Bulls were sideswiped early Friday by an extremely robust January nonfarm payroll report, states Jon Markman, editor of Strategic Advantage.

Surging bond yields sent the benchmark S&P 500 (SPX) as low at 4,451 in the morning before buyers showed up.

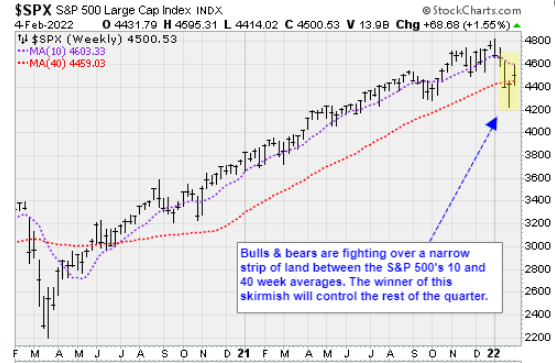

Bulls did try to push through the 4,530 overhead resistance level later in the session, but sellers resurfaced into the close. The index closed at 4,500, up 0.5%.

Volatility is extreme as both bulls and bears find data points to support their agendas. These macro themes—stronger corporate profitability vs rising inflation—will play out again this week with more key fourth quarter earnings reports and Friday’s release of the consumer price index report.

Ultimately, I suspect that bulls will find the energy to push through 4,530 and make a serious run at 4,620, the 50-day moving average, but it's not a slam dunk. Bears appear to be squandering their window of opportunity, but don’t count them so long as the S&P 500 remains below that 4,620 level.

If buyers fade back into the mists, critical support for the S&P 500 remains at 4,210. If breached, below that level lies bears’ house of darkness and pain.

Upshot

Stocks rebounded Friday after January's job gains surged well above estimates, while Amazon's (AMZN) upside fourth quarter earnings boosted the beaten-up tech sector.

The Nasdaq Composite (^IXIC) climbed 1.6% to 14,098.01 to bring its weekly gain to 2.4%. The Dow Jones Industrial Average (DIJ) closed slightly lower at 35,089.74 but was up 1.1% this week.

Consumer discretionary and financials led the way, while the materials sector lagged.

The 10-year US Treasury yield surged nine basis points to 1.92%, the highest since December 2019…West Texas Intermediate crude oil surged 2% to $92.10 a barrel.

Oil prices surged to fresh seven-year highs on continuing supply concerns in the face of strong demand and geopolitical tensions as Russia, the world's number three producer, continues to threaten Ukraine. A Texas cold snap threatened to squeeze shale oil supply.

Nonfarm payrolls shrugged off concerns about the impact of the Covid-19 omicron variant on the labor market, while the workforce participation rate rose to the highest level in two years.

Nonfarm payrolls climbed 467,000 in January, and December's gain was revised up to 510,000 from 199,000 previously, the Bureau of Labor Statistics said Friday. The Econoday consensus was for a payroll rise of 150,000. Job gains for November and December were revised up by a combined 709,000.

"We had expected that omicron-related callouts and business closures, especially in the leisure and hospitality sector, would generate a contraction in payrolls," Jefferies economists Thomas Simons and Aneta Markowska said in a note. "Instead, we saw leisure and hospitality jobs lead the increase in employment."

In company news, Clorox (CLX) reported a decline in fiscal second quarter adjusted earnings and sales while lowering earnings guidance for the full-year 2022. Shares sank nearly 15%, the biggest decline in the S&P 500.

Amazon shares soared 13%. The company said it plans to raise the price of Prime membership to counter higher costs and increase sales. The Amazon Web Services data center business boosted fourth quarter revenue, while earnings got a lift from the investment in electric truck developer Rivian Automotive (RIVN).

Snap (SNAP) shares skyrocketed 59%, rebounding from a decline of nearly 24% Thursday. The social media giant reported late Thursday non-GAAP fourth quarter net income and revenue that exceeded Wall Street expectations and guided revenue for the current quarter above analysts' estimates.