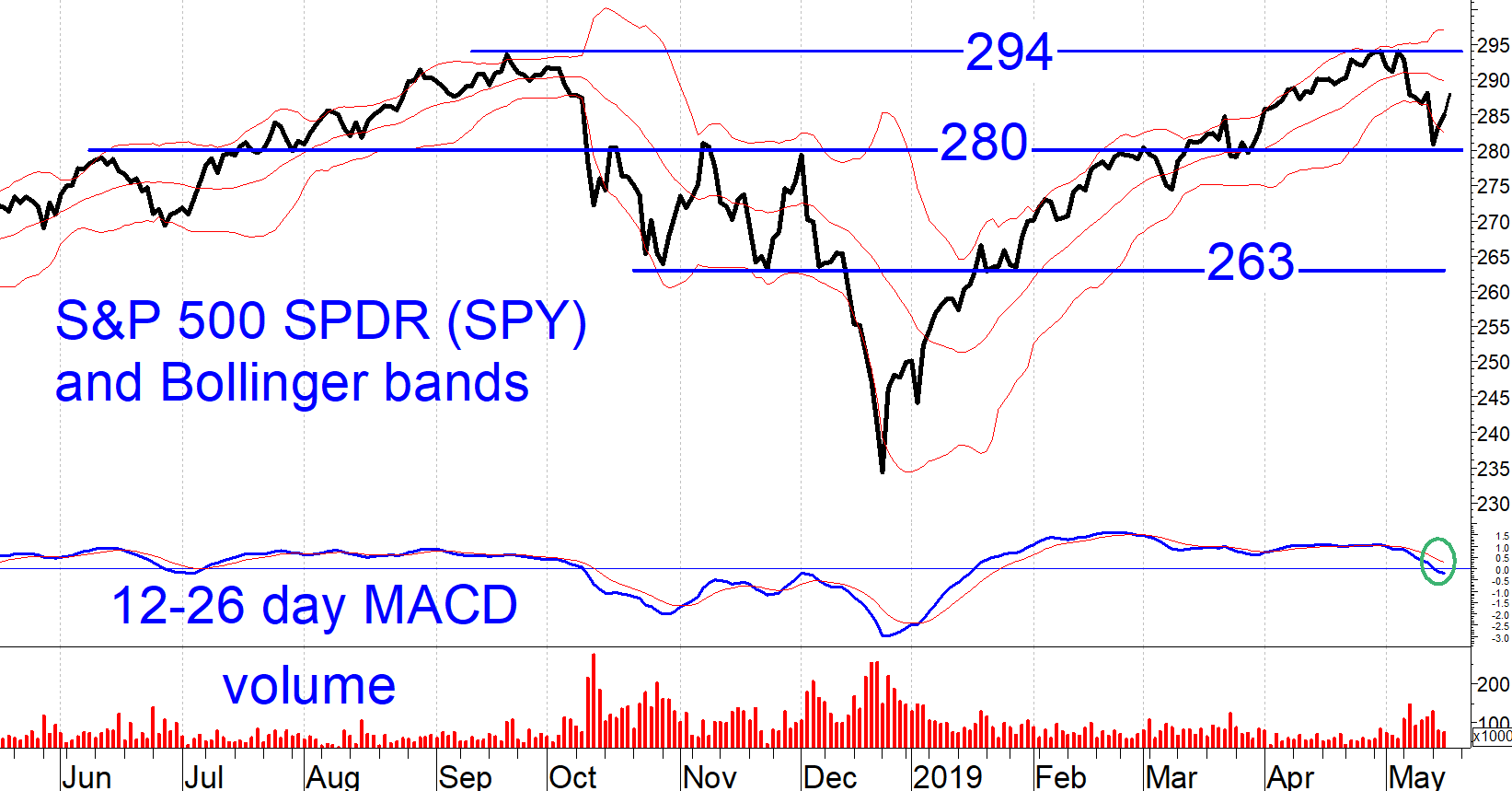

My expectation is that stocks will have to reprice themselves to reflect an era of more restricted trade. Given how large our economy is and how relatively little of it depends on exports, I expect that we will be able to weather the trade storm without a recession. The implication is that risk should be well contained for U.S. stocks, perhaps limited to a downside of 280 on SPY that we have already seen or perhaps limited to an extension of the recent decline down to 263. (See chart below.) On the other hand, our foreign equity timing model went on a sell signal this week, underscoring that U.S. stocks remain more attractive than foreign stocks.

Figure: S&P 500 SPDR (SPY), 20-day +/- 2 stdev Bollinger bands and 12-26-9 day MACD.

The near-term SPY technical picture suggests a battle between bulls and bears around 280.

The chart shows that in April and early May, SPY retested the Sept. high around 294 and pulled back to the 280 level that was support last July and resistance in October and November, as well as in February this year.

The nearest resistance is the middle Bollinger band around 289-290. During an uptrend, SPY should spend most of the time between the middle and upper bands. During a downtrend SPY should spend most of its time below the middle band. During a sideways market SPY should spend roughly equal time above and below the middle band while rarely extending beyond the upper and lower bands.

For now, SPY is operating within a 280-294 trading range. However, the behavior of SPY relative to its Bollinger bands over the next two- to three weeks will tell us what type of trend is now in effect. My bet is on a sideways trend.

The 12-26 day MACD has slipped below zero for the first time since January (circled in the chart above). This does not predict a turn-around but bears watching to see if any bullish formations such as a rising double bottom are generated.

Bottom line

Investors should remain cautious. Equity exposure should be concentrated in large-cap U.S. stocks. SPY is a good default option, and the Consumer Staples Sector SPDR (XLP) is also appealing. Even though our equity models are on a buy, most of our clients have 55% or less equity exposure. Shorter-term traders can look to open covered SPY call positions if SPY pulls back to 281 or lower. With VIX at its highest levels since January, the potential rewards from such a strategy compare favorably to buying and holding SPY alone.