The Federal Reserve’s move toward raising interest rates has created a difficult set of market conditions in which trader indecision is causing a trendless, stop-and-go, nearly impossible to trade market, states Joe Duarte, technical specialist and editor of In the Money Options.

The Fed’s Psycho Warfare

A key component in any battle plan is to use psychological warfare as much as possible in order to preserve resources which can then be deployed in the conquest and consolidation phase that follows open combat.

And the Fed is following the playbook to a T.

The central bank seems to be hoping for a repeat of the market we saw in 2003-2004, where stocks fell aggressively before the first interest rate increase of the cycle but were able to hold their own thereafter.

That’s likely why they’ve been talking in a loud voice about raising interest rates aggressively—well ahead of the expected March launch of what the majority of observers expect to be a protracted and lengthy period that includes multiple rate hikes.

The consensus number seems to be for seven rate increases before the cycle ends, to which we humbly respond:

Really?

What’s the Point?

The end game to this talk now and hope later strategy is to create the conditions for a slowing economy by engineering a meaningful, but not irreparable, fall in stock prices ahead of the actual interest rate increases.

Specifically, the hoped-for goal is that the Fed will have to raise interest rates fewer times than it would have to do otherwise.

This, of course is due to the fact that central bankers know full well that the stock market is a huge influence on the economy, which is the basic tenet of my MELA system—M (Markets), E (Economy), L (Life Decisions), and A (Algos) all work in tandem.

The Market is the Economy

Familiar readers are aware that in MELA, the action in the markets is what drives the spending habits of those with IRAs, 401 (k) plans, and well-funded trading accounts. When the stock market is doing well, this subset of the population, which is responsible for an outsized share of economic activity, feels more comfortable in spending. And it’s their spending that drives economic growth.

In other words, the Fed does not really want to break the MELA crowd’s back. But it does want to squeeze inflation out of the system.

The problem is that the current inflation is mostly being fueled by the limits of the current supply and demand scenario that has emerged after the Covid pandemic and its effects on the way people live and work; along with government policies, which have helped shape and reinforce this behavior pattern. And those things are slow to change.

Meanwhile, with the world drowning in debt, if the Fed goes too far, it may have more trouble on its hands than it may be able to resolve quickly, even if it eases aggressively and restarts the printing presses.

Meanwhile, if and when the MELA crowd puts its hands in its pockets because of an increasingly impossible market to trade, and the repercussions of that on its spending habits become apparent, the negative effect on the economy may be more depressive and happen faster than any Fed model may predict.

Meanwhile, prepare for a continuation of the current directionless market including the big air pockets we’ve seen of late in stocks with bad earnings or any news item which disappoints.

New Low on NYAD Suggests More Trouble Ahead

The New York Stock Exchange Advance Decline line (NYAD) and the major stock indexes continue to struggle and have repeatedly failed to rise above key chart resistance points, which suggests that sellers are patiently awaiting new opportunities to lighten up on stocks at these key price areas.

This is interesting because every price drop is accompanied, as you would expect by a rise in the CBOE Volatility Index (VIX), which measures put option volume. And while VIX does rise with the selling sprees, it has yet to move decisively above the 30 area, which suggests that the current difficult-to-trade market we are seeing at the moment could go on for some time as there is no sign of a significant capitulation by the bears.

A rise in VIX signals that put option volume (bets that the market is going to fall) are on the rise. What follows when put volume rises is that rising put volumes cause market makers to sell puts and simultaneously hedge their bets by selling stocks and stock index futures.

But what we’re seeing now suggests that dealers are being forced to put on hedges and then remove them as they counter trader indecision. And this is what’s causing the stop-and-go price action.

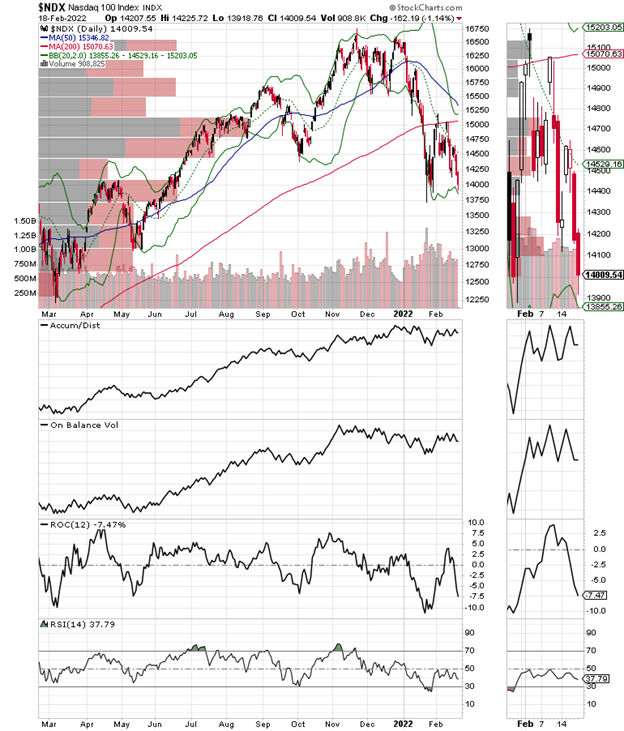

The Nasdaq 100 Index (NDX) never made it back above its 200-day moving average again. The index continues to test the recent lows, but as the S&P 500 (SPX) has managed not to break below this key support area.

The S&P Small Cap 600 Index (SML) again remained well below its 200-day moving average. There is some relative strength here as SML is mostly going nowhere while the rest of the market continues to fall. Whether this means that small stocks will lead the next up leg in the market remains to be seen.

To learn more about Joe Duarte, please visit JoeDuarteintheMoneyOptions.com.