One of the ultra-low-risk strategies developed by BCI in 2020 involved selling weekly 10-Delta cash-secured puts, explains Alan Ellman of The Blue Collar Investor.

This created a greater than 90% probability that the puts would not be exercised (expire in-the-money or with intrinsic-value). Since 2020—2021 represented an unusually low interest rate environment, annualized returns of 8%—15% looked pretty darn good. Since our contract obligations are for five days, Monday holidays caused a significant decline in that week’s annualized returns. No big deal since it’s only a few weeks per year. This article will offer a solution, with pros and cons, on circumnavigating this Monday holiday issue as it relates to this strategy.

Observations on Rolling Weekly Puts on Expiration Friday

I have noticed that by rolling the puts between 11:00 AM ET and 1:00 PM ET on expiration Friday to the following weekly expiration Friday, the annualized returns will not be impacted to any significant extent. The downside is that we are now undertaking weekend risk, which is not the case if we simply trade between Monday and Friday.

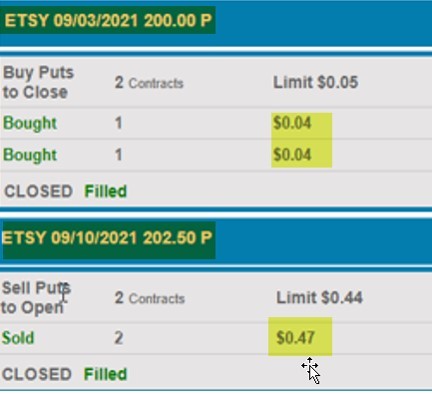

Real-Life Example With ETSY Taken From One of my Portfolios

- 8/30/2021: Sell two times $200.00 9/3/2021 puts at $0.42

- 9/3/2021: ETSY trading at $220.38 at 1:00 PM ET

- 9/3/2021: The cost-to-close the 9/3/2021 $200.00 put was $0.04 per-share or $8.00 for the two contracts

- 9/3/2021: The 9/10/2021 $202.50 put (Delta of -0.9) generated $0.47 per-share

Brokerage Account Statement Showing the Etsy (ETSY) Put Options Being Rolled Out-and-Up Retaining the 10-Delta Status

ETSY: Rolling Puts Out-and-Up

Annualized Calculations for the 9/3/2021 Contract Expiration ($200.00 put)

[($0.42/ ($200.00 — $0.42)] x 52 = 10.94%

Annualized Rolling Calculations for the 9/10/2021 Contract Expiration ($202.50 put)

[($0.47 — $0.04)/ $($202.50 — $0.47)] x 52 = 11.07%

Discussion

There was virtually no difference between the original annualized returns and that the rolling returns despite one less day in the contract. Certainly, one trade does not make a scientific study, but I’ve done this a few dozen times (as of writing this article) and all had similar results. The advantage of this rolling is higher returns for the four-day week and the disadvantage is the weekend risk incurred. Since holiday weekends are usually quiet, the risk is limited but present, nonetheless.

Market Now Deeply Oversold

I created a chart showing how the recent decline in the stock market (S&P 500) has moved the market, technically, into oversold territory. The chart below shows the stochastic oscillator, a momentum indicator, to be in oversold territory (below the 20%—far right circle). The last four times this occurred, the market immediately rebounded:

The S&P 500 (SPX) and the Stochastic Oscillator

Learn more about Alan Ellman on the Blue Collar Investor Website.